Retirement Number: Beyond the Single Figure – A Realistic Approach

When we refer to your retirement number, most people think about how much money you need to save to meet your retirement goals. Having a specific retirement number can feel comforting. It provides you with a seemingly concrete, attainable goal. But is one definitive figure truly valuable in the context of planning for retirement?

We’d love to say “yes.” But it may be an over-simplification. Identifying a perfect retirement number is just too simplistic to be realistic — at least for most people. The retirement-number concept caught on precisely because it is so simple. Who doesn’t want to plug in a number, reach that number, and then move into the golden years without a second thought?

Sorry folks, it’s usually not going to be that straightforward. It is crucially important for investors to understand the true, more complicated, nature of retirement.

Stuff Happens

Life is full of unexpected events, and that won’t change when you enter retirement. In fact, if you plan to retire at 65, you could spend 20 years or more in retirement. Just think how things can change over the span of two to three decades.

In 2001 (two decades ago from this post) the first installment of the Harry Potter film series was released and seeing it in theaters would have cost you $5.65. In 1991 – 30 years ago – the film Robin Hood: Prince of Thieves was released, and the average U.S. ticket price was $4.21. Compare that to the average price of a movie ticket today (if you even go to a movie theater in this COVID-19 world) – more than double the price at around $9.50 a movie.

Beyond inflation, there are sundry other aspects to consider. Let’s say you retire with $1 million. You’d have a very different retirement experience depending on whether the stock market crashed the day after you retired or soared for the first decade of your retirement. Likewise, health problems or family issues could change your outlook on financial security. Even overspending during the early years of your retirement could throw a wrench into your plan.

These are great examples of why the highly simplified “retirement number” can be misleading — and possibly even dangerous — to your future financial security. A much more realistic approach is required.

Introducing Monte Carlo

Monte Carlo simulations are mathematics-based analyses that attempt to make sense out of ambiguity and random variables. In other words, your retirement.

The concept of a retirement number makes planning appear to be black and white, but retirement planning is anything but. Monte Carlo simulations can help to add the necessary nuance that give you actionable knowledge.

These simulations use details based on your existing situation to analyze thousands of hypothetical retirement scenarios to determine your likelihood of success.

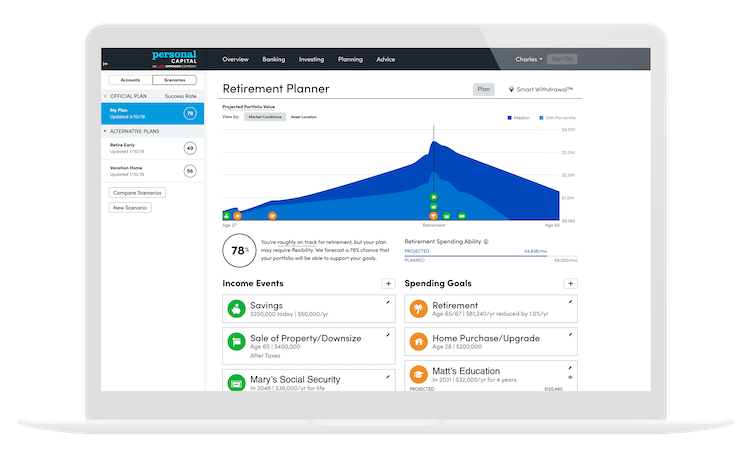

For example, let’s say you want to retire at 65, you want to maintain your current lifestyle throughout your lifetime, and you want to do so using the assets you’ve already accumulated. A Monte Carlo simulation will run thousands of hypothetical market scenarios (thereby playing out situations in which the market tanks, or roars, shortly after your retirement), and combines those market possibilities with your desired and planned cash flows. Personal Capital’s Monte Carlo software uses 5,000 scenarios. In the end, you will receive a probability-of-success ranking of low, medium, or high.

Test it out with this simplified version.

The next step is up to you. There are many individual levers you and your financial advisor can pull to make your situation one that has a higher likelihood of success. For example, you may discover that you have a medium probability of successfully meeting your retirement goals. To potentially improve your probability of success, you could:

- Delay your retirement

- Save more each year before retirement

- Reduce your planned retirement spending

- Adjust your investment strategy and risk profile in the hopes of higher returns

You could pull any or all of the levers to work towards increasing the probability that your investments sustain you throughout your retirement. Or, you can stick with your plan and acknowledge that some flexibly on your part may be required. This could mean actions such as:

- Downsizing your lifestyle later in your retirement

- Working a part-time job

- Moving in with family

The choices you make entirely depend on your personal comfort level with flexibility.

How do you run a Monte Carlo simulation on your own retirement portfolio?

You can do it easily, securely, and for free by signing up for Personal Capital’s free financial tools. Within your Dashboard, you’ll gain access to the Retirement Planner, a retirement calculator that will allow you to run a Monte Carlo simulation based on your current portfolio and other major financial events that you input (like a home purchase, when you plan to take Social Security, and more). The robust financial tools aggregate information from all of your financial accounts in one secure location. This allows you to track your net worth, budget for short-term goals, and analyze your investments.

It’s completely free and takes just a few minutes. Unlike seeing Harry Potter in the theater.

-

National Guard Retirement: Eligibility, Benefits & Pay Calculation

Army and Air Force National Guard service members become eligible for military retirement benefits at age 60. After you complete 20 years of service at this part-time job, you can collect a lifetime b

-

Financial Strategies for Your 40s: Secure Your Future

By the time you turn 40, the pace of your life is a lot different from what it was when you were fresh out of college or still figuring things out in your 30s.Your biggest concerns probably revolve a

retire

- Calculate CAGR: A Simple Guide to Compound Annual Growth Rate

- Calculate Mortgage Payments: The Bank Formula Explained

- Maximize Your Retirement Savings: A Practical Guide

- Military Retirement Pay Calculator: Understand Your Benefits

- Retirement Savings Calculator: How Much Do You Really Need?

- Protecting Your Retirement: Recession-Proofing Your Portfolio

- Protect Your Retirement: Understanding the 26(f) Program

- IRA Investment Strategies: Maximize Your Retirement Growth

- Planning for Your Parents' Retirement: A Comprehensive Guide

-

Understanding Your Postal Retirement: A Guide to FERS & Benefits

Understanding Your Postal Retirement: A Guide to FERS & BenefitsThe U.S. Postal Service is covered, as are all federal nonmilitary agencies, under the Federal Employment Retirement System (FERS), which pays all of its employees a pension in accordance with how muc...

-

Federal Retirement Pay: A Comprehensive Calculation Guide

Federal Retirement Pay: A Comprehensive Calculation GuideThe U.S. government offers retirement benefits to its employees that aim to compete with private sector retirement benefits. Federal pensions depend on your career, years of service and age. They also...