Understanding Bank Ratings: A Guide to Financial Stability

Bank rating is a measure of financial soundness for banks. Just like credit agencies such as Standard & Poor’s (S&P)S&P – Standard and Poor'sStandard & Poor’s is an American financial intelligence company that operates as a division of S&P Global. S&P is a market leader in the, Moody’s, and Fitch that give credit ratings to individual consumers and corporations, the Federal Deposit Insurance Corporation (FDIC) assigns credit ratings to banks and other financial institutions.

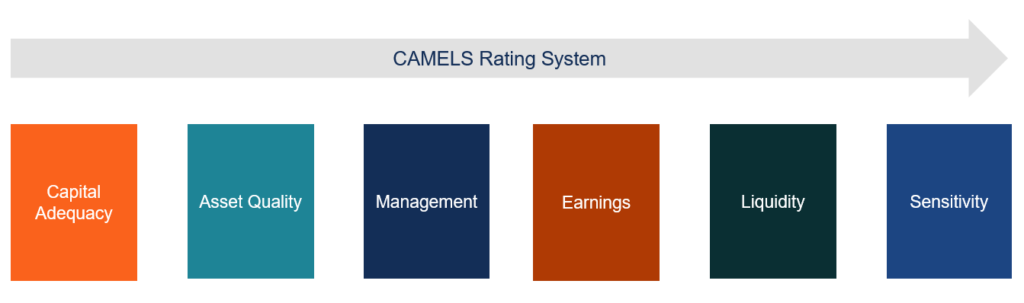

Bank ratings are generally between 1 and 5 – with 1 being the best and 5 being the worst. Bank ratings are computed using the CAMELS rating systemCAMELS Rating SystemThe CAMELS Rating System was developed in the United States as a supervisory rating system to assess a bank's overall condition. CAMELS is an acronym that, a globally recognized rating system that measures the financial soundness of financial institutions based on six factors.

What are the Six Components of the CAMELS Rating System?

1. Capital Adequacy

Capital adequacy measures cash reserves of banks and financial institutions relative to the minimum capital requirements set by regulatory authoritiesSecurities and Exchange Commission (SEC)The US Securities and Exchange Commission, or SEC, is an independent agency of the US federal government that is responsible for implementing federal securities laws and proposing securities rules. It is also in charge of maintaining the securities industry and stock and options exchanges.

To get a high rating on capital adequacy, financial institutions must be well within the minimum capital requirements set by the regulators. Institutions must also meet all other requirements set by regulatory agencies, including guidelines and regulatory policies related to interest and dividends.

2. Asset Quality

Asset quality measures the quality of a bank’s loans and other assets based on both credit and market risk. It involves identifying and rating potential risk factors relative to the capital earnings generated. Credit risk is measured by assessing the quality of loans and credit worthiness of borrowers.

Investments in government bonds and loans to corporations with high credit ratings are considered safe, while corporate loans to companies with low credit ratings are considered low-quality loans. The Federal Deposit Insurance Corporation (FDIC)Federal Deposit Insurance Corporation (FDIC)The Federal Deposit Insurance Corporation (FDIC) is a government institution that provides deposit insurance against bank failure. The body was created emphasizes measuring the quality of loans as these provide the main source of income for banks.

The asset quality rating also measures market risk by evaluating how a bank’s market value of investments will change under different economic environments. It involves stress testing the market value of securities to changes in key economic indicators, such as interest rates and inflation.

3. Management

Management measures the management’s ability to run the day-to-day operations, execute key functions, and adapt to changing market conditions to manage investment risk factors. It also involves an internal review of management policies to ensure that they comply with regulatory guidelines.

4. Earnings

Earnings measures a bank’s ability to consistently generate stable earnings on a risk-adjusted basis. A bank generates earnings by capturing the difference in the spread between the rate at which it lends and the rate at which it pays on deposits.

The ability of a bank to consistently grow its earnings and deposits is a key determinant of its future viability and prospects. Regulators measure the quality of earnings by assessing the bank’s growth in deposits, balance sheet stability, quality of loans, and interest rate spread.

5. Liquidity

Liquidity measures a bank’s ability to meet its short-term obligations, including withdrawal of deposits. It involves identifying assets that can be easily converted into cash.

Regulators assess liquidity by evaluating the amount and quality of liquid assets relative to the short-term obligations of the institution. The liquidity coverage ratio is used to assess whether the bank holds enough liquid assets. Generally, only high-quality liquid assets are considered for this analysis.

6. Sensitivity

Sensitivity measures how sensitive a bank’s earnings are to particular risk factors. Regulators use the sensitivity information to understand how the exposure of the institution is distributed among specific industries. The information is then used to assess how lending capital to specific industries can impact the bank’s income and credit risk.

The sensitivity rating also assesses income sensitivity based on exposure to volatility in foreign exchange, commodities, equities, and derivative markets.

Interpreting Bank Ratings

The FDIC assigns a bank rating between 1 and 5 based on the CAMELS assessment framework. A rating of 1 or 2 is assigned to financial institutions that are strong on all six aspects of the CAMELS framework. The institutions are generally considered to be in a sound financial position.

A rating of 3 is considered satisfactory and indicates that no major issues are facing the bank in question. Banks that are assigned ratings of 4 or 5 are generally considered to be in danger. Such banks need to take immediate action and require careful monitoring.

Finally, financial institutions that are assigned a rating of 5 demonstrate a high probability of declaring bankruptcy in the next 12-24 months.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful:

- Banking FundamentalsBanking FundamentalsBanking fundamentals refer to the concepts and principles relating to the practice of banking. Banking is an industry that deals with credit

- Credit RatingCredit RatingA credit rating is an opinion of a particular credit agency regarding the ability and willingness an entity (government, business, or individual) to fulfill its financial obligations in completeness and within the established due dates. A credit rating also signifies the likelihood a debtor will default.

- Rating AgencyRating AgencyA rating agency assesses the financial strength of companies and government entities, especially their ability to meet principal and interest payments

- Sensitivity AnalysisWhat is Sensitivity Analysis?Sensitivity Analysis is a tool used in financial modeling to analyze how the different values for a set of independent variables affect a dependent variable

-

Original Bank Statement: Definition & How to Obtain

Many adult consumers have at least one bank account for saving money, writing checks or keeping money safe until using it to pay bills. Banks issue statements for their customers to keep records and t

-

Understanding Payable-on-Death (POD) Bank Accounts: A Comprehensive Guide

A POD account is a way to ensure that your money goes to designated people in the event of your death. A POD bank account, also known as payable-on-death, allows you to appoint someone to rec

finance

- Understanding B Credit Ratings: What They Mean for Businesses

- Understanding Bank Loans: Types, Terms & How They Work

- Understanding Bank Overdrafts: Causes, Costs & Solutions

- Bank Drafts: Definition, How They Work & Usage

- Bank Line of Credit (LOC): Definition & How It Works

- Understanding Bank Statements: A Comprehensive Guide

- Bank Stress Tests: Understanding Financial Resilience

- Commercial Banks: Definition, Services & Bridge Loans

- Understanding Bank Statements: A Comprehensive Guide

-

Understanding A1 Credit Ratings: A Guide to Financial Strength

The term A-1 or A1 credit is a rating of financial strength of companies and other entities issuing bonds and other forms of debt. The exact meaning of the term varies, but is a general indication of ...

-

Understanding Bank Adjustments: What They Are & Why They Happen

Understanding Bank Adjustments: What They Are & Why They HappenEveryone occasionally makes mistakes, even the friendly experienced professionals at your local bank branch. Sometimes, even the technology they use creates errors. When that happens, your bank will m...