Master Limited Partnerships (MLPs): Definition & Key Features

A master limited partnership is a publicly-traded business venture that combines the features of a corporationCorporationA corporation is a legal entity created by individuals, stockholders, or shareholders, with the purpose of operating for profit. Corporations are allowed to enter into contracts, sue and be sued, own assets, remit federal and state taxes, and borrow money from financial institutions. with that of a partnership and exists as a publicly-traded limited partnership. Such business ventures are exempt from corporate tax. A master limited partnership pools the tax benefits of a private partnership and liquidity of a publicly-traded business.

Summary

- A master limited partnership is a hybrid business venture that combines the features of a corporation and a limited partnership.

- Master limited partnerships are not required to pay federal tax.

- They must receive at least 90% of their income from qualifying sources to obtain the tax benefits.

Features of a Master Limited Partnership

- A master limited partnership is not considered a separate legal entity like a corporation – rather, it is treated as an aggregate of existing partners.

- These partnerships issue “units” similar to partnerships instead of shares; however, the units can be traded on a national stock exchange.

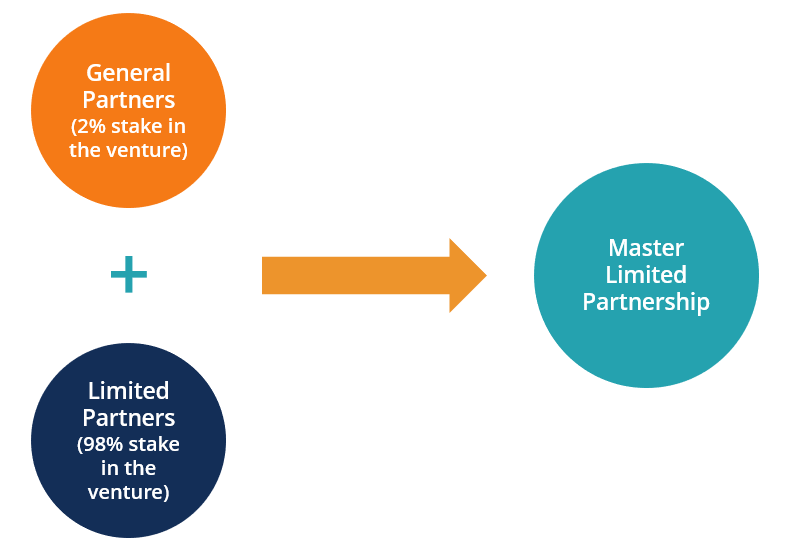

- There are two types of partners in such business ventures – general partners and limited partners.

- The general partners are responsible for the daily activities of the business, while the limited partners are the ones who invest in the business. The limited partners are called unitholders.

- Limited partners receive cash distributions that are treated as a return of capital, whereas general partners obtain compensation based on the performance of the business.

Tax Exemption Feature of a Master Limited Partnership

A master limited partnership receives the tax benefit features of a limited partnership, wherein the businesses are exempted from paying the corporate tax on their revenues. The unitholders, however, pay the tax on the portion of their partnerships’ earnings.

Hence, these businesses are not liable for double taxation as corporations are – corporate tax by the business on its revenue and personal tax by the shareholders on the income from the holdings. This implies that a master limited partnership pays higher yields than a traditional stock, as, due to the tax exemption, more money is available for distribution to unitholders.

Restrictions

Since master limited partnerships do not pay federal taxes, certain restrictions are put in place by the U.S. government to curtail the loss of corporate tax revenue. Hence, to obtain the tax benefits, a master limited partnership should receive 90% or more of its income from qualifying sources.

Income realized from real estate, exploration, transporting natural resources, and processing of goods are all considered as qualified income. Therefore, a company can derive at most 10% of the income from sources such as commoditiesCommoditiesCommodities are another class of assets just like stocks and bonds. Most commodities are products that come from the earth that possess and natural resources. The criterion limits the sectors that master limited partnerships can operate in.

Advantages of a Master Limited Partnership

- A master limited partnership provides investors with consistent distributions. Additionally, the investments are low-risk, implying that the investors receive a stable income over the investment period.

- Almost 80% of the distributions from such partnerships are tax-deferred. This means that the investors are not liable to pay tax until their portion is sold. It also offers tax benefits, as when the unitholders sell their portion, they pay taxes at the capital gains rate instead of the personal income tax rate, which is usually higher.

- The investors receive more income yield than with traditional equities – generally in the range of 6%-7%.

- The tax exemption feature results in more capital, which can be used in future projects.

Disadvantages

- Since master limited partnerships are in industries with slow growth, such as exploration, there is a slow return on investments.

- The corporate tax liability is passed on to the investors, which can negatively affect their return.

- The process of filing taxes may become complicated if the limited partners own units in various states where the partnership operates.

- There is a smaller pool of investors for master limited partnerships, as institutional investors incur tax liabilities for investing in units.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful:

- Corporate StructureCorporate StructureCorporate structure refers to the organization of different departments or business units within a company. Depending on a company’s goals and the industry

- Limited Liability Partnerships (LLPs)Limited Liability Partnerships (LLPs)Limited Liability Partnerships (LLPs) are a corporate business structure that enables entrepreneurs, professionals, and enterprises to provide services via

- Institutional InvestorInstitutional InvestorAn institutional investor is a legal entity that accumulates the funds of numerous investors (which may be private investors or other legal entities) to

- Professional CorporationsProfessional CorporationsA professional corporation is a corporation that comprises different types of professionals such as doctors, lawyers, or accountants. In most states, professionals who want to incorporate their practice can do so by forming a corporation or service corporation.

-

Understanding Income Tax Payable: A Guide for Businesses

Income tax payable is a term given to a business organization’s tax liability to the government where it operates. The amount of liability will be based on its profitability during a given perio

-

Understanding Net of Tax: Definition & Calculation

Net of tax is the amount obtained after the applicable tax is deducted from the gross incomeGross IncomeGross income refers to the total income earned by an individual on a paycheck before taxes and o

Business strategy

- Understanding Limited Partnership Interests: Roles & Liabilities

- Franchise Tax Explained: What It Is & Who Pays

- Understanding Income Tax: A Comprehensive Guide for Individuals & Businesses

- Understanding Taxation: A Comprehensive Guide to Government Revenue

- Progressive Tax Explained: How It Works & Examples

- Regressive Taxes: Definition, Examples & Impact on Income Inequality

- Tax Depreciation Explained: A Comprehensive Guide for Taxpayers

- Family Limited Partnerships (FLPs): A Comprehensive Guide

- Understanding Business Partnerships: Types, Liability & Formation

-

Understanding Federal Income Tax: A Comprehensive Guide

Understanding Federal Income Tax: A Comprehensive GuideIn many countries, taxes are imposed at the federal, state/provincial, and local level. The income tax that one pays at the federal level is determined by applying a predetermined rate to the earnings...

-

Understanding Horizontal Equity in Taxation

Understanding Horizontal Equity in TaxationHorizontal equity is an economic theory that is used to assess the fairness of tax burden across a population. The theoretical underpinning of horizontal equity is that the amount of taxes paid should...