Avoid the $326,000 Investing Mistake: Don't Panic Sell!

Disclosure: This post may receive compensation from partners listed through affiliate partnerships, at no cost to you. This doesn’t influence our ratings, and the opinions are our own. Learn more here.

What does a $326,000 investing mistake look like?

Panic selling during a market crash to “feel safe.”

I watched it happen in 2008…

Two investors. Same portfolios. Opposite decisions.

One sold everything. One stayed invested.

The difference 11 years later? $326,000.

Here’s exactly how it happened (and how you can avoid making the same mistake):

Investor A: The Market Timer

March 2008:

- Portfolio value: $250,000

- Watching the news every night

- Anxiety building as markets decline

October 2008:

- Market down 35% from peak

- Portfolio now worth $162,500

- Can’t take it anymore – sells everything to “stop the bleeding”

- Plans to “get back in when things stabilize”

March 2009:

- Market starts recovering

- Waits for “confirmation it’s safe”

- Misses the initial 20% rebound

June 2009:

- Finally reinvests at higher prices

- Has $162,500 to invest (the cash from selling)

December 2019 (11 years later):

- Final portfolio value: $486,000

- Return: ~10% annualized from reinvestment point

The cost of panic selling and market timing: Over $300,000

Investor B: The Long-Term Investor

March 2008:

- Portfolio value: $250,000

- Also watching the news, also anxious

October 2008:

- Portfolio down to $162,500

- Painful to watch, but does nothing

- Actually continues monthly $500 contributions

March 2009:

- Still fully invested

- Buying shares at historically low prices with monthly contributions

December 2019 (11 years later):

- Final portfolio value: $812,000

- Return: ~10.5% annualized on original investment, plus new contributions compounded

The reward for staying invested: $326,000 more than Investor A

Same starting point.

Same market conditions.

Completely different outcomes.

The only difference? Investor B stayed invested through the volatility.

The Data Backs This Up

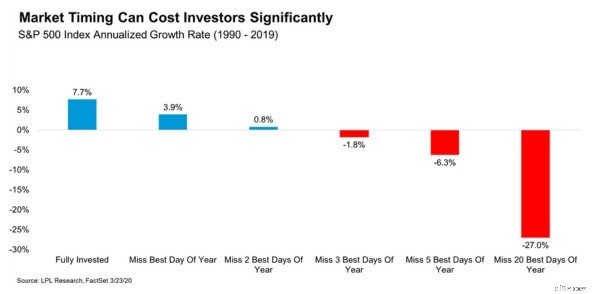

Take a look at this chart showing S&P 500 returns from 1990-2019:

Here’s what it shows:

- Fully Invested: 7.7% annual return

- Miss the BEST 1 day: 3.9% annual return

- Miss the BEST 5 days: -1.8% annual return

- Miss the BEST 20 days: -27.0% annual return

Missing just the 5 best trading days over 30 years means the difference between growing your wealth and losing money.

Here’s the problem: Those best days are impossible to predict.

In fact, many of the market’s best days happen during the most volatile periods – right when investors are most tempted to sell.

During the 2008-2009 crisis:

- 6 of the 10 best single-day gains happened within 2 weeks of the 10 worst days

- If you sold to “avoid the bad days,” you almost certainly missed the best days too

You can’t have one without risking the other.

What Investor B Did Differently (And What You Can Do)

Investor B didn’t have superhuman discipline.

She had a system that removed emotion from the equation.

Here’s her exact strategy:

1. Automated Everything

- Set up automatic monthly contributions ($500) to her investment account

- Enabled automatic dividend reinvestment (DRIP)

- Never had to “decide” to invest – it just happened

Why this works: You can’t panic sell or time the market if your investing is on autopilot.

2. Stopped Checking Daily

- Deleted investing apps from her phone

- Checked portfolio quarterly instead of daily

- Focused on account statements showing contributions, not daily fluctuations

Why this works: Daily volatility triggers emotional reactions. Quarterly reviews show the long-term trend.

3. Had a Written Investment Plan

Before the crisis, she wrote down:

- “I’m investing for retirement in 25+ years”

- “Short-term volatility is expected and normal”

- “I will not sell unless my financial goals fundamentally change”

During the crisis, she reread this document weekly.

Why this works: Your future self makes better decisions than your panicked present self.

4. Used the “STOP” Technique

Whenever she felt the urge to sell, she asked herself one question:

“Has my financial situation fundamentally changed, or is this just market noise?”

99% of the time, the answer was noise.

Why this works: Verbalizing your thoughts interrupts the emotional response and engages rational thinking.

5. Asked Three Key Questions

Before any buy or sell decision, she asked herself:

- Do I believe in the long-term potential of these investments? (Yes – diversified index funds in profitable companies)

- Am I investing for a long-term goal? (Yes – retirement in 25+ years)

- Has my financial situation fundamentally changed? (No – still employed, emergency fund intact)

If all three answers supported staying invested, she did nothing.

Why this works: Creates a logical framework that overrides fear-based decisions.

The Bottom Line

Investor A tried to outsmart the market.

Investor B trusted time in the market.

The result?

Investor B ended with $326,000 more.

Here’s what I learned from advising hundreds of investors:

The ones who built the most wealth weren’t the smartest.

They weren’t the ones with the best market predictions.

They were the ones who:

- Invested consistently, regardless of market conditions

- Stayed invested through volatility

- Automated their investing to remove emotion

- Focused on decades, not days

The hardest part of successful investing isn’t finding the right stocks.

It’s doing nothing when everyone else is panicking.

Investor B’s $326,000 advantage came from having a system that helped her do exactly that.

Build your system today.

Your bank account will thank you later,

Fiona

The Millennial Money Woman

-

529 College Savings Plans: A Comprehensive Guide for Parents

My wife and I began thinking about college expenses when we were expecting our first child. With college tuition rising faster than inflation, we know that saving for college is important! My wife an

-

Achieve Financial Independence: Calculate & Track Your Net Worth

MM Note: This post was written by Todd Kunsman, a 29-year-old who started his FIRE journey 3 years ago. His previous guest posts include 8 Steps To Financial Freedom and 5 Steps To Start Sav

Personal finance

- Financial Compatibility: 3 Essential Money Questions to Ask Before Marriage

- Common Money Mistakes: Fix Your Finances Today

- Meratas CEO Darius Goldman Discusses Income Share Agreements on This Week in Startups

- Canceling Holiday Travel Due to COVID-19: What Are Your Options?

- Pandemic's First College: Higher Education & Alternative Financing Updates

- Higher Ed & Alternative Finance News: Weekly Roundup - Meratas Memo

- Fourth Stimulus Check: Fact vs. Fiction - What You Need to Know

- Child Tax Credit Impact: Study Highlights Benefits for Minority Households

- Freelancer Rate Increase: When & How to Ask for a Raise

-

Budget-Friendly Halloween Costumes: Creative & Affordable Ideas

Budget-Friendly Halloween Costumes: Creative & Affordable IdeasDressing up for Halloween is one of the best parts of the holiday, especially if you’re a creative person. But buying a Halloween costume can get expensive, with many costing more than $5...

-

Average Family Income in the US: A Comprehensive Overview

Average Family Income in the US: A Comprehensive OverviewYou hear a lot of talk about the "Average American Family." How many members does it have, where do they live, what do they eat? All of these are popular topics. But the primary figure bandi...