Understanding 2/10 Net 30: Trade Credit Explained

2/10 Net 30 refers to the trade creditTrade CreditA trade credit is an agreement or understanding between agents engaged in business with each other that allows the exchange of goods and services offered to a customer for the sale of goodsCost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct or services. 2/10 net 30 means that if the amount due is paid within 10 days, the customer will enjoy a 2% discount. Otherwise, the amount is due in full within 30 days.

Example of a Trade Credit

The CEOCEOA CEO, short for Chief Executive Officer, is the highest-ranking individual in a company or organization. The CEO is responsible for the overall success of an organization and for making top-level managerial decisions. Read a job description of Company A faces decreasing sales due to fierce competition in the marketplace. The CEO believes that the reason sales are declining is due to the company not offering trade credits. In fact, Company A is the only company in the industry that does not offer trade credits to customers. Then Company A sets up a new trade credit term for customers – 2/10 net 30. Customers who purchase on credit are given 30 days to settle their obligationAccounts PayableAccounts payable is a liability incurred when an organization receives goods or services from its suppliers on credit. Accounts payables are. However, if paid within 10 days, customers enjoy a 2% discount on the goods purchased.

If a customer purchases $10,000 from Company A on the terms 2/10 net 30 and pays within 10 days, the customer only needs to pay $10,000 x 0.98 = $9,800. On the other hand, if the customer pays after 10 days, he must pay the full amount of $10,000.

Journal Entries for Trade Credit

There are two methods of accounting for discounts: Net method and Gross method.

Let us consider the following example:

A customer of Company A, realizing that the company is offering credit terms of 2/10 net 30, decides to make a purchase of $1,000. The net method and gross method journal entries are provided below:

The net method records the receivables at the sale price less the cash discount. The company would need to make an adjustment for the interest earned if the customer does not take advantage of the discount.

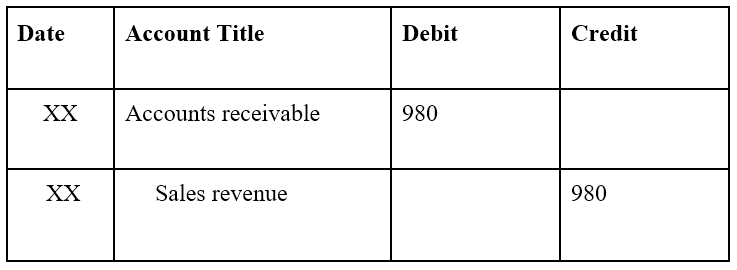

The initial journal entry:

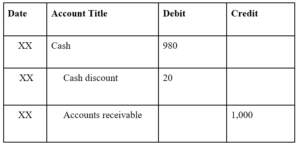

Note: $1,000 x 0.98 = $980. The net method records the receivables at the sale price less the cash discount.

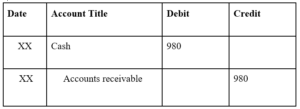

If the customer pays within 10 days and takes advantage of the 2% discount:

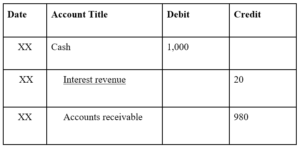

If the customer pays after 10 days and does not take advantage of the 2% discount:

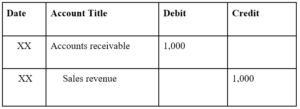

The gross method records the face value of receivables. If the customer takes advantage of the discount, the company will reduce its revenue in the income statement.

The initial journal entry:

Note: The gross method records the receivables at face value.

If the customer pays within 10 days and takes advantage of the 2% discount:

Note: Cash discount goes on the income statement to reduce revenue.

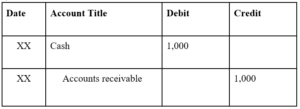

If the customer pays after 10 days and does not take advantage of the 2% discount:

The Importance of Offering Trade Credit

From a supplier’s perspective, trade credit is offered to facilitate more frequent and higher volume purchases. The flexibility in the time of payment attracts more customers and generates more sales for the company.

From a purchaser’s perspective, trade credit allows buyers to make purchases without immediately parting with their cash. Therefore, it also offers flexibility in that buyers can make purchases when there is no cash on hand.

The Risk in Offering Trade Credit

The biggest risk to a supplier when offering trade credit is the potential for bad debt. Since cash does not immediately switch hands in a purchase, the buyer may end up not paying for the purchases. When companies offer trade credit, an allowance for doubtful accounts is set up to anticipate the amount of bad debts from credit purchases.

Additional Resources

CFI is the official provider of the global Financial Modeling and Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional free CFI resources below will be useful:

- Sale and Purchase AgreementSale and Purchase AgreementThe Sale and Purchase Agreement (SPA) represents the outcome of key commercial and pricing negotiations. In essence, it sets out the agreed elements of the deal, includes a number of important protections to all the parties involved and provides the legal framework to complete the sale of a property.

- Revolving Credit FacilityRevolving Credit FacilityA revolving credit facility is a line of credit that is arranged between a bank and a business. It comes with an established maximum amount, and the

- Accounts ReceivableAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow

- Credit SalesCredit SalesCredit sales refer to a sale in which the amount owed will be paid at a later date. In other words, credit sales are purchases made by

-

Understanding Forced Credit Card Payments: What You Need to Know

What Does it Mean to Force a Credit Card Payment? When you swipe your credit card at a restaurant or store, you are electronically authorizing the credit card company to lend you the money fo

-

Understanding Credit Card Referral Responses in Processing

What Does Referral Mean in Credit Card Processing? A referral is a response received on a credit card terminal after a credit card is swiped for authorization. The response does not mean the

Accounting

- Credit Card Validation: A Comprehensive Guide for Businesses

- Understanding Credit Lines on Credit Cards: Limits & Usage

- Understanding Credit Adjustments (CR) on Your Credit Card Statement

- Understanding 'NR' on Your Credit Report: What Does It Mean?

- Understanding 'MR' on Your Credit Report: What It Means

- Understanding 'HC' on Your Credit Report: What Does It Mean?

- Understanding Net Monthly Income: Definition & Calculation

- Understanding the R9 Credit Score Code: What It Means & Implications

- Understanding Premium & Discount to Net Asset Value (NAV) in Mutual Funds

-

Foreclosure Redeemed: Understanding the Impact on Your Credit Report

Foreclosure Redeemed: Understanding the Impact on Your Credit ReportWhat Does Foreclosure Redeemed Mean on a Credit Report? In many states, when a mortgage lender forecloses on a home or other property, the owner gets one last chance to stop the process by im...

-

Net Worth Explained: Understanding Your Financial Health

Net Worth Explained: Understanding Your Financial Health...