Roth IRA: Your Path to Tax-Free Wealth & Financial Freedom

-

by

Fiona Smith

by

Fiona Smith

- Updated April 2, 2025

Disclosure: This post may receive compensation from partners listed through affiliate partnerships, at no cost to you. This doesn’t influence our ratings, and the opinions are our own. Learn more here.

You don’t have to be a pro-investor to open a Roth IRA.

In fact, Roth IRAs are one of the simplest and most powerful tools for building wealth.

And in this guide, I’ll show you how a Roth IRA can make you a tax-free millionaire (even if you’re just starting out).

Let’s dive in.

In this guide

What is a Roth IRA and How Does it Work?

A Roth IRA is a tax-advantaged retirement account that anyone can open. You pay taxes on any contributions you make and in exchange, you won’t have to pay taxes on withdrawals, including investment profits.

If you’re just starting out in your career and if you believe taxes will be higher in the future, a Roth IRA could be one of the best types of investment vehicles for you.

Below is a quick overview of the key features:

Investment Growth / Profit

Tax-free

Contribution Limits [2024]

$7,000 – under 50

$8,000 – 50 and older

Contribution Phase-Out Begins at this Annual Earned Income Level

Single filers: $146,000–$161,000

Married Filing Jointly: $230,000–$240,000

Eligibility to Contribute

Must have earned income

Earned income must fall within or under the phase-out limits

Minimum Age to Open a Roth

None (as long as you have earned income)

A parent must sign-up with you if you are under 18

Age you can Withdraw all Assets Without Penalty

59.5

What you can Withdraw Without Penalty at Any Time

Initial Contributions

Penalty if you Withdraw Assets Before 59.5

10% penalty on the investment profits

Must pay ordinary income taxes on investment profits

IRA stands for: Individual retirement account.

A Roth IRA is a type of individual retirement account.

So, just like:

- Regular investment account

- Checking accounts

- Savings accounts

- 401k accounts

…A Roth IRA is simply the name of an account that can hold your investments.

By investments, I mean that a Roth IRA could have some of the following:

- Cash

- ETFs

- Bonds

- Stocks

- Index Funds

- Mutual Funds

You get the point.

A Roth IRA also means your money is treated differently on a tax basis:

Contributions

Are Taxed

Investment Profit

Not Taxed

A Roth IRA means that the money you contribute is already taxed – and that you do not receive a tax deduction on your Roth IRA contributions (unlike with a Traditional IRA).

Let’s take your weekly paycheck for example:

Total Weekly Earnings

$2,000

Taxes

$500

Take-Home Paycheck

$1,500

Your take-home pay is $1,500.

And as you can see, you’ve already paid taxes.

When you decide to invest in a Roth IRA, you would take a portion of that leftover $1,500 (it’s already been taxed) and put that into your Roth IRA.

However, it’s a different story when it comes to the withdrawals of your Roth IRA (which I will discuss later).

Earned income would not include income from:

- Social security

- Deferred compensation

- S corporation distributions

As long as you have earned income – you can contribute to a Roth IRA, regardless of your age.

If you are younger than age 18, an adult can open a custodial Roth IRA account for you (the adult will control the account until you turn 18 or 21, depending on the state you live in).

Second, let’s review what income phaseout ranges for a Roth IRA mean:

For the 2024 year, your contributions will phase out if you make over $146,000 per year (for the individual tax filer) and if you make $230,000 per year (for the married tax filer).

How much can I Contribute to my Roth IRA?

There are maximum annual contribution limits but no minimum contribution limits.

You do not need $1,000 to start investing in a Roth IRA.

You can start with an investment as small as $10.

The only caveat here is that some Roth IRA providers (like Vanguard, Fidelity, Charles Schwab, etc.) may not allow you to start investing with $10 – you may need to boost your investment up to $100 or more.

Contribution Amount

Under 50

50 and Older

For 2024

$1 to $7,000

$1 to $8,000

If you’re just starting and cannot afford to invest $1,000’s in your Roth IRA, I’d suggest to consider opening a Roth IRA account with Acorns.

Acorns is the perfect investment app for the beginning investor. It takes all but 5 minutes to set-up and you have some pretty good quality investments.

Plus, you can invest as little as $5 with Acorns.

How to Open a Roth IRA

If you are ready to open a Roth IRA account, then it’s time to act.

Below are the 4 steps to open a Roth IRA account:

- Select your Roth IRA company

- Open your Roth IRA account

- Fund your Roth IRA account

- Select your investments

1. Select your Roth IRA Company

Before you even open your Roth IRA account, you have to select which company you want to hold your Roth IRA.

Below are my personal favorites:

- Best Micro-Investing Roth IRA platform: Acorns

- Best Automated & Hands-off Roth IRA platform: M1 Finance

There are many other great companies out there as well such as Vanguard (another personal favorite).

Acorns and M1 Finance in my opinion offer great services for low prices.

2. Open your Roth IRA Account

The next step is to actually open your Roth IRA account.

Here’s how long it should take you to open your Roth IRA account:

Acorns

9 Minutes

M1 Finance

10 Minutes

It takes less than 5 minutes to open your Roth IRA account… so you really can’t use the excuse “I don’t have time.”

3. Fund your Roth IRA Account

Next, you have to fund your Roth IRA account.

How to fund your Roth IRA account:

- In your newly opened Roth IRA account, find the page (or link) to connect your bank account

- Update your bank routing number and account number

- Select how much (if any) you want to transfer from your bank to your Roth IRA

- Fund your Roth IRA with cash from your checking account

I would also call the Customer Service team to help you confirm this funding process and help you answer any questions you may have.

Remember that every Roth IRA platform is different, so I would always recommend for you to do your own research.

4. Select your Investments

Lastly, you need to consider which investments you will buy in your Roth IRA.

A Roth IRA offers many different investment options, including:

- ETFs

- Stocks

- Bonds

- Index Funds

- Mutual Funds

- Real Estate Investment Trusts (REITs)

Investing in a Roth IRA is very similar to investing in any other, regular investment account.

You can:

- Invest automatically

- Buy and sell investments

- Monitor your investments

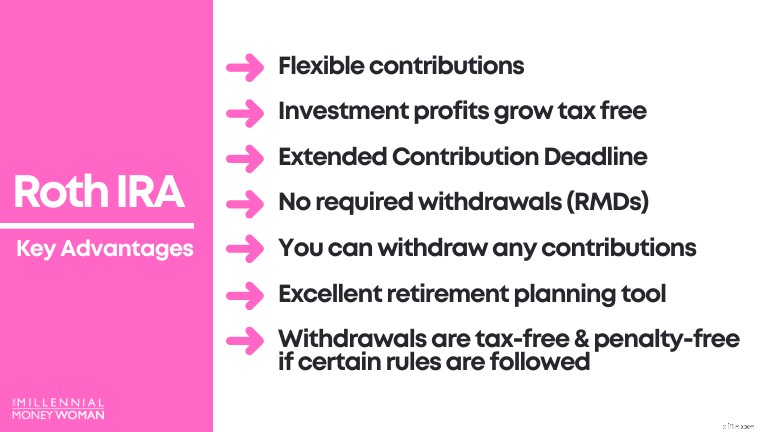

Roth IRA Advantages

The next step is understanding the key advantages of a Roth IRA.

These include the following:

- Flexible contributions

- Investment profits grow tax-free

- Extended Contribution Deadline

- No required withdrawals (RMDs)

- You can withdraw any contributions

- Good retirement planning tool for young folks

- Withdrawals are tax-free & penalty free if certain rules are followed

Roth IRA Advantage #1: Earnings and Investment Profits Grow Tax-Free

The number 1 reason why Roth IRAs are a preferred investment instrument is because the investment profits are not taxed.

1 Time Roth IRA Contribution

$1,000

Timeframe Invested

45 years

Investment Return

7%

Final Portfolio Value

$21,002

Now let’s analyze the tax consequences, assuming you’re over 59.5 and had your Roth IRA open for 5 or more years:

Original Contribution

$1,000

Investment Profits

$20,002

Using these guidelines, you’ll see the massive tax advantage with Roth IRAs, when it’s time to withdraw your money:

Original Contribution ($1,000)

Tax-Free

Investment Profits ($20,002)

Tax-Free

In Roth IRAs, your investment profits are completely tax-free after age 59.5 and if you keep your account open for 5+ years.

You are not obligated to pay Uncle Sam a dime of taxes with a Roth IRA, assuming you follow the specified guidelines.

Roth IRA Advantage #2: Withdrawals are Tax-Free and Penalty-Free

This advantage is very similar to the one I just described above:

- Your investment growth is tax-free

- Anything you withdraw from your Roth IRA is tax and penalty-free*

*To be very clear – you do have to follow certain rules to make sure that everything really is tax and penalty-free.

The 2 general guidelines to avoid taxes and a 10% penalty on the investment profits are below:

- If you are 59.5 or older

- And opened your account 5+ years ago

Roth IRA Advantage #3: Can Withdraw Contributions Penalty and Tax-Free

There is a difference between the term investment gains and the term investment contribution.

Let’s take this sample scenario:

Original Contribution

$1,000

Investment Profits

$20,002

Total Portfolio Value

$21,002

Even if you’re 22 years old and only had your Roth IRA for 2 years, you can still withdraw up to $1,000 without any penalties or taxes.

Why?

Because you’ve already been taxed on that $1,000 contribution.

In other words, Uncle Sam doesn’t care what you do with your original contribution – you can keep it in your Roth IRA or you can withdraw the money.

Roth IRA Advantage #4: No Required Withdrawals (RMDs)

Traditional IRAs and 401k’s force you to take out a portion of your money at age 72.

For a Traditional IRA and 401k this means:

- You’ll have to pay income taxes on whatever you withdraw

Roth IRAs do not have this rule – they do not have RMDs (required minimum distributions).

Why do Roth IRAs not have RMDs?

That’s because you already paid taxes on your original contributions (remember the after-tax money/paycheck example).

Roth IRA Advantage #5: Roth IRAs are Typically a Good Retirement Planning Tool for Younger Folks

Roth IRAs typically are a great retirement planning tool for young folks.

That’s because if you’re young, you are typically at the beginning of your working career, earning the lowest wages in your life:

- You’re in one of the lowest tax brackets

If you’re in a low tax bracket, that means it probably doesn’t hurt you too much if you’re taxed on Roth IRA contributions today (instead of having those contributions being deducted from your income taxes, as with Traditional IRAs).

Down the road, let’s say when you are 40 or 60 years old, you are typically toward your peak earning years:

- You’re in a higher tax bracket

If you’re in a higher tax bracket, you’ll likely want to consider other options like a Traditional IRA, since contributions will be deducted immediately from your income tax returns, which means you’ll have a lower tax bill in the current year.

Roth IRA Advantage #6: Extended Contribution Deadline

I had this experience the first year I opened my Roth IRA: It was the middle of December and I only had made $500 of Roth IRA contributions.

All of a sudden, I found myself scrambling to hit the December 31st contribution deadline… until I realized that the Roth IRA contribution deadline is extended (phew!).

This means that:

Latest Roth IRA contribution deadline

Contribute on the tax day filing deadline (typically April 15th of every year) to make a contribution for the previous year

In plain English:

- Date: February 2, 2025

- You’re looking to make a $7,000 Roth IRA contribution for 2024

- Roth IRA contribution deadline for 2024: April 15, 2025

Thank goodness for flexible deadlines!

Roth IRA Advantage #7: Flexible Contributions

Just as with flexible contribution deadlines, a Roth IRA also offers you flexibility in the type and amount of contributions you add to your Roth IRA.

You don’t have to make 1 lump-sum contribution of $7,000 each year.

Here’s what you can do:

- Invest when you want to invest

- Contribute when you have the money

- Automatically set up an investment strategy

- Dollar cost average every week (for example)

- Randomly pull money into your Roth IRA when you have money

Basically, you treat a Roth IRA just like any other investment account.

The tax treatment (after-tax) and contribution amount ($7,000 if you’re under 50) are the major differences.

Does a Roth IRA have an Early Withdrawal Penalty?

Yes, there is an early withdrawal penalty with a Roth IRA.

You may have to pay a 10% penalty in addition to paying income taxes if you withdraw any of the investment profits (not contributions) from your Roth IRA before age 59.5.

There are some ways to get around this early withdrawal penalty, which include:

59.5 years or older

Roth IRA is open for 5+ years

No

No

59.5 years or older

Roth IRA is open for less than 5 years

No

Yes

Younger than 59.5

Roth IRA is open for less than 5 years

Yes

Yes

Below are some additional scenarios that may help you understand what will happen with your Roth IRA withdrawal scenarios:

If you:

- Are younger than 59.5

- Had your Roth IRA for less than 5 years

You may be able to avoid:

- Penalties

- Not taxes

In [some of] the following situations:

- Pay for a disability or death

- Pay for qualified education expenses

- Pay for qualified birth or adoption expenses

- Pay for a first-time home (up to $10,000 in your life)

- Pay for unreimbursed medical expenses or health insurance if you’re unemployed

On the flip side, let’s check out what happens if you’ve had your Roth IRA for 5+ years.

If you:

- Are younger than 59.5

- Had your Roth IRA for 5+ years

You may be able to avoid:

- Penalties

- Taxes

In [some of] the following situations:

- Pay for a disability or death

- Pay for qualified education expenses

- Pay for qualified birth or adoption expenses

- Pay for a first-time home (up to $10,000 in your life)

- Pay for unreimbursed medical expenses or health insurance if you’re unemployed

When can you Withdraw from a Roth IRA?

To keep matters simple, 59.5 is the age at which you can withdraw from a Roth IRA without the 10% penalty and without income tax.

Note that you do need to have your Roth IRA open for 5 or more years to avoid both penalties and taxes.

What is the Difference Between a Roth IRA and a Traditional IRA?

I’ve been asked this question multiple times.

Ultimately, both the Roth IRA and the Traditional IRA are excellent investment accounts.

Below is a chart that details which account might be the best for you, given your situation:

Could be the Best option if…

You believe your income will be higher during retirement than your tax bracket today

You believe your income tax bracket will be lower during retirement than your tax bracket today

As you can see, choosing the optimal investment account really has to do with your income earning potential and how much you believe your earned income will be during retirement.

That’s why when you’re young (ie – you have a higher income earning potential, since you’re at the beginning of your career), it’s typically recommended that you choose the Roth IRA route.

Can you Lose Money in a Roth IRA?

Investing in a Roth IRA is like investing with any other account – so the potential to win or lose money is always a risk.

However, if you:

- Consistently invest

- Maintain a long term mindset

- Invest in low-cost index funds

- Never withdraw your investments

Then chances are, after 4 or 5 decades, you would have made some serious [tax-free] profits.

Let’s check it out in the sample scenario, below.

Your current age

20

Investment time frame

45 years [you’ll be 65 years old]

Estimated annual return

7%

Deposit frequency

Monthly

Deposit amount

$300

Total ending portfolio value

$1,061,298 [Tax-free!!]

Remember, over the past 50 years, the stock market returned an average of 7% (adjusted for inflation) which is why I used this 7% return number here.

Some years could be a higher return, others a lower return, but the average should be around 7%.

Roth IRA: The Bottom Line

A Roth IRA is a tax-advantaged retirement investment account.

- Investment gains and profits are tax-free

- Your contributions are after-tax (you don’t receive a deduction)

- Your withdrawals are tax-free (assuming you follow several Roth IRA rules)

Typically speaking, a Roth IRA is a retirement account that can help younger folks who expect to see an increase in their income during retirement.

When they start withdrawing money from their Roth IRA during retirement, they won’t have to pay taxes.

There are 2 requirements to contribute to a Roth IRA:

- You must have earned income

- Your annual income must fall within the phaseout ranges (explained above)

So when is a Roth IRA the best option for you?

- It all depends on how you envision your future income during retirement

- If you expect to be in a higher tax bracket in retirement then it would likely be better to invest in a Roth IRA today

Essentially, it’s sort of a gamble whether a Roth IRA is the best for you because it really comes down to your future.

However, I would argue that most of you know yourselves by now.

You know whether you want to:

- Grow your career

- Grow your income

- Earn a lot of money in your future years

- Marry (and have an additional income stream on tax returns)

If you said “yes” to any of the above options, then a Roth IRA may likely be the best option for you because chances are you’ll end up in a high tax bracket during retirement.

Here’s what I do:

I’ve been investing in a Roth IRA since I was 20 years old.

I firmly believe that a Roth IRA is the right choice for me, because I know that when I’m ready to retire at 65 or 70 (yes, I love to work), I better be in a higher tax bracket than I am today.

In the end, it’s a personal preference.

But, it’s a good idea to start thinking about your options today.

Your bank accounts will thank you later!

Join 30,000+ People That Get My Weekly Tips via Email

Every Saturday morning, you’ll get 1 actionable tip to help you save more money, increase your income, and multiply your wealth 👇

No spam. Just the highest quality tips on the web.

Join 30,000+ others and get access to exclusive tips, strategies, and resources that I don’t share anywhere else 👇

-

Top 10 Secured Credit Cards to Rebuild Your Credit

Secured credit cards can help re-establish credit. Americans who fall behind in their credit card payments and other bills may suffer a decline in their credit scores. Secured credit cards ma

-

Ripple (XRP) Jumps 20% Following Santander Payment App Integration

Ripple (XRP) prices today surged more than 20%, leading a global rally for cryptocurrencies. Financial institution Santander has tapped Ripples technology for its latest blockchain-based mobile paym

Personal finance

- Corporate Tax Rates by State: A Comprehensive Guide for Business Owners

- Job Hopping Pays Off: Americans Can Expect an Average 5.8% Salary Increase by Switching Jobs

- Budgeting 101: A Young Professional's Guide to Financial Freedom

- Inflation vs. Wages: Why U.S. Workers Experienced a Real Pay Cut in 2021

- Save Money on Pet Food: A Simple Change for 2022

- Inflation & Stimulus: What Americans Need to Know

- 8 Smart Financial Decisions for a Secure Future

- Roth IRA: A Comprehensive Guide to Tax-Free Retirement Savings

- Investing in Target (TGT): A Guide to Buying Stock

-

Bitcoin: The Double-Edged Sword of Decentralization - Risks & Rewards

Bitcoin: The Double-Edged Sword of Decentralization - Risks & RewardsBitcoin reached a huge new peak in value in June 2017, when one unit of the virtual currency was worth US$2,851 (£2,208), up from around US$600 just a year earl...

-

Reverse Stock Split Explained: What It Is & How It Works

Reverse Stock Split Explained: What It Is & How It WorksA reverse stock split, as opposed to a stock split, is a reduction in the number of a company’s outstanding shares in the market. It is typically based on a predetermined ratio. For example, a 2...