Understanding Earned Premium: A Guide for Life & Health Insurance

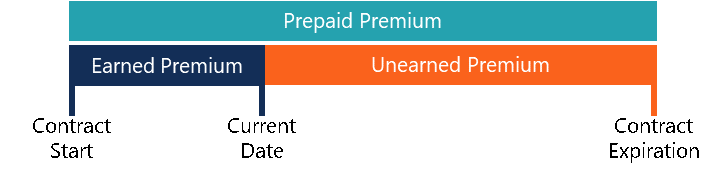

An earned premium represents premiums earned on the portion of an insurance contract that has expired. The premiums associated with the active portion of an insurance contract are considered unearned, as the insurance companyLife and Health InsurersLife and health (L&H) insurers are companies that provide coverage on the risk of loss of life and medical expenses incurred from illness or injuries. The customer - the purchaser of the insurance policy - pays an insurance premium for the coverage. is still taking on a risk in order to generate the premiums.

Summary

- An earned premium represents premiums earned on the portion of an expired insurance contract.

- There are two methods that insurance companies use to report their earned premiums: the accounting method and the exposure method.

- Actual methods for recording the premiums can be much more complex.

Understanding Earned Premium

When an insurance company writes an insurance contract, they assume financial riskFinancial Risk ModelingFinancial risk modeling is the process of determining how much risk is present in a particular business, investment, or series of cash flows. Learn risk analysis during the time of that contract. For example, if you buy insurance on your car and your car is hit and damaged, the insurer would need to pay a certain amount of money towards paying for that damage.

For this reason, insurance companies consider premiums on an insurance contract unearned until the contract has expired. Once the contract has expired, the insurance company is no longer assuming any financial risk, and the premium is considered earned.

The diagram above can help to understand how earned premiums work. While the insurer might have collected a prepaid premium on the contract start date, the earned premium is only the pro-rated amount of that premium until the current date.

Unearned Premiums

Unearned premiums are premiums that have been collected by the insurance company, where the underlying portion of the insurance contract has not expired. In the case that the contract is ended prematurely, the premiums would be returned to the policyholder.

For example, assume that a customer bought a one-year auto insurance policy and prepaid for six months of premiums at $100 per month. However, after one month, the car figures in an accident, requiring the insurer to reimburse the policyholder. The insurer makes $100 as earned premiums and returns $500 to the insured party as unearned premiums.

Methods for Calculating Earned Premium

There are two main methods for calculating the earned premium:

1. Accounting method

The accounting method takes the number of days since the beginning of an insurance contract and multiplies the figure by the premium earned each day. It is the most common method for calculating earned premium and accurately reflects the amounts insurance companies made on specific contracts.

2. Exposure method

The exposure method is much more complex and data-driven than the accounting method. It uses historical data to estimate the value of insurance contracts. It looks at the risk of payout and the estimated collection of premiums.

Example Using Accounting Method

Assume an insurer writes a one-year auto insurance contract with a premium of $100 per month. The policyholder prepays for six months worth of premiums. After three months, what would the earned premium be under the accounting method and the exposure method?

Using the accounting method, you would simply multiply the monthly premium by the number of months expired. Therefore, the earned premium would be $300 (3 months x $100/month). The remainder amount of prepaid premiums would be returned to the policyholder and would be considered unearned premiums ($300).

Example Using Exposure Method

Using the exposure method, the customer would need to look at historical risk levels. If the company decided that the chance of payout of the given contract is 5% with a payout of $1,000, the level of risk would need to be factored into the earned premium calculation by looking at the unearned portion.

$1,000 x 5% = $50 and $100 x 95% = $95; $45 (the difference between the expected value of premium earned and the expected value of payouts) would be the insurer’s monthly expected value of profit from the insurance policy.

Other Considerations

While the above examples of calculating earned premiums can help consumers to understand them, they are simplifications of models that are used by insurers. Insurance companies continue to become more accurate and data-driven in the way they structure policies.

Additionally, insurance contracts contain stipulations that can void them and affect earned premiums. For example, if a customer took out a life insurance policy and didn’t specify a serious medical condition, the contract would be void. Therefore, the insurer would keep the unearned premiums as earned premiums.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Commercial Insurance BrokerCommercial Insurance BrokerA commercial insurance broker is an individual tasked with acting as an intermediary between insurance providers and customers.

- HMO vs PPOHMO vs PPO: Which is Better?Getting the best healthcare often requires choosing between an HMO vs PPO. You need to be able to make an informed decision on which plan will work best.

- Property and Casualty InsurersProperty and Casualty InsurersProperty and casualty (P&C) insurers are companies that provide coverage on assets (e.g., house, car, etc.) and also liability insurance for accidents, injuries, and damage to other people or their belongings.

- Variable Life InsuranceVariable Life InsuranceVariable life insurance is a form of life insurance that combines the characteristics of life insurance and investment. Characteristics: policy loans

-

Liquidity Premium: Definition, Calculation & Investment Implications

A liquidity premium compensates investors for investing in securities with low liquidity. Liquidity refers to how easily an investment can be sold for cash. T-billsTreasury Bills (T-Bills)Treasury Bil

-

Call Premium Explained: Understanding Issuer Redemptions & Option Pricing

A call premium refers to the amount above par value an investor receives when the debt issuer redeems the security earlier than its maturity date. If a security is redeemed before it reaches maturity,

finance

- Dwelling Insurance: Understanding Coverage & Benefits

- Understanding Net vs. Gross Premium: What's the Difference?

- Understanding Annual Insurance Premiums: A Comprehensive Guide

- Understanding Pro-Rata vs. Short-Rate Insurance Premiums: Get a Refund

- Understanding Health Insurance Premiums: A Comprehensive Guide

- Bancassurance Explained: How Banks and Insurance Partner

- Understanding Unearned Premiums in Insurance: A Comprehensive Guide

- Understanding Car Insurance Premiums: Factors & Costs

- Comprehensive Car Insurance: What It Covers & Why You Need It

-

Understanding Insurance Premiums: Types & Factors

Understanding Insurance Premiums: Types & FactorsInsurance premiums are the monies paid by individuals to insurance companies in exchange for financial security in the event of damage or a loss. Often, these premiums are dependent upon a variety of ...

-

Default Risk Premium: Understanding & Calculation

Default Risk Premium: Understanding & CalculationA default risk premium is effectively the difference between a debt instrument’s interest rate and the risk-free rateRisk-Free RateThe risk-free rate of return is the interest rate an investor c...