Free Non-Directional Trading Strategies Template | Corporate Finance Institute

Published June 25, 2019

Read Time 2 minutes

Over 2.8 million + professionals use CFI to learn accounting, financial analysis, modeling and more. Unlock the essentials of corporate finance with our free resources and get an exclusive sneak peek at the first module of each course. Start Free

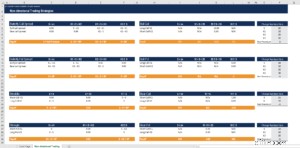

What is the Non-Directional Trading Strategies Template?

The non-directional trading strategies template allows users to determine the profit when buying options. This template focuses on non-directional strategies that bet on the volatility of the market to create profit. These strategies usually include a combination of call and put options. The profit of the strategies depends on the spot price and the cost of the option premiums. Numbers of strike prices, net premiums, and spot prices can all be altered.

Here is a quick preview of CFI’s non-directional trading strategies template.

Download the Free Template

Overview of Non-directional Trading Strategies

Non-directional trading strategies are bets on the volatility of the underlying asset. A straddle or strangle strategy is used by investors if they believe there will be high volatility in the asset prices. However, if they believe there will be low volatility, then they will create a butterfly spread. All strategies are created by using either call or put options.

Butterfly spread using calls

Investors use a butterfly spread when they think there will be little volatility in the price. Butterfly spread using calls are made by combining a bull call spread and a bear call spread. The bull call has strike prices of K1 and K2, and the bear call has strike prices of K2 and K3. This is also the same as buying a call with K1, a call with K3 and selling two calls with a strike price of K2.

Butterfly spread using puts

Butterfly spread using puts is also a bet on low volatility of the price. This trading strategy is made with a bull put spread and bear put spread. The bull put spread has strike prices of K1 and K2, and the bear put spread has strike prices of K2 and K3. This is also the same as buying a put with K1, a put with K2, and selling two puts with a strike price of K2.

Straddle

Investors use the straddle strategy when they believe the price of the underlying asset will be volatile. This is made with a call and put option with the same strike price. If premiums are not considered, then investors will receive a profit if the spot price is either bigger or smaller than the strike price.

Strangle

A strangle strategy is similar to a straddle as both rely on the volatility of the market. It is also made with the purchase of a call and put option. However, a strangle costs less than a straddle. This is because the put option has a lower strike price, and the call option has a higher strike price.

Why Does It Matter?

Non-directional trading strategies template help investors limit their risk, decrease costs, and predict the cash flow with greater accuracy. These strategies also allow investors to make investment decisions based on their market predictions.

Additional Resources

For more resources, check out CFI’s Business Templates Library to download numerous free Excel modeling, PowerPoint presentations, and Word document templates. See also our financial modeling resources and Excel resources.

-

![Medicaid Application: Eligibility & How to Apply - [State Name]](https://www.etffin.com/article/uploadfiles/202109/2021092610242280_S.jpg)

Medicaid Application: Eligibility & How to Apply - [State Name]

Low-income individuals and families may qualify for Medicaid benefits that cover such things as medical assistance, doctor's visits, prescription drugs, testing, physical therapy, hospital stays a

-

Ethereum (ETH) Price Surge: Is Now the Right Time to Buy?

Many or all of the products here are from our partners that pay us a commission. It’s how we make money. But our editorial integrity ensures our experts’ opi

finance

- Break the Cycle: How to Stop Impulse Clothing Purchases

- Veteran Car Loans: Affordable Auto Financing Options for Military Members

- Voting Trust Certificate: Definition & Corporate Control

- Visa vs. Mastercard: Which Card is Right for You?

- Coverdell ESA: Your Guide to College Savings & Tax Benefits

- How Social Media Distractions Impact Your Finances - A Comprehensive Guide

- Understanding Cash Advances: How They Work & When to Use Them

- Achieve Your Financial Goals: 6 Common Mistakes to Avoid

- Navigating Finances After Marriage: A Practical Guide

-

Smart Home Buying: Expert Tips for a Successful Purchase

Smart Home Buying: Expert Tips for a Successful Purchasediv.cust...

-

Top Microtask Sites: Earn Money Online with Quick Tasks

Top Microtask Sites: Earn Money Online with Quick TasksEven if you have a busy schedule, there are countless easy ways to earn extra money on the side. The best micro task sites let you make money online by completing a variety of activities in 20 minute...