Understanding Flotation Costs: A Comprehensive Guide

Flotation costs are the costs that are incurred by a company when issuing new securities. The costs can be various expenses including, but not limited to, underwriting, legal, registration, and audit fees. Flotation expenses are expressed as a percentage of the issue price.

After the flotation costs are determined by a company, the expenses are incorporated into the final price of the issued securitiesMarketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion.. Essentially, the incorporation of the costs reduces the final price of the issued securities and subsequently lowers the amount of capital that a company can raise.

The size of flotation expenses depends on many factors, such as the type of issued securities, their size, and risks associated with the transaction. Note that the costs for issuing debt securities or preferred sharesPreferred SharesPreferred shares (preferred stock, preference shares) are the class of stock ownership in a corporation that has a priority claim on the company’s assets over common stock shares. The shares are more senior than common stock but are more junior relative to debt, such as bonds. are generally lower than those for issuing common shares. The flotation costs for the issuance of common shares typically ranges from 2% to 8%.

Flotation Costs and Cost of Capital

The concept of flotation costs is strongly related to the concept of cost of capitalCost of CapitalCost of capital is the minimum rate of return that a business must earn before generating value. Before a business can turn a profit, it must at least generate sufficient income to cover the cost of funding its operation.. Since flotation expenses affect the amount of capital that can be raised by issuing new securities, the costs must somehow impact a company’s cost of capital. There are two main views regarding the matter:

Approach 1: Incorporate flotation costs into the cost of capital

The first approach states that the flotation expenses must be incorporated into the calculation of a company’s cost of capital. Essentially, it states that flotation costs increase a company’s cost of capital. Recall that the cost of capital of a company consists of the cost of debt and cost of equityCost of EquityCost of Equity is the rate of return a shareholder requires for investing in a business. The rate of return required is based on the level of risk associated with the investment. Thus, expenses affect the cost of capital by changing either cost of debt or cost of equity, depending on a type of securities issued (e.g., issuance of common stock affects the cost of equity).

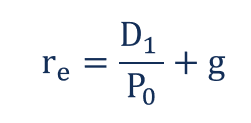

For example, let’s assume that a company issues new common shares. Before the transaction, a company’s cost of equity can be calculated using the following formula:

Where:

- re – Cost of equity

- D1 – Dividends per share one year after

- P0 – Current share price

- g – Growth rate of dividends

However, the issuance of new shares causes a company to incur flotation expenses. Thus, the current share price (denoted as ) must be adjusted for the effect of such costs.

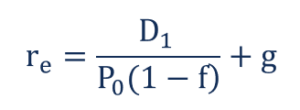

As a result, the cost of equity formula adjusted for the flotation costs will look:

Where:

- re – Cost of equity

- D1 – Dividends per share one year after

- P0 – Current share price

- g – Growth rate of dividends

- f – Flotation cost (in percentage)

Nevertheless, the abovementioned approach is not accurate because the incorporation of flotation expenses does not depict the actual picture. In such a scenario, the cost of capital is overstated by the percentage of flotation expenses incurred. The costs of flotation are non-recurring expenses that are incurred by a company only once when new securities are issued.

Approach 2: Adjust the company’s cash flows

Alternatively, the second approach is to adjust the company’s cash flows for the flotation expenses. Unlike the first method, the adjustment approach does not modify the actual cost of capital. Instead, a company deducts the costs from the cash flows that are used in the calculation of net present value (NPV)Net Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present..

The cash flow adjustment method was initially suggested by John R. Ezzell and R. Burr Porter in the article “Flotation Costs and Weighted Average Cost of Capital.” The main idea behind the method is that the costs are only one-time expenses paid to third parties.

The approach of deducting the flotation expenses from the company’s cash flows is more appropriate than the direct incorporation of the costs into a cost of capital because it considers the one-time nature of the expenses. Simultaneously, a company’s cost of capital remains unaffected by the flotation expenses, and it is not overstated.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Capital Raising ProcessCapital Raising ProcessThis article is intended to provide readers with a deeper understanding of how the capital raising process works and happens in the industry today. For more information on capital raising and different types of commitments made by the underwriter, please see our underwriting overview.

- Initial Public Offering (IPO)Initial Public Offering (IPO)An Initial Public Offering (IPO) is the first sale of stocks issued by a company to the public. Prior to an IPO, a company is considered a private company, usually with a small number of investors (founders, friends, family, and business investors such as venture capitalists or angel investors). Learn what an IPO is

- Offering MemorandumOffering MemorandumAn Offering Memorandum is also known as a private placement memorandum. It is used as a tool to attract external investors.

- Retainer FeeRetainer FeeA retainer fee is an upfront cost paid by an individual for the services of an advisor, consultant, lawyer, freelancer, or other professional.

-

Cost Behavior Analysis: Understanding Cost Relationships & Management

Cost behavior analysis refers to management’s attempt to understand how operating costs change in relation to a change in an organization’s level of activity. These costs may include direc

-

Understanding Direct Cost of Sales (COGS): Definition & Components

Direct cost of sales, more commonly known as cost of goods sold (COGS), is the amount of cash that a company invests in the production of a good or service it sells. Direct cost of sales do

finance

- Understanding Agency Costs: Protecting Shareholder Interests

- Understanding Cost of Production: A Comprehensive Guide

- Understanding Cost Structure: Fixed vs. Variable Costs

- Understanding Fixed Costs: Definition, Examples & Importance

- Understanding Incremental Cost: A Definition & Key Considerations

- Understanding Proceeds: Definition, Types & Calculation

- Capitalized Costs Explained: Definition & Examples

- Cost Allocation: Definition, Methods & Importance

- Cost Drivers: Understanding What Impacts Your Business Expenses

-

Life Cycle Cost Analysis (LCCA): A Comprehensive Guide

Life Cycle Cost Analysis (LCCA): A Comprehensive GuideLife cycle cost analysis (LCCA) is an approach used to assess the total cost of owning a facility or running a project. LCCA considers all the costs associated with obtaining, owning, and disposing of...

-

Product vs. Period Costs: Understanding the Key Differences

Product vs. Period Costs: Understanding the Key DifferencesManufacturing companies need to track both produc...