401(k) Plan Fees: Understanding Costs and Maximizing Returns

The new 401k fee disclosure requirements have brought a lot of attention to 401k plans, which is a good thing. Most people don’t pay too much attention to their administration and plan fees since they usually only have one option for their 401k administrator, and often only a handful of investment options. The new fee disclosure requirements are changing this, and many people are finally becoming aware that they may be paying too much to their plan administrators and fund managers. As of August 30th, 2012, employers will be required to clearly list the fees employees are paying for their 401k plans, making it easier to compare 401k plans.

How Does Your 401k Plan Compare to Other Plans?

One of the easiest ways to compare 401k plans is to visit BrightScope.com, which is an online resource that compares 401k and 403b plans from a variety of businesses and organizations. You can use this tool to review the 401k plan and investments at your company, or use it to compare 401k plans at more than one company. You can get a general idea of how good a 401k plan is at a company by using their tool without logging in. Here is an example of the Google 401k plan review.

Using BrightScope as a visitor will give you basic information, but you will need to create an account if you want a more in depth review of the plan, or if you want to compare 401k plans at more than one company. The more in depth reviews allow you to input details such as your income, the company you work for, the investments you have selected, and other items. From there, the tool will give you a basic report showing you how much you are paying in fees, and how much it can affect your investments in the long run.

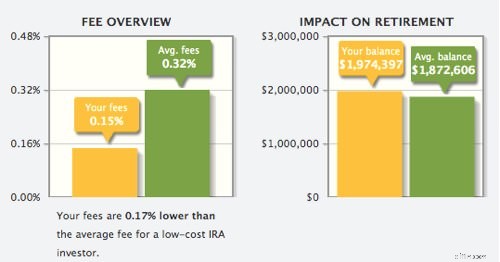

The screenshot below shows a hypothetical report showing a 401k plan with an overall expense ratio of 0.15% compared (yellow) to the average fees of 0.32% (green). These are only the fund fees and not the administrator fees. As you can see, reducing fees can earn you tens of thousands more over a lifetime.

How Can You Use This Information?

As we mentioned, you can use this tool to compare your plan against the industry, or you can compare multiple employer plans. If you are searching for a job, you can use this as one of your criteria for choosing a job offer over another company. I wouldn’t use a 401k plan as my #1 option, but it would be a good tie breaker. You could also use this tool to decide which plan to invest in of you have more than one 401k plan. Also consider that while you might only have one 401k plan, your spouse might have one as well. If you and your spouse have combined accounts, then you may consider investing up to the company match in one account,then investing a larger percentage of income in the plan with the better options, maximizing your investments.

“Wait a minute,” you say. “I’m not married, my company only offers a few oinvestment options, and I’m not planning on leaving for a new employer any time soon. How can I use this to my advantage?”

Great question. Brightscope will also look at your individual investments within your plan and give you an idea of the fees you are paying for each fund. You may find it beneficial to switch to an alternate fund that charges a lower management fee.

Comparing 401k Plans – Real World Exercise

I used to have two 401k plans – one from my former day job, and a Solo 401k for my small business income. My Solo 401k is self directed and is held at Vanguard. Since it is self-directed, I cannot easily compare it to other plans within my industry. I stock it with inexpensive index funds and the employer match is whatever I decide, so it ends up being a very good plan for my needs.

I went to the BrightScope comparison page and checked out my former company’s 401k plan. It rates a 71 out of 100, compared to its peers. The highest in its peer group was a 95, the lowest was a 14 and the average was 66.

While the 401k plan offered by my former employer was above average for its peers, it wasn’t as good as I could do on my own, so I decided to roll it over into an IRA; I did the rollover at Vanguard so I could consolidate holdings at one company and reduce the number of fees I was paying. There are a lot of benefits to rolling over a 401k into an IRA, so see if this is for you.

How You Can Improve Your 401k Plan

It’s a good idea to review your 401k plan at least once a year, or any time you have a major life event, such as changing jobs, moving, having children, children moving out, a birth, death, divorce, etc. When reviewing your plan and contributions, make sure to look at your entire plan and participation level. Here are some tips for managing your 401k plan.

- Take advantage of free money. It’s a good idea to always contribute at least as much as the employer match. It’s never a good idea to leave free money on the table.

- Manage your contribution limits. You can contribute up to $17,500 this year (plus $5,000 more as a catch-up contribution if you are over age 50). Take a look at your contribution level and see if it is appropriate for your income and financial goals. See full list of 401k contribution limits for more information.

- Manage your 401k plan fees. As we mentioned earlier, you may not be able to do much about administration fees if you aren’t leaving your employer any time soon, but you can change which funds you are investing in. You can also consolidate old accounts by rolling them into your current 401k plan, or into an IRA.

- Manage your asset allocation. It’s a good idea to review your asset allocation at least once a year. Also remember to treat all of your assets and other accounts as one big bucket – don’t try to allocate your 401k separately from investments held in IRAs, taxable investments, other retirement funds etc.

If your plan is still lacking after trying these measures to control your 401k plan costs, then consider contributing money into other retirement plans, such as a Roth IRA.

-

Navigating Market Volatility with Your 401(k): A Long-Term Strategy

Making smart, confident investing decisions means having a plan — not just in the coming days but for the long term. For many individuals, this includes participating in an employer-sponsored 40

-

Socially Responsible Investing: Impact on Your Portfolio & Performance

Socially responsible investing is a hot trend for individual investors right now. In fact, according to Morgan Stanley’s Institute for Sustainable Investing’s 2019 “Sustainable Signals” survey: 75% o

invest

- Inheritance and HUD Housing: Understanding the Impact

- Using Your 401(k) for a Car: Options & Considerations

- Maximize Your Retirement Savings: A Practical Guide

- Understanding 401(k) Plans: A Comprehensive Guide

- Early 401k Withdrawal: Strategies to Avoid Penalties

- Maximize Your 401(k): Expert Investment Strategies & Planning

- 401(k) Rollover Guide: Seamlessly Transfer Your Retirement Savings

- 401(k) Rollover: Transferring Your Retirement Savings to an IRA

- Christmas Spending Trends: What You Need to Know

-

529 Plans: Using College Savings for Tuition, Private School & Student Loans

The 529 college savings plan is one of the best ways to set aside money for your children’s college education. The plan offers a host of features that make it an attractive option for savers, ...

-

Credit Score Updates: How Often Do They Occur & What Affects Them?

Credit Score Updates: How Often Do They Occur & What Affects Them?When you’re on the road to repairing your credit report, you’ll probably be excited to see how much your credit score has gone up since you started to make positive changes. Perhaps you...