Understanding Stale-Dated Checks: Expiration Dates & What to Do

While running errands this afternoon, I stopped by the bank to deposit a check. All of the tellers were occupied with difficult clients. (I’m old-fashioned and go inside to make deposits for my business finances.) While I waited, I eavesdropped on the nearest conversation. A woman was frustrated because she’d just opened a checking account a few weeks ago, and now it was overdrawn. She couldn’t understand. “I don’t see how that’s possible,” she said.

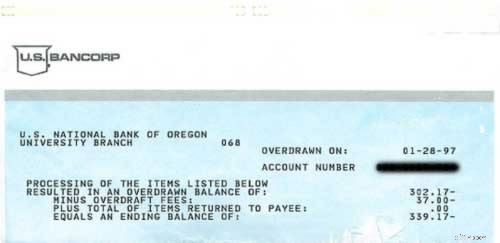

The teller was very patient and very polite. She tried to help the woman figure out where the problem was. Together, they went through the woman’s checkbook register and compared it to the bank’s computer. Finally, they discovered the culprit: a $50 check the woman had written on June 21st.

“They deposited that?” the woman said.

“Yes,” said the teller.

“Wow,” the woman said. “It had been so long that I thought they must have lost it. I’ve already used that money for something else.”

The teller didn’t say anything.

“Can they really take that long to deposit a check?” the woman asked.

“Yes, ma’am,” said the teller.

Introduction to Stale-Dated Checks

Stale-dated checks are a frequent concern in both personal and business transactions. A stale-dated check is simply a check that has not been cashed or deposited within a certain period—most commonly six months (or 180 days) from the date written on the check.

After this time frame, financial institutions are not required to honor the check, which can create confusion and inconvenience for both the person who wrote the check and the recipient.

Understanding what makes a check stale-dated, how financial institutions handle these situations, and the potential consequences is essential for smooth transactions and avoiding unnecessary headaches.

What are the Laws?

In my younger days, I had similar experiences (though never with checks that were just a few weeks old). I’d write a check, and it would remain un-deposited for several months. What a dilemma! Should I use the money to buy comic books? Or should I keep it in my account in case the check actually goes through? Because I toed the line so close to zero, the answer was important. Different banks and states have different rules regarding how long a check remains valid, so it’s important to understand the specific policies that apply to your situation.

In my case, every check was eventually deposited, and funds were withdrawn from my account. This hurt me twice because I, too, had added the money back into my checkbook. Dumb, but true.

When I got home today, I looked up the actual law on stale checks. It turns out that a bank can pay or return an old check as it sees fit. According to the United States Uniform Commercial Code, a bank is not obliged to pay a check more than six months old. Here’s the full text of the guideline:

A bank is under no obligation to a customer having a checking account to pay a check, other than a certified check, which is presented more than six months after its date, but it may charge its customer’s account for a payment made thereafter in good faith.

This means there is a time limit for cashing checks, typically based on the date issued. The time limit determines when a check becomes stale and whether it can still be processed.

In other words, the bank isn’t required to pay a check more than six months old. But it can if it wants. Generally speaking, banks may reject a check that is presented after a certain timeframe, but some may still process it depending on their rules.

In other words, the bank isn’t required to pay a check more than six months old. But it can if it wants. The bottom line? If you have a stale check outstanding, contact your bank to determine their policy. Don’t just assume the funds are free to be spent.

I’m not sure what happened with the woman at my bank today. When I became impatient and left, the manager was helping her. It sounded as if they were going to waive the overdraft fee, but there was nothing they could do about the fact that the woman was still thirty or forty dollars short in her account. State laws may also affect how banks handle overdrafts and stale checks.

Risks of Stale Checks

Letting a check go uncashed for too long can lead to a variety of problems. Once a check is considered stale, a financial institution may refuse to process it, leaving the recipient without the expected funds. If a stale check is deposited and the issuing bank no longer has sufficient funds in the account, the check may bounce, resulting in insufficient funds fees for the issuer and possible returned check fees for the recipient.

There’s also the risk that uncashed checks may eventually be classified as unclaimed property, requiring the funds to be turned over to the state. This escheatment process can make it difficult for the rightful owner to recover the money. To avoid these risks, it’s important to keep track of issued and received checks, and to act within the appropriate time frame.

Best Practices for Handling Stale-Dated Checks

To avoid the complications that come with stale-dated checks, it’s wise to adopt a few best practices. Always check the date on any check you receive and deposit it as soon as possible—don’t let it sit forgotten in a drawer. If you’re the one writing the check, communicate with recipients to confirm that checks have been received and deposited, and don’t hesitate to reissue a check if necessary.

Embracing direct deposit and electronic payments can also help reduce the risk of stale checks altogether. By staying organized and proactive, both sides can avoid the headaches of dealing with stale-dated checks and ensure that payments are processed smoothly and on time.

Frequently Asked Questions

How long are personal checks good for?

Personal checks are typically valid for six months from the date written on the check. However, while most personal checks expire after six months, certain types of checks, such as payroll checks or government-issued checks, may be valid for up to one year. After that, banks may consider the cheque ‘stale-dated’ and may not honour it. However, policies can vary from bank to bank, so it’s always advisable to cash or deposit cheques as soon as possible.

How long is a business check good for?

Just like personal checks, business checks are generally good for six months from the date written on the check. Small business owners should be aware that different rules may apply to business checks, especially payroll checks, depending on the bank or state. After this period, they can be considered ‘stale-dated’. Different banks, however, may have different policies regarding stale-dated business checks, so it’s best to check with your bank.

Can I cash a check from 2 years ago?

In most cases, a check will be considered ‘stale-dated’ if it’s more than six months old and banks are not obliged to cash or deposit it. Therefore, a check that is two years old is very likely to be declined by the bank. It might be best to contact the issuer and request a new check.

If a check remains an uncashed check for an extended period, the funds may be passed to the state as unclaimed property. In such cases, the payee may need to file a claim with the state or request that the check be re issued by the original issuer.

Can you still cash a check after the void date?

No, once a check has reached its void date, also known as the expiration date, it can no longer be cashed or deposited. The void date is usually indicated on the check by the issuer, serving as a deadline for when the check must be cashed. If you try to cash a check after its void date, it will most likely be declined by the bank.

-

Disintermediation: Definition, Benefits & Examples

Disintermediation is the removal of different elements within the middle of a supply chain. The intermediaries in product development – or “middlemen” – are removed from the su

-

Pet-Friendly Home Renovations: Boost Your Home's Value & Appeal

div.cust

Savings

- Calculate Your Annual Income: A Simple Step-by-Step Guide

- Laundry Savings: A Simple Way to Save Money

- Boost Your Savings: 4 Reasons to Choose a High-Yield Savings Account

- Debt Payoff vs. Saving: Which Should You Prioritize?

- Buy Now, Save Later: Understanding the Pros & Cons of BNPL vs. Saving

- Finding Profitable Stocks: A Guide to Stock Market Investing

- Boost Your Savings: 5 Simple Strategies for Long-Term Wealth

- Claim Your Unclaimed Stimulus Check: $1,200 CARES Act Payment

- High-Yield Savings Accounts: 5 Smart Use Cases

-

Simple Budgeting Strategies: Achieve Your Financial Goals

Simple Budgeting Strategies: Achieve Your Financial GoalsOne change helped get me on track. ...

-

Cross-Currency Transactions: Definition & How They Work

Cross-Currency Transactions: Definition & How They WorkA cross currency transaction involves the use of more than one currency. For example, you may be involved in a cross currency transaction in order to convert one currency into another currency. Previo...