Understanding Interest: Costs & Rewards of Borrowing and Lending

Interest refers to the cost of borrowing money or the reward for lending money. Typically, banks charge interest on money borrowed on top of the expected repayment of the principal. At the same time, banks also pay interest on depositors’ funds in savings and investment accounts. They do so to entice more deposits, which they use for on-lending to customers, charging a higher interest rate than they pay depositors.

Hence, interest is essentially additional money paid on top of the principal amount borrowed on a loan or received on top of deposits in a savings or investment account. Interest results from the opportunity costOpportunity CostOpportunity cost is one of the key concepts in the study of economics and is prevalent throughout various decision-making processes. The incurred due to the inability of the lender to utilize the money being lent out.

Interest is usually calculated as a percentage of a loan or deposit. Interest payments are made periodically, i.e., monthly, semi-annually, annually, or any other period as defined in a loan or savings/investment contract.

Interest is generally quoted as an annual rate but can be calculated for periods shorter or longer than a year. The percentage rate of interest charged is referred to as the interest rate. Examples of interest-bearing financial instruments include loans, mortgages, credit card debt, bonds, commercial paper, fixed deposits, bankers’ acceptancesBanker’s AcceptanceA banker’s acceptance refers to a financial instrument that represents a promised future payment from a bank. It states the name of the entity, among others.

History of Interest

The practice of charging interest on loans became widely accepted during the Renaissance era when mobility, trade, and commerce started to flourish. Conditions were ripe for starting new businesses, encouraging entrepreneurs to establish new business ventures. Loans were now needed for productive purposes (rather than consumptive reasons), which justified the charging of interest.

In medieval times, the charging of interest was considered morally reproachable and dubious as loans were largely purely consumptive, hence no tangible reason to reward lenders. Middle Eastern civilizations considered compound interestCompound InterestCompound interest refers to interest payments that are made on the sum of the original principal and the previously paid interest. An easier way to think of compound interest is that is it "interest on interest," where the amount of the interest payment is based on changes in each period, rather than being fixed at the original principal amount. as necessary to the development of industry, agriculture, and urbanization.

However, Islamic law forbids the charging of interest. It led to the development of interest-free Islamic banking and finance in the latter part of the 20th century. Countries such as Iran, Pakistan, Sudan, Saudi Arabia, Malaysia, UAE, and Kuwait practice Islamic banking to various degrees.

Prolific economists developed theories of interest rates concerning the economy, including Adam Smith, Irving Fisher, John Maynard KeynesJohn Maynard KeynesJohn Maynard Keynes (1883-1946) was an English economist who founded Keynesian economics, which discussed recessions and what governments should do, Carl Menger, Frédéric Bastiat, among others. Interest is an essential element in the functioning of global financial markets in the 21st century.

Interest Determinants

The amount of interest that is charged by a lender varies due to several factors, such as:

- Loan amount

- Loan type

- Tenure of the loan

- Expected inflation

- Liquidity of the loan

- Borrower credit history and credit score

- Government action of interest rate policy

- Risk of default

Interest Calculations

There are two major types of interest calculations: simple interest and compound interest.

Simple Interest

Simple interest is calculated using a rate of interest expressed in percentage terms, charged against the principal debt or outstanding amount at defined periods. Therefore, it is particularly easy to calculate simple interest at regular intervals. The borrower has more certainty on the required amount of future loan repayments or investment returns. Simple interest generally means the absence of compounding.

The simple interest formula is:

Simple Interest = P * r * t

Where:

- P = Principal value

- r = Annual interest rate

- t = Time (in years)

A loan of $20,000 with a simple interest of 5% per annum will incur an annual interest of $1,000.

Compound Interest

Compound interest is calculated by adding interest earned on prior periods of a loan or deposit to the principal amount. Therefore, successive interest payments are calculated on prior interest earned plus principal, which results in higher interest payments at every payment interval of the asset.

Compound interest is essentially interest on interest. It yields higher interest than simple interest, which encourages savings and investment but is costly for the borrower. Therefore, compound interest is influenced by the rate of compounding interest and the frequency in which the interest is compounded, i.e., either daily, monthly, quarterly, semi-annually, annually, or any other defined rate of recurrence.

Monthly compounding means that interest accruing during the month is compounded at the end of each month and added to the loan balance each month before calculating next month’s interest. Interest can also be compounded continuously, where it is measured using the exponential function e, which arises whenever a quantity (interest) grows or decays at a rate proportional to its current value. Compound interest is more commonly used on credit and deposit instruments.

The formula for compound interest is below:

Where:

- P = Principal value

- r = Annual interest rate

- n = Number of times interest is compounded each year

- t = Number of time periods of the loan/investment (e.g., number of years)

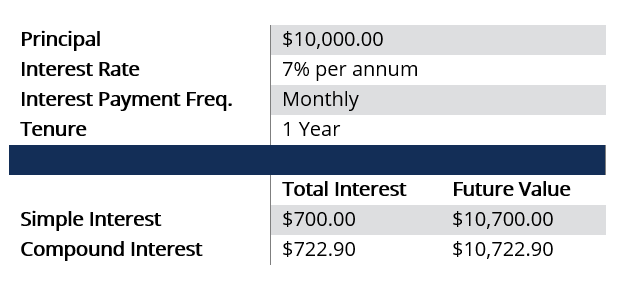

Example: Simple Interest vs. Compound Interest

Compound interest can be obtained using the formula as:

Compound Interest = $10,000 [(1 + 0.07/12)12×1 – 1] = $722.90

The example above demonstrates the power of compound interest. A fixed deposit of $10,000.00 for one year can grow to $10,722.90 on maturity using compound interest compared to $10,700.00 using simple interest. If it is a 2-year instrument, the amount of compound interest earned will increase from $722.90 in year 1 to $775.16 in year 2.

The example may suggest that the difference is small considering the amount of $10,000, but many banks today compound interest daily; hence, a large deposit can lead to a significant difference between the two interest calculations.

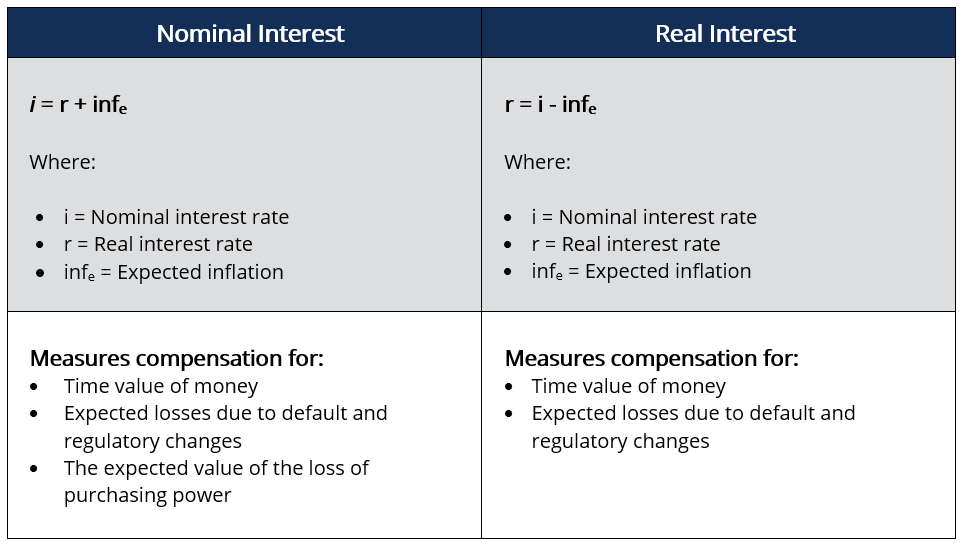

Nominal Interest vs. Real Interest

The fundamental difference between nominal interest and real interest is inflationInflationInflation is an economic concept that refers to increases in the price level of goods over a set period of time. The rise in the price level signifies that the currency in a given economy loses purchasing power (i.e., less can be bought with the same amount of money).. Nominal interest refers to interest paid (or earned) on a loan, i.e., the contractual rate agreed on granting the loan. Alternatively, the nominal interest rate is the sum of the real interest rate and expected inflation. The real interest is the nominal interest adjusted for inflation.

Real interest represents the effective interest rate paid (or earned). It is calculated as the difference between the nominal interest rate and the inflation rate. The Fischer effect is a concept that says an increase in expected inflation leads to an increase in nominal interest rate but leaves the expected real interest rate unchanged.

If a bank wants to earn interest of 9% and expects the inflation to be 3%, it must charge a nominal interest rate of 12% to account for inflation. If a bank charges a nominal rate of 9%, it will effectively earn a real rate of 6% (9% less 3%), which is sub-economic and less than the 9% they wanted.

Real interest rates can be negative when the inflation rate is higher than the nominal interest rate. However, nominal interest rates cannot be negative as it would not make sense for banks to pay a borrower to use its money. Nominal rates come with a floor of 0%.

Types of Interest

1. Fixed Interest

Fixed interest is calculated by using a fixed rate of interest on a loan. The rate is usually agreed upon at the time of granting a loan between the lender and the borrower by way of a loan contract. A fixed amount of interest is charged each interval period of interest payment by multiplying the principal loan amount or loan balance and the fixed interest rate.

The fixed interest rate is not affected by changes in market interest rates. A borrower charged a fixed interest rate of 8% per annum for a $50,000 loan over five years will pay an annual interest of $4,000 for the five-year period. Fixed interest is easier to calculate and predict.

2. Floating/Variable Interest

Floating interest is where the rate used to calculate interest payments fluctuates over time. The floating rate is usually linked to the prime rate, which banks use to lend to customers with good credit. It fluctuates depending on the central bank policy decisions.

Borrowers can benefit or incur losses if the prime rate decreases or increases, respectively. Banks normally quote the floating rate as the prime rate plus a margin that depends on the borrower’s credit rating.

3. The Prime Rate and Federal Funds Rate

The prime rate is the interest rate banks charge their most creditworthy customers. It is usually lower than the interest rate charged to most customers. In the U.S., it is the rate linked to the Federal Funds RateFederal Funds RateIn the United States, the federal funds rate is the interest rate that depository institutions (such as banks and credit unions) charge other depository institutions., i.e., the interest rate where banks lend and borrow money from each other.

4. Discount Interest

The discount interest rate is the rate used by banks to borrow funds from the central bank (in the U.S., Federal Reserve). The rate is not accessible to the public but is only used by institutional banks and the central bank.

The discount interest rate involves large sums of financial securities traded for short-term periods, i.e., overnight or a single day. It is used by banks to cover daily funding shortages, correct liquidity gaps, and prevent a bank from failing.

5. Annual Percentage Rate (APR)

Annual percentage rate (APR) is interest expressed as an annual rate rather than a periodic rate. Total interest is expressed annually on the total cost of the loan, including other costs. APR is generally used by credit card companies to set interest rates when consumers carry forward the balance on their credit card without repaying it fully.

APR is calculated as the prime rate plus a margin derived from the consumer’s credit rating. A credit card with a 30% percent APR equates to a daily percentage rate (DPR) of 0.082%. The DPR is multiplied by the daily card balance and multiplied by the number of days in the billing cycle.

More Resources

CFI offers the Certified Banking & Credit Analyst (CBCA)®Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money.

- Commercial PaperCommercial PaperA commercial paper refers to a short-term, unsecured debt obligation issued by financial institutions and large corporations in place of costlier methods of funding.

- Default RiskDefault RiskDefault risk, also called default probability, is the probability that a borrower fails to make full and timely payments of principal and interest,

- Prime RatePrime RateThe term “prime rate” (also known as the prime lending rate or prime interest rate) refers to the interest rate that large commercial banks charge on loans and products held by their customers with the highest credit rating.

-

Loan Administrator: Understanding Their Role and Responsibilities

What Is a Loan Administrator? When you take out any type of loan, such as a mortgage or car loan, you will have to work with a loan administrator during the life of the loan. Become a savvy l

-

Understanding Liens: A Comprehensive Guide to Property Rights

If you’ve taken out a loan to buy a car or house, there’s been a lien on it. So, what’s a lien and why should you care? A lien is a legal claim that allows a person or entity (a

finance

- Loan Capitalization Explained: Understanding Accrued Interest

- Understanding Good Loan Interest Rates: What to Expect

- Understanding Add-On Interest: How It Works & Loan Payments

- Bullet Loan Explained: Structure, Risks & Benefits

- Collateral Explained: What It Is & How It Works

- Deferred Interest Explained: How it Works & Benefits

- Gift Loans: Understanding Tax Implications and Legal Considerations

- Bullet Loans: Risks, Benefits & How They Work

- Understanding Precomputed Loans: What You Need to Know

-

Understanding Vested Interest: Definition & Implications

Understanding Vested Interest: Definition & ImplicationsVested interest refers to an entity’s personal involvement in a business project, an investment, or the outcome of a given situation. Usually, they are situations that include the possibility of...

-

Starter Loans: Build Credit with Low or No Credit History

Starter Loans: Build Credit with Low or No Credit HistoryIf you’re new to borrowing money or have low credit scores, you may consider taking out what’s sometimes called a starter loan or credit-starter loan. Starter loans are personal lo...