Bullet Loan Explained: Structure, Risks & Benefits

A bullet loan is a type of loan in which the principal that is borrowed is paid back at the end of the loan term. In some cases, the interest expenseInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also is added to the principal (accrued) and it is all paid back at the end of the loan. This type of loan provides flexibility to the borrower but it is also risky. In a debt scheduleDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows, periodic expenses would only consist of interest expense and no principal payment, as this is consolidated at maturity.

All of these terms essentially mean that a borrower is going to be making a large payment only at the end of the repayment term. With a bullet loan, borrowers can sometimes get access to loans they would not be able to afford as a regular, long-term loan with a monthly payment schedule.

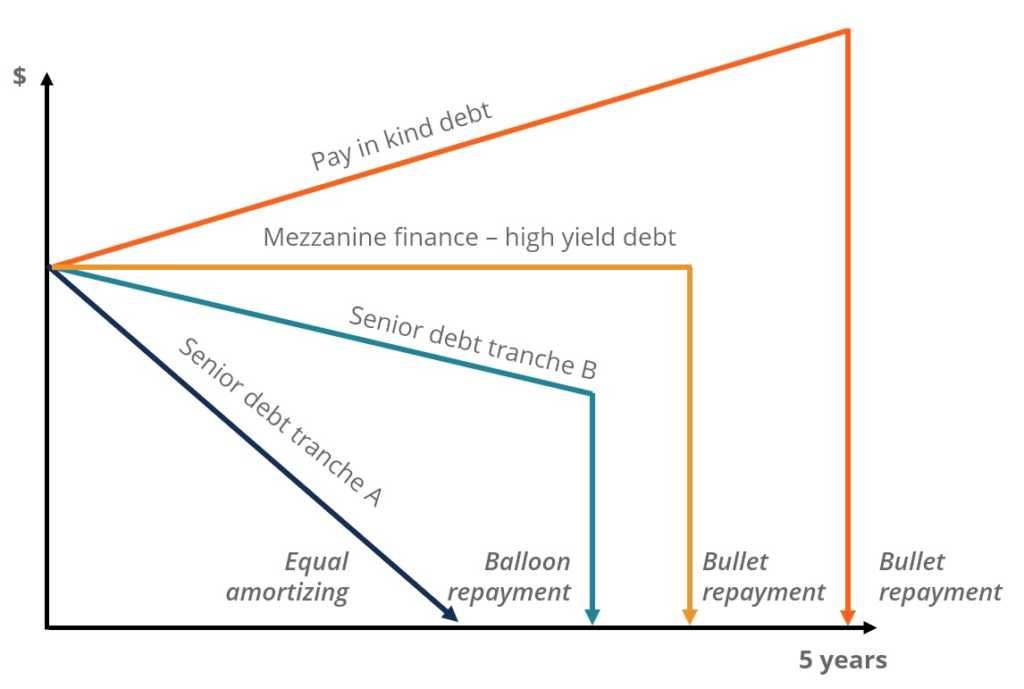

Below is an example of principal repayment profiles for various different types of loans.

Source: CFI’s Free Corporate Finance Course.

Advantages of Bullet Loans

One of the primary advantages of this type of loan is that it provides flexibility to the borrower. When an individual is trying to shop for a loan, he or she might find that the loan payments are too high to afford. By getting a bullet loan, the individual can significantly reduce the amount of money that will be due on each payment. In many cases, the borrower is only going to have to pay for the interestSimple InterestSimple interest formula, definition and example. Simple interest is a calculation of interest that doesn't take into account the effect of compounding. In many cases, interest compounds with each designated period of a loan, but in the case of simple interest, it does not. The calculation of simple interest is equal to the principal amount multiplied by the interest rate, multiplied by the number of periods. that is accruing during each period.

A bullet loan will sometimes also include the interest that is accruing in the amount that is due at the end of the loan. When this happens, the borrower is not going to have to make any payments until the end of the loan. This type of loan is less common, but it can be used in some circumstances. It is most appropriate when the borrower does not want to be burdened with high monthly loan payments now but has a reasonable expectation of receiving the necessary cash flow to repay the loan by the end of the loan term.

Disadvantages of Bullet Loans

Even though a bullet loan can be beneficial, it is also extremely risky.Risk Averse DefinitionSomeone who is risk averse has the characteristic or trait of preferring avoiding loss over making a gain. This characteristic is usually attached to investors or market participants who prefer investments with lower returns and relatively known risks over investments with potentially higher returns but also with higher uncertainty and more risk. Many borrowers have faced issues with this type of loan after getting involved with one. One of the biggest problems is that many borrowers do not make the proper arrangements to be able to make the balloon payment at the end of the loan term.

The balloon payment comes due and the borrower does not have the money to pay it. In that case, the lender will foreclose on any property that is securing the loan.

Bullet loans are also refinanced quite frequently. Borrowers often use the loan to get quick access to the money they need. They then take advantage of the small monthly payments associated with the bullet loan. When the balloon payment comes due, they will refinance into another loan.

Additional Resources

Thank you for reading the CFI guide to bullet loans and their pros/cons. CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level.

To keep learning and advancing your career, the following resources will be helpful:

- Bridge LoanBridge LoanA bridge loan is a short-term form of financing that is used to meet current obligations before securing permanent financing. It provides immediate cash flow when funding is needed but is not yet available. A bridge loan comes with relatively high interest rates and must be backed by some form of collateral

- PIK LoanPIK LoanA payment-in-kind or PIK loan is a loan where the borrower is allowed to make interest payments in forms other than cash.

- BankruptcyBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts

- Free Corporate Finance Course

-

Loan Administrator: Understanding Their Role and Responsibilities

What Is a Loan Administrator? When you take out any type of loan, such as a mortgage or car loan, you will have to work with a loan administrator during the life of the loan. Become a savvy l

-

Understanding Liens: A Comprehensive Guide to Property Rights

If you’ve taken out a loan to buy a car or house, there’s been a lien on it. So, what’s a lien and why should you care? A lien is a legal claim that allows a person or entity (a

finance

- Loan Capitalization Explained: Understanding Accrued Interest

- Understanding Good Loan Interest Rates: What to Expect

- Understanding Add-On Interest: How It Works & Loan Payments

- Collateral Explained: What It Is & How It Works

- Deferred Interest Explained: How it Works & Benefits

- Understanding Interest: Costs & Rewards of Borrowing and Lending

- Gift Loans: Understanding Tax Implications and Legal Considerations

- Bullet Loans: Risks, Benefits & How They Work

- Understanding Precomputed Loans: What You Need to Know

-

Understanding Vested Interest: Definition & Implications

Understanding Vested Interest: Definition & ImplicationsVested interest refers to an entity’s personal involvement in a business project, an investment, or the outcome of a given situation. Usually, they are situations that include the possibility of...

-

Starter Loans: Build Credit with Low or No Credit History

Starter Loans: Build Credit with Low or No Credit HistoryIf you’re new to borrowing money or have low credit scores, you may consider taking out what’s sometimes called a starter loan or credit-starter loan. Starter loans are personal lo...