Compound Interest Calculator & Retirement Savings Explained

Saving for a big goal like retirement can feel overwhelming. With tight budgets and plenty of time to kick the can down the proverbial road, saving for their golden years has become an afterthought for many.

But with Social Security income that typically only replaces about 40% of preretirement income and private-sector pensions quickly fading out of existence, more Americans are having to grapple with the reality that they’ll need to do some of their own saving for retirement.

Feeling stressed at the prospect of saving for retirement or your other long-term goals? We have good news: You don’t have to put away tons of money each month to reach your savings goals. You just have to start now and make use of a nifty little concept known as compound interest.

What Is Compound Interest?

You may have heard that when it comes to saving for retirement, the sooner you start, the better. That’s true, and not just because you’ll have more time to put money away if you start early in your career. The sooner you start putting aside money for retirement, the longer your money has to grow from compounding interest.

Compound interest is calculated at a specific frequency, such as daily or monthly, then added back to the principal (i.e. your initial investment) so the next interest calculation includes the now-larger principal. This results in exponential growth of the investment balance.

In plain English, compound interest means you earn money not just on your initial balance, but also on any interest you’ve earned. This differs from simple interest, where any interest charged isn’t added to the principal, so interest is only ever charged on the initial amount.

So, how does compound interest work in practice, and why is it so important in investing? Let’s take a look at an example.

John is looking to start saving for retirement. He’s 35 and wants to invest $100 each month into his 401(k).

John plans on retiring at age 65. His investment earns interest at a rate of 5%, compounded annually.

When John retires, he’ll have $79,727 in 401(k) savings. Not too shabby, considering he only contributed $36,000 of his own money over the years. The rest of that all comes from the increasing value of his investment and the compound interest he earned because of it.

Now, why is it so important to start saving as soon as you can? Let’s look at one of John’s younger coworkers.

Jenna is 20. Like John, she wants to get started saving for retirement. However, after looking at her budget, she can only contribute $50 each month. She also plans on retiring at age 65.

By the time Jenna retires, she’ll have a total of $95,820. Not only will she have more than John, but she will also have contributed less of her own money than he did; by the time she retires, she’ll have put only $27,000 of her own money toward her retirement.

What if Jenna had contributed $100 each month? By the time she’s ready for retirement, she’d have $191,640, with less than a third of that money coming from her own contributions. And if her company offered a 50% match on each of those $100 monthly contributions, she’d end up with a total of $287,460.

Now, John’s returns aren’t anything to sneeze at, either. The point of all this isn’t that you have to start saving for retirement at a very young age and if you don’t then you shouldn’t even bother. The important thing is that you start now.

It’s like that old saying: The best time to plant a tree was 20 years ago. The second best time is now. The same is true when it comes to compound interest.

The Compound Interest Formula

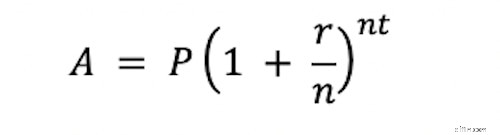

If you’re a fan of doing the math yourself, here’s an equation you can use to calculate compound interest on your own.

In this formula, “A” is the final amount you’ll end up with. “P” is the amount you started with (i.e. your principal), “r” is your interest rate, “n” is the number of times interest is compounded each year and “t” is the total number of years the amount will be invested for.

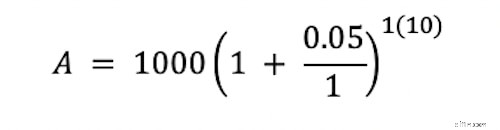

Here’s an example: You invest $1,000. You have an interest rate of 5% that compounds annually, and you want to know what your investment balance would be after 10 years.

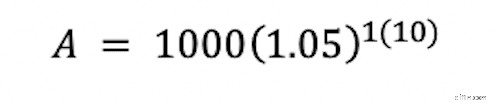

Remember high school math class? You always have to start with the stuff in the parentheses. If you divide 0.05 by 1, you get 0.05. Then, add 1.

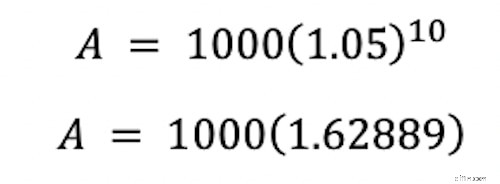

Solving the exponent is the next step.

Finally, we multiply.

After 10 years, your initial $1,000 investment will have grown to $1,628.89, without any additional work on your part.

Prefer not to do math, or have a more complex situation than what can fit in this simple formula? No worries! Input your numbers into our calculator below and we’ll show you how much your money can grow over time.

Compound Interest Calculator: Future Value Of Savings

How Does Compounding Work With Investment Returns?

Earning interest on something like a savings account is a little different from earning interest on an investment.

With a savings account, your bank might pay you a small amount of interest for keeping your money in the account. The bank will set this interest rate.

When you make an investment, the amount you earn on that investment depends on how well that investment does – which depends on a lot of different factors, including larger economic trends.

The returns you receive on investments compound as you reinvest them, much in the same way interest compounds on your savings account balance.

For example, say you buy a share of a stock for $100. The company whose stock you own has a good year, increasing in value by 10%. That means you’ve earned $10 on your investment. To compound your gains, you take that extra $10 and invest it back into your initial $100 share. When the company grows in value by another 10% the next year, you’ll earn $11 this time, thanks to your reinvestment of your previous year’s earnings. This continues exponentially until you decide to sell your share.

However, keep in mind that when you invest, this can also work in the reverse. The value of the investment could also go down, and you could lose money on your investment rather than gain it.

Summary: Invest Early And Let Your Money Grow

Looking at all the examples provided above, one thing is clear: if you’ve got some money and a lot of time, you can turn that money into even more money.

Whatever your long-term goals are – whether it be retirement, saving for a child’s college education or something else – compound interest can put your money to work and maximize the amount of money you’ll have for those goals.

Want to learn more about how to handle your personal finances? We’ve got you covered.

-

Times Interest Earned (TIE): Understanding Financial Health

Times interest earned (TIE) is a financial ratio that measures a company’s ability to meet its interest obligations based on its current income. This ratio is important to current and prospective cred

-

Understanding Medicare Tax: Definition, Rates & How It Works

What is Medicare tax and how does it work? Good question: It’s essentially defined as a payroll tax that’s applied to workers’ gross earnings and self-employe

Personal finance

- Calculating Compound Interest on a TI-83 Plus: A Step-by-Step Guide

- Understanding Short Interest: Definition & Market Implications

- Compound Interest Explained: How to Grow Your Wealth

- Compound Interest Calculator: Calculate Investment Growth

- Compound Interest: Understand the Power of Exponential Growth

- Understanding Interest: Definition, Calculation & Importance

- Compound Interest Explained: How It Works & Benefits

- Simple vs. Compound Interest: Understand the Difference & Impact

- Net Worth: Definition, Calculation & FAQs - Track Your Financial Health

-

Retirement Savings Calculator: Plan for Your Future

Retirement Savings Calculator: Plan for Your FutureIt’s never too early to begin saving for retirement! Our retirement calculator makes it easy to set and keep tabs on your retirement savings goals. Fill in the calculator with your inform...

-

Compound Interest: Formula, Calculation & Powerful Growth Explained

Compound Interest: Formula, Calculation & Powerful Growth ExplainedThere’s an urban legend that Albert Einstein once called compound interest “the most powerful force in the universe.” We can’t be sure he really said it, but the sentiment is certainly true: Compound ...