Calculate Free Cash Flow to Equity (FCFE) from Net Income: A Step-by-Step Guide

Free Cash Flow to Equity (FCFE)Free Cash Flow to Equity (FCFE)Free cash flow to equity (FCFE) is the amount of cash a business generates that is available to be potentially distributed to shareholders. It is calculated as Cash from Operations less Capital Expenditures. This guide will provide a detailed explanation of why it’s important and how to calculate it and several can be calculated using net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through as well as using the Free Cash Flow to the Firm (FCFF) formulaFree Cash Flow to Firm (FCFF)FCFF, or Free Cash Flow to Firm, is cash flow available to all funding providers in a business. debt holders, preferred stockholders, common shareholders. It is the amount of cash generated by a company that can be potentially distributed to the company’s shareholders. When using an intrinsic valuation method such as the Discounted Cash Flow (DCF) valuation modelDiscounted Cash Flow DCF FormulaThis article breaks down the DCF formula into simple terms with examples and a video of the calculation. Learn to determine the value of a business., an analyst can use FCFE as the business’ cash flowCash FlowCash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period. There are many types of CF generating ability.

The FCFE is different from the free cash flow to the firm (FCFF), which indicates the amount of cash generated to all holders of the company’s securities (both investors and lenders).

FCFE from Net Income Formula

Free cash flow to equity (FCFE) can be calculated in many ways. To calculate the FCFE from net income, we need to look at the formula and break it down. Here is the formula to calculate FCFE from net income:

FCFE = Net Income + Depreciation & Amortization – CapEx – ΔWorking Capital + Net Borrowing

However, FCFE is usually derived by using the free cash flow to the firm (FCFF) formula. To reconcile this, let’s look at how we get FCFE from FCFF. Here is the formula for FCFF:

FCFF = Net Income + Depreciation & Amortization – CapEx – ΔWorking Capital + Interest Expense (1 – t)

Where:

- FCFF – Free Cash Flow to the Firm

- CapEx – Capital Expenditure

- ΔWorking Capital – Net change in the Working Capital

- t – Tax rate

Notice that FCFE and FCFF share very similar terms such as depreciation, capital expenditures, and changes in working capital. The main difference between the FCFF and FCFE is the impact of interest expenses and their tax shieldsTax ShieldA Tax Shield is an allowable deduction from taxable income that results in a reduction of taxes owed. The value of these shields depends on the effective tax rate for the corporation or individual. Common expenses that are deductible include depreciation, amortization, mortgage payments and interest expense. Therefore, the FCFE can be calculated using the FCFF formula:

FCFE = FCFF + Net Borrowing – Interest Expense (1 – t)

FCFE from Net Income Formula and Financial Statements

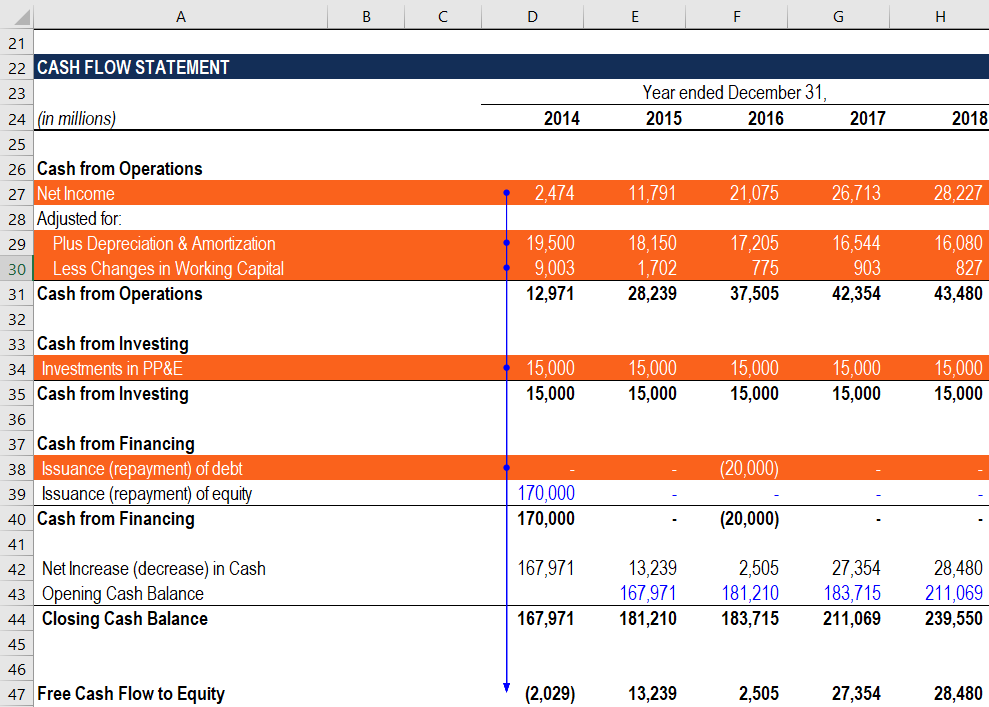

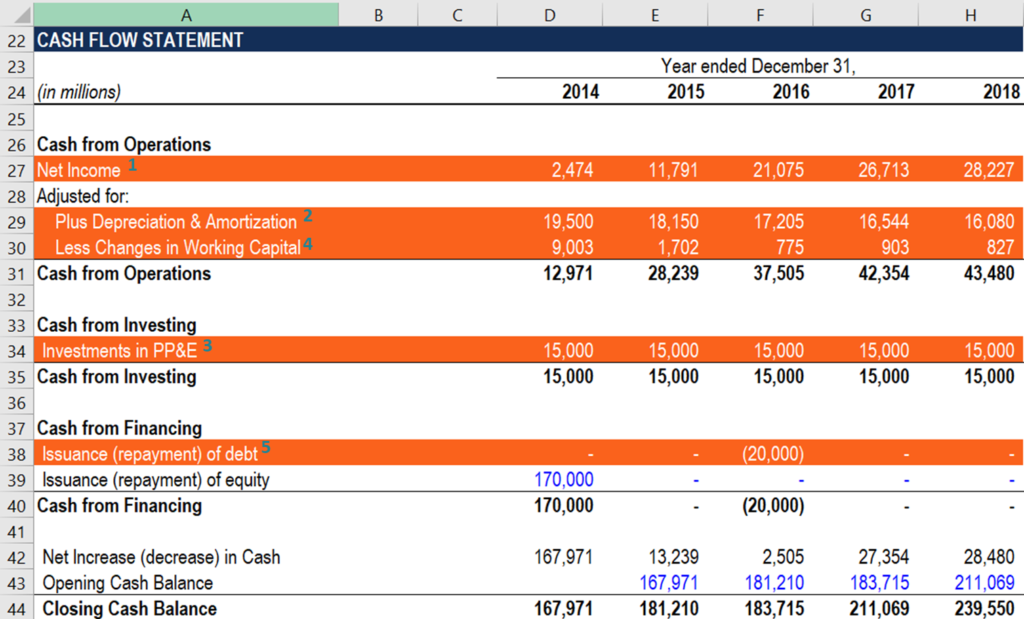

An analyst who calculates the free cash flows to equity in a financial model must be able to quickly navigate through a company’s financial statements. The primary reason is that all the inputs required for the calculation of the metric are taken from the financial statements. The guidance below will help you to quickly and correctly incorporate the FCFE from Net Income calculation into a financial model.

- Net Income: Net income (also referred to as the net earnings) can be found at the bottom of the income statement. In addition, the net income is listed on the cash flow statement in the calculation of the cash flows from operating activities. Every calculation of the cash flow from operating activities starts with the net income. Since many other inputs are taken from the cash flow statement as well, it is recommended to use the financial statement to link the net income to the FCFE calculations.

- Depreciation & Amortization: The depreciation and amortization expense is recorded on the company’s income statement under the Expenses section. The section follows the company’s gross profit. Similar to net income, the depreciation and amortization expense is also listed on the cash flow statement on the Cash from Operations section.

- CapEx: The capital expenditure (CapEx) can be found on the cash flow statement within the Cash from Investing section.

- Change in working capital (can also be denoted as ΔWorking Capital) is calculated in the company’s cash flow statement within the Cash from Operations section.

- Net debt: The net debt amount is also located on the cash flow statement under the Cash from Investing section.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Capital ExpenditureCapital ExpenditureA capital expenditure (“CapEx” for short) is the payment with either cash or credit to purchase long term physical or fixed assets used in a

- How the 3 Financial Statements are LinkedHow the 3 Financial Statements are LinkedHow are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and

- Projecting Income Statement Line itemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Owner’s EquityOwner’s EquityOwner's Equity is defined as the proportion of the total value of a company’s assets that can be claimed by the owners (sole proprietorship or partnership) and by the shareholders (if it is a corporation). It is calculated by deducting all liabilities from the total value of an asset (Equity = Assets – Liabilities).

-

Calculate Your Annual Household Income: A Simple Guide

If you want to determine your eligibility for certain government programs, you need to know your annual household income. The federal government has several definitions of annual household income. For

-

Cashing a PayPal Check: A Step-by-Step Guide

Although PayPal offers a method of direct deposit from the available funds in your account to your bank account, some people would prefer to have a paper trail. So they request a check be mailed. Cash

Accounting

- Calculating Income from Discontinued Operations: A Comprehensive Guide

- Calculate Net Income: A Balance Sheet Guide

- Net Increase Calculation: Understanding & Formula

- Net Rental Income: Calculation & Tax Reporting for Landlords

- Net Income: Definition, Calculation & Importance for Business

- Calculating Free Cash Flow to Equity (FCFE): A Comprehensive Guide

- Calculating Free Cash Flow to Equity (FCFE) from EBITDA: A Step-by-Step Guide

- Calculating Cash Flow from Investing Activities: A Step-by-Step Guide

- Calculate Your Net Income: A Simple 4-Step Guide

-

Understanding Aggregate Income: A Comprehensive Guide

Understanding Aggregate Income: A Comprehensive GuideYour aggregate income is the total income for a couple filing a joint return. Your aggregate income is your gross income, and the term generally refers to the combined incomes of a couple fil...

-

Net Return Calculation: A Comprehensive Guide for Investors

Net Return Calculation: A Comprehensive Guide for InvestorsHigher net returns indicate better-performing investments. Investors use net returns to calculate the return on their investments after all expenses and profits have been included. For exampl...