Understanding Credit Scores: What They Are & Why They Matter

A credit score is a number representative of an individual’s financial and credit standing and ability to obtain financial assistance from lenders. LendersFinancial IntermediaryA financial intermediary refers to an institution that acts as a middleman between two parties in order to facilitate a financial transaction. The institutions that are commonly referred to as financial intermediaries include commercial banks, investment banks, mutual funds, and pension funds. use the credit score to assess a prospective borrower’s qualification for a loan and the specific terms of the loan. Essentially, it is used to determine the borrower’s ability to pay back the borrowed amount in due time. The credit score assessment is provided by a consumer credit reporting agency such as Equifax or TransUnion.

Who Uses Credit Scores?

Any organization that lends money as a source of business uses credit scores to assess the eligibility of a borrower. Such organizations specifically include banksTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks in the USA as of February 2014. , credit card companies, fintech-based lenders, insurance companies, landlords, government agencies, and mortgage companies.

It can be any individual or organization that seeks to lend someone money or enter into a contract that will require another party to pay them back in a predetermined time.

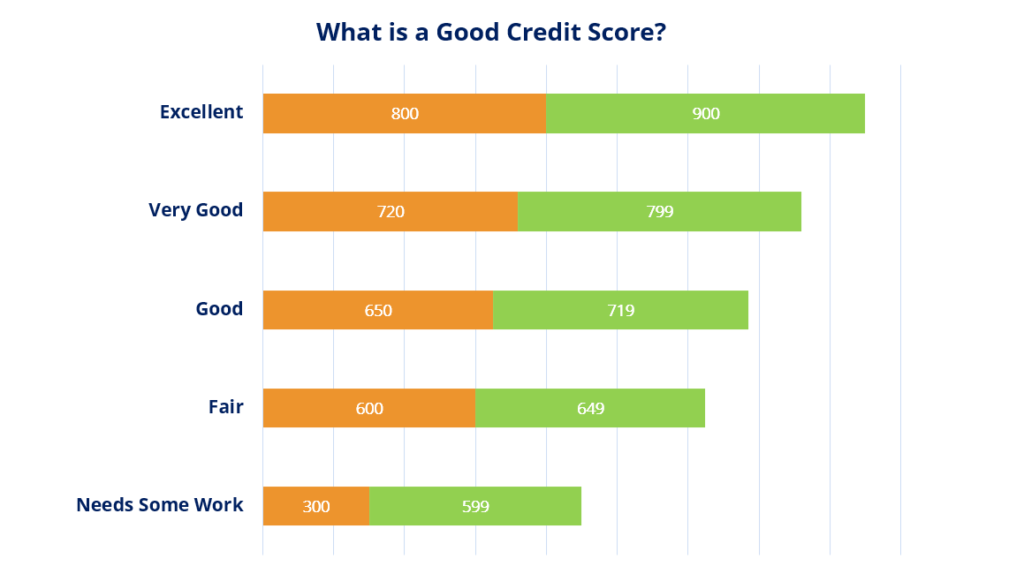

What is a Good Credit Score?

A credit score ranges from 300 to 850. The higher your credit score, the better your standing as a borrower is. A respectable credit score is above 670.

How to Improve your Credit Score

1. Pay your bills on time

Paying off what is due on time consistently will establish your credibility as a borrower. Building your credit history takes time and steadily paying off what you owe in a timely manner is considered one of the biggest indicators of your creditworthiness.

For lenders, past behavioral patterns are considered key indicators of the future. Therefore, proving to lenders that you are capable of paying back on time helps improve your credit score.

2. Reduce your overall loan amounts

Proactively paying off more than what is due will ultimately help you showcase yourself as a credible borrower, who not only pays back, but who does so ahead of the due date. Doing that can also decrease any interest paymentsInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also on borrowed funds.

For example, if you have the means to prepay your mortgageMortgageA mortgage is a loan – provided by a mortgage lender or a bank – that enables an individual to purchase a home. While it’s possible to take out loans to cover the entire cost of a home, it’s more common to secure a loan for about 80% of the home’s value., then by doing so, you are coming across as a credible borrower and your credit score will improve.

3. Manage credit cards effectively:

Credit cardsCredit CardA credit card is a simple yet no-ordinary card that allows the owner to make purchases without bringing out any amount of cash. Instead, by using a credit, if used diligently, are an excellent way to improve your credit score. Ideally, you should not spend more than 35% of your credit limit. Following this practice will help keep your total debt amount in check and also help ensure that you are able to easily pay back financing extended to you. Lenders specifically look at how much of your available credit you have actually borrowed. Again, to rate higher with lenders, it’s a good idea to access no more than 35% of your available credit at any given time. So, for example, if you have a credit card with a $5,000 line of credit, you shouldn’t allow your outstanding balance for that card to get above $1,700-$1,800.

4. Do not buy what you can’t afford

As a golden rule, do not purchase things that you can’t immediately pay off. While buying things on credit is convenient, if there is something you cannot afford immediately with the funds available to you, it is generally better to look in the other direction.

Maintaining financial health is all about making the correct decisions for yourself in the broad scheme of things and not indulging in impulse purchases that you may regret later.

Related Readings

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money.

- ArrearsArrearsArrears refers to payments that are overdue and that are supposed to be made at the end of a given period after missing out on the required payments.

- Fair Credit Billing Act (FCBA)Fair Credit Billing Act (FCBA)The Fair Credit Billing Act (FCBA) is a US federal law that mandates the protection of consumers from exploitation by creditors through billing errors. Enac

- Loan CovenantLoan CovenantA loan covenant is an agreement stipulating the terms and conditions of loan policies between a borrower and a lender. The agreement gives lenders leeway in providing loan repayments while still protecting their lending position. Similarly, due to the transparency of the regulations, borrowers get clear expectations of

-

Understanding B Credit Ratings: What They Mean for Businesses

Corporations and other businesses must demonstrate their creditworthiness to potential lenders – and that's where credit rating agencies come in. Standard & Poor's (S&P), Moody's a

-

Understanding the R9 Credit Score Code: What It Means & Implications

A notation of "R9" next to an account on a credit report is not actually a credit score but rather a code that indicates the payment status of that account. Payment status affects your credi

finance

- Understanding FICO Scores: Your Key to Creditworthiness

- Understanding Bad Credit Scores: What You Need to Know

- Understanding Fair Credit Scores: Ranges & What They Mean

- Understanding Credit Scores: What's Average & How to Improve

- Understanding Bad Credit Scores: Causes & How to Improve

- Understanding Credit Scores: What's a Good Score & How to Achieve It

- Understanding FICO Scores: Your Comprehensive Guide

- Understanding Fair Credit Scores: What They Mean & How to Improve

- Understanding Credit Scores: What They Are & Why They Matter

-

Intraday Credit: Understanding Short-Term Account Overdrafts

Intraday Credit: Understanding Short-Term Account OverdraftsIntraday credits refer to short periods during which an account may be overdrawn. An intraday credit, also called a daylight credit, is a credit lasting less than one day given to a person or...

-

Credit Amnesty: Understanding the Truth & Avoiding Scams

Credit Amnesty: Understanding the Truth & Avoiding ScamsCredit amnesty may not be as enticing as it sounds. This ruse is as old as the hills. While you'll see credit amnesty offers in television and radio advertising, you're most likely to...