Understanding Cost Structure: Fixed vs. Variable Costs

Cost structure refers to the various types of expenses a business incurs and is typically composed of fixed and variable costsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according. Fixed costs are costs that remain unchanged regardless of the amount of output a company produces, while variable costs change with production volume.

Operating a business must incur some kind of costs, whether it is a retail business or service provider. Cost structures differ between retailers and service providers, thus the expense accounts appearing on a financial statementThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are depend on the cost objects, such as a product, service, project, customer, or business activity. Even within a company, cost structure may vary between product lines, divisions, or business units, due to the distinct types of activities they perform.

Fixed Costs

Fixed costs are incurred regularly and are unlikely to fluctuate over time. Examples of fixed costs are overhead costs such as rent, interest expenses, property taxes, and depreciationDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in. of fixed assets. One special example of a fixed cost is direct labor cost. While direct labor cost tends to vary according to the number of hours an employee works, it still tends to be relatively stable and, thus, may be counted as a fixed cost, although it is more commonly classified as a variable cost where hourly workers are concerned.

Variable Costs

Variable costs are expenses that vary with production output. Examples of variable costs include direct labor costs, direct material costCost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total, utilities, bonuses and commissions, and marketing expenses. Variable costs tend to be more diverse than fixed costs. For businesses selling products, variable costs might include direct materials, commissions, and piece-rate wages. For service providers, variable expenses are composed of wages, bonuses, and travel costs. For project-based businesses, costs such as wages and other project expenses are dependent on the number of hours invested in each of the projects.

Cost Allocation

Cost allocation is the process of identifying costs incurred, and then accumulating and assigning them to the right cost objects (e.g., product lines, service lines, projects, departments, business units, customers) on some measurable basis. Cost allocation is used to distribute costs among different cost objects in order to calculate the profitability of, for example, different product lines.

Cost Pool

A cost pool is a grouping of individual costs, from which cost allocations are made later. Overhead cost, maintenance cost, and other fixed costs are typical examples of cost pools. A company usually uses a single cost allocation basis, such as labor hours or machine hours, to allocate costs from cost pools to designated cost objects.

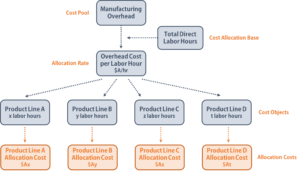

Example of Cost Allocation

A company with a cost pool of manufacturing overhead uses direct labor hours as its cost allocation basis. The company first accumulates its overhead expenses over a period of time, say for a year, and then divides the total overhead cost by the total number of labor hours to find out the overhead cost “per labor hour” (the allocation rate). Finally, the company multiplies the hourly cost by the number of labor hours spent to manufacture a product to determine the overhead cost for that specific product line.

The Importance of Cost Structures and Cost Allocation

To maximize profitsNet Profit MarginNet Profit Margin (also known as "Profit Margin" or "Net Profit Margin Ratio") is a financial ratio used to calculate the percentage of profit a company produces from its total revenue. It measures the amount of net profit a company obtains per dollar of revenue gained., businesses must find every possible way to minimize costs. While some fixed costs are vital to keeping the business running, a financial analystGuide to Becoming a Financial AnalystHow to become a financial analyst. Follow CFI's guide on networking, resume, interviews, financial modeling skills and more. We've helped thousands of people become financial analysts over the years and know precisely what it takes. should always review the financial statements to identify possibly excessive expenses that do not provide any additional value to core business activities.

When an analyst understands the overall cost structure of a company, he/she can identify feasible cost reduction methods without affecting the quality of products sold or service provided to customers. The financial analyst should also keep a close eye on the cost trend to ensure stable cash flows and no sudden cost spikes occurring.

Cost allocation is an important process for a business because if costs are misallocated, then the business might make wrong decisions, such as overpricing/underpricing a product, or invest unnecessary resources in non-profitable products. The role of a financial analyst is to make sure costs are correctly attributed to the designated cost objects and that appropriate cost allocation bases are chosen.

Cost allocation allows an analyst to calculate the per-unit costs for different product lines, business units, or departments, and, thus, to find out the per-unit profits. With this information, a financial analyst can provide insights on improving the profitability of certain products, replacing the least profitable products, or implementing various strategies to reduce costs.

Other Resources

CFI is a global provider of financial modeling courses and financial analyst certificationBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!. To continue developing your career as a financial professional, check out the following additional CFI resources:

- Cost Behavior AnalysisCost Behavior AnalysisCost behavior analysis refers to management’s attempt to understand how operating costs change in relation to a change in an organization’s

- Marginal Cost FormulaMarginal Cost FormulaThe marginal cost formula represents the incremental costs incurred when producing additional units of a good or service. The marginal cost

- Sunk CostSunk CostA sunk cost is a cost that has already occurred and cannot be recovered by any means. Sunk costs are independent of any event and should not

- Cost MethodCost MethodThe cost method of accounting is used for recording certain investments in a company's financial statements. The investment is recorded at historical cost

-

Understanding Labor Costs: Direct & Indirect Expenses

What Is the Cost of Labor? The cost of labor is the sum of all wages paid to employees, as well as the cost of employee benefits and payroll taxes paid by an employer. The cost of labor is bro

-

Understanding and Managing Inventory Costs: A Comprehensive Guide

Inventory procurement, storage and management is associated with huge costs associated with each these functions.Inventory costs are basically categorized into three headings:Ordering CostCarrying Cos

finance

- Understanding Cost of Production: A Comprehensive Guide

- Understanding Flotation Costs: A Comprehensive Guide

- Understanding Incremental Cost: A Definition & Key Considerations

- Capitalized Costs Explained: Definition & Examples

- Cost Allocation: Definition, Methods & Importance

- Cost Behavior Analysis: Understanding Cost Relationships & Management

- Cost Drivers: Understanding What Impacts Your Business Expenses

- Direct Costs Explained: Definition, Examples & vs. Indirect Costs

- Understanding Implicit Costs: A Comprehensive Guide

-

Understanding Implicit Costs: Opportunity Cost in Business

What Is an Implicit Cost? An implicit cost is any cost that has already occurred but not necessarily shown or reported as a separate expense. It represents an opportunity cost that arises when...

-

Cost Allocation: Definition, Types, and Examples for Businesses

Cost Allocation: Definition, Types, and Examples for BusinessesEven small businesses can benefit from properly a...