Know Your Client (KYC): Definition, Importance & Compliance

The Know Your Client (KYC) or Know Your Customer (KYC) is a process to verify the identity and other credentials of a financial services user. KYC is a regulatory process of ascertaining the identity and other information of a financial services user.

The Know Your Client (KYC) process helps against money launderingMoney LaunderingMoney laundering is a process that criminals use in an attempt to hide the illegal source of their income. By passing money through complex transfers and and prevents the financing of terrorist activities. It is a mandatory process required by many countries to ensure that the customers are actually who they are claiming to be.

Importance and Benefits of KYC

To be mandated by the law, the Know Your Client (KYC) process also helps the financial institutions in several ways:

- Helps lenders perform risk assessment by identifying the previous financial history and assets owned

- Limits fraud that result mainly due to hiding of identity

- Prevents money laundering and other anti-social activities

- Brings stability and investment to the country, as it makes the financial framework more trustworthy and less risky

- Decreased uncertainty allows institutions to lend more to customers and increase their profits

A number of countries and economic regions oversee financial anti-money laundering agencies or regulators that overview financial transactions to prevent tax evasion, terrorism financing, and other anti-social activities. All the agencies are a part of the Global Financial Action Task Force (FATF), which overviews financial transactions globally.

KYC Documents Required

The KYC process is carried out for both individuals and organizations. KYC authentication is based on verification of identity and place of residence. The documents required for the KYC process for individuals include the usual documents that individuals generally use, such as:

- Driver’s license

- Social security card/number

- Passport

- Documents issued by the state or the federal government.

For proof of residence, the following documents can be furnished:

- Utility bills, such as telephone, electricity, gas, etc.

- Bank statementsBank StatementA bank statement is a financial document that provides a summary of the account holder’s activity, generally prepared at the end of each month.

- Employment documents

- Housing contracts and rent agreements

KYC Process

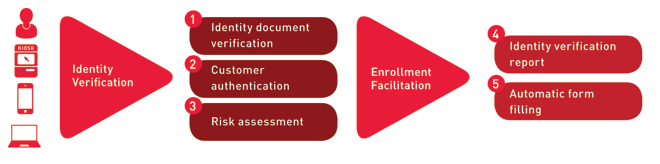

The KYC process is simple and differs only slightly from country to country. A simple KYC process flow is depicted below:

The KYC process can follow the following steps, although not always in the same order:

Step 1: Submission of documents

An applicant or potential user of financial services is required to submit documents for the verification of their identity and residence status. The submission can be either in electronic form or physical form.

Step 2: Identity verification

The identity verification is carried out from the authorized agency/organization based on the document submitted. For example, if the applicant submits a driver’s license, the verification will be done from the Department of Motor Vehicles (DMV).

Step 3: Residency verification

The residency verification requires ascertaining the resident status (domestic or foreign), current residential address, alternative residential address, citizenship status, etc.

Step 4: Verification of financial condition

The assets and liabilities claimed are verified using documents, contacting the issuer, and physical checks. This reduces the risk of misrepresentation.

Step 5: Transactions monitoring

The financial institution checks the transactions conducted by the customer/client, and any transaction that is different/high-valued, frequent, etc., is flagged automatically and then undergoes stringent manual checks.

After completion of all the above steps, the individual/body is deemed KYC verified. It may also include a verification certificate, but that is generally not the case. The process may be simple for the user, but the financial institution’s verification process needs dedication and diligence. The KYC process is an integral part of various due diligenceDue DiligenceDue diligence is a process of verification, investigation, or audit of a potential deal or investment opportunity to confirm all relevant facts and financial information, and to verify anything else that was brought up during an M&A deal or investment process. Due diligence is completed before a deal closes. checks made by companies, investors, banks, etc.

KYC Verification Agencies

As discussed earlier, the KYC process consumes a significant amount of time and effort. Hiring staff and performing physical verification is a cumbersome and costly affair. The cost becomes higher for smaller financial institutions. As a result, the KYC process is usually contracted out to agencies that specialize in them. The two major reasons for doing so are:

- Agencies offer reduced costs for the same due to economies of scaleEconomies of ScaleEconomies of scale refer to the cost advantage experienced by a firm when it increases its level of output.The advantage arises due to the.

- They also come with a better experience, as they’ve undertaken the process for all types of institutions and clients.

Choosing an agency to perform KYC depends on the type of verification needed. Some processes, such as a bank account opening, may not involve checks on assets and liabilities. Therefore, some important facts to consider include:

- Is the agency offering all the services required? Some agencies may only provide identity and address verification.

- Document verification coverage can differ, as some agencies may not offer international coverage or coverage in documents using different languages.

- The most important factor is if the agency is verified/licensed by the relevant regulatory body in a given jurisdiction.

- Tools and technology are used for data handling and whether it is safe enough to prevent document loss and loss of client confidentiality.

- The price offered should be significantly lower than what it would cost to carry out the process by other means.

More Resources

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)®Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Anti-Money LaunderingAnti-Money LaunderingAnti-Money laundering (AML) is a set of policies, procedures, and technologies that prevents money laundering and monitor potential fraudulent activity.

- Customer BondingCustomer BondingCustomer bonding is the process through which a company or organization makes connections with its customers. The goal of customer bonding is to develop a

- Fraud TriangleFraud TriangleThe fraud triangle is a framework commonly used in auditing to explain the reason behind an individual’s decision to commit fraud. The fraud

- Types of Due DiligenceTypes of Due DiligenceOne of the most important and lengthy processes in an M&A deal is Due Diligence. The process of due diligence is something which the buyer conducts to confirm the accuracy of the seller's claims. A potential M&A deal involves several types of due diligence.

-

Understanding IRA Withdrawal Rules: Early Access to Retirement Funds

This article was fact-checked by our editors and CPA Janet Murphy, senior product specialist with Credit Karma Tax®. If you’re struggling financially and have some money set aside

-

Coronavirus Tax Relief: What You Need to Know - Credit Karma Tax

This article was fact-checked by our editors and Christina Taylor, MBA, senior manager of tax operations for Credit Karma Tax®. The financial impact of the COVID-19 pandemic has sp

finance

- Understanding Face Masks: Guidance & Safety Information

- 401(k) Mistakes: Avoid Costly Errors & Maximize Retirement Savings

- Child Life Insurance: Is It Right for Your Family?

- Understanding the IPO Process: A Comprehensive Guide

- Debit Cards for Kids: A Parent's Guide to Financial Literacy

- Rent Your Car: A Comprehensive Guide to Car Sharing & Side Hustle Income

- First-Time Home Buyer's Guide: Essential Things to Consider

- Understanding Investment Fees: A Comprehensive Guide

- Massachusetts Unemployment Benefits: COVID-19 Relief & Eligibility

-

![Louisiana Mortgage Rates: Trends & Options - [Year]](https://www.etffin.com/article/uploadfiles/202110/2021101111045324_S.jpg) Louisiana Mortgage Rates: Trends & Options - [Year]

Louisiana Mortgage Rates: Trends & Options - [Year]Louisiana hosts more than 400 festivals and events each year, making it an exciting place to live and work. The state also offers a low cost of living and small-business culture. I...

-

Joint Checking Accounts: A Comprehensive Guide for Shared Finances

Joint Checking Accounts: A Comprehensive Guide for Shared FinancesCo-managing your money with another person could be necessary for multiple reasons, from merging your finances as a married couple to caring for an elderly parent. Opening a joint ...