14 Proven Money Hacks to Boost Your Financial Future

Disclosure: This post may receive compensation from partners listed through affiliate partnerships, at no cost to you. This doesn’t influence our ratings, and the opinions are our own. Learn more here.

Today I’m going to show you 14 money hacks you should be using.

In fact, these money savings hacks will help you:

- Pay off debt

- Save more money

- Make more money

- Invest more money

Let’s dive right in.

In this article

The 14 Best Money Hacks

You and I both work very hard for our money.

It’s only natural that we want to find ways to keep and grow our wealth as much as possible.

However, it’s not always easy to know where (or how) to start.

And that’s why I created this list of the best money hacks so you can build generational wealth.

So if you’re ready, let’s kick things off with money hack #1.

1. Open an Investment Account

One of the savviest money hacks is opening an investment account ASAP.

Pros

– Helps you build long term wealth

– Uses compound interest to grow your investments

Cons

– Stock market volatility

– You won’t see immediate progress

Best Resource

M1 Finance

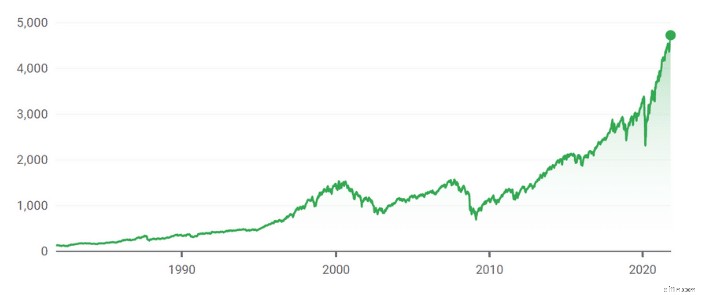

Did you know that more than 50% of US adults have money invested in the stock market?

The stock market is such a great place to grow your money and build long-term wealth.

Rarely will you get rich fast in the stock market.

If you don’t believe me, then believe the 6th richest man in this world – Warren Buffett.

Buffett is a very strong believer in the “Buy and Hold” investing strategy (aka buy a stock and hold it for the next 3 to 4 decades so it can appreciate in value).

In fact, Buffett’s favorite investment was the S&P 500 index fund (it’s my favorite investment as well!).

The picture above is the S&P 500’s performance today. The 2008 Great Recession looks like a tiny blip on this grandiose chart!

Focus on the long-term investment, and you’ll probably make a profit.

In fact, if you had invested $10,000 in the S&P 500 index back in 1980, that $10,000 would have been worth over $760,000 in 2018!

Long-term investing requires minimal effort as well.

With long-term investing, you simply choose an index fund or a stock that you want to invest in and then hold that stock or fund for the next couple of decades.

Now, you can start investing by opening an investment account with well-known (and free) platforms like M1 Finance 👇

M1 Finance is a free investment app where you can either build your own investment portfolio using the 6,000+ stocks and ETFs offered on M1 Finance or by selecting one of M1 Finance’s pre-selected portfolios (or “pies” as they are called).

There are 2 types of pies:

- Custom Pies – You can create your own investment strategy from 6,000+ ETFs and funds

- Expert Pies – You can select from 80+ pies created by M1 Finance’s expert team

The good news is you don’t have to be an experienced investor to start using M1.

However, you do need at least $100 to start investing with M1 Finance.

Whatever your choice, make sure to follow this money hack and start investing today.

Your bank accounts will thank me later.

2. Invest in Yourself

Out of all the money hacks listed in this article, I believe this is one that you should implement and practice regularly.

Pros

– Learn daily

– Improve your skills

– Add more value & get paid more

Cons

– Time-consuming

– Could cost some upfront money

Best Resource

Udemy

Investing in yourself is the ultimate life hack.

Investing in yourself is the best investment you can make.

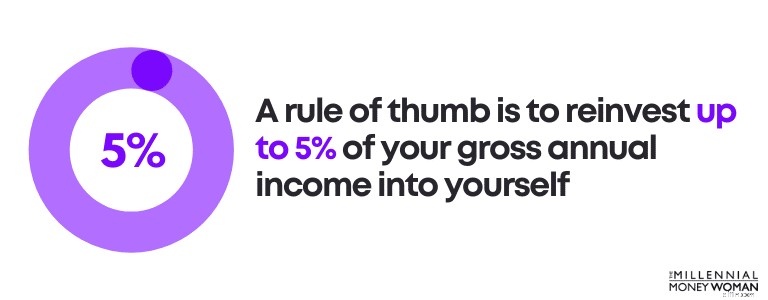

In fact, I try to reinvest about 3% to 5% of my gross annual income back into myself to grow my career and my knowledge.

You can never go wrong investing in yourself.

Below are several examples that I have used in the past to successfully reinvest in myself and in my future:

- Books

- Exercise

- Seminars

- Meditation

- Online classes

- Starting a business

- Attending networking events

I try to make it a goal to read a minimum of 1 book a month to expand my knowledge and learn from other, successful people.

Did you know that 85% of self-made millionaires read 2+ books per month?

Some of my favorite books include:

- The Behavior Gap by Carl Richards

- The Millionaire Mind, by Dr. Thomas J. Stanley

- The Monk who Sold his Ferrari by Robin Sharma

- The Subtle Art of Not Giving a F*ck by Mark Manson

There is so much knowledge packed into these books – be it about psychology, money, life, or just purpose.

I also love taking online classes as a form of investing in myself.

While I would love nothing more than going back to college and becoming an eternal student, learning subjects from astronomy to arithmetic, I don’t want to spend $100,000’s of dollars on a degree.

That’s where online class programs like Udemy have played a major role in my development 👇

Udemy is an online platform that offers the following:

- 65 languages

- 70,000 instructors

- 40 million students

One of my favorite courses that’s offered by Udemy that can come in handy – especially if you’re planning to start your own business – is called: An Entire MBA in 1 Course.

I also want to point out that investing in your knowledge is not the only way to invest in yourself.

You can also invest in your:

- Mental health

- Physical health

In fact, 76% of the wealthy exercise aerobically for at least 30 minutes daily.

Personally speaking, exercise:

- Decreases my stress

- Improves my fitness

- Helps me stay focused

- Increases my happiness

So overall, exercise is actually a pretty positive thing in my life, which is why I exercise for at least 30 minutes, 5 times a week.

Take this money hack to heart: Investing in yourself will likely yield the highest returns.

3. Monetize Your Social Media Account

A great money hack you can use to earn passive income is monetizing your social media account.

Pros

– You earn money by sharing affiliate products/services

Cons

– It takes time to build an audience

Best Resource

X Mastery

Believe it or not, you can make money from your social media account.

In fact, since I started my Twitter account just over a year ago, I’ve been able to make $1,000’s from my social media profile!

Before you even start thinking about money, you have to make sure you have some of the basic strategies in place.

These strategies include:

- Creating a brand

- Using high-quality images

- Taking the time to craft a great bio

- Including your website URL (if you have one)

As an example, here’s how my social media profile looks:

While I’m not saying that my social media profile is perfect, I am saying that my profile seems to work, since I gain between 200 to 300 followers a day.

However, monetizing your social media account isn’t just about the looks, the aesthetics, or the feel of your profile.

It also has to do with:

- Your niche

- Your content

- Your engagement

Before you monetize, you want to figure out the type of niche you plan on being in.

Niches on social media could include:

- Food

- Travel

- Fitness

- Finance

- Comedy

- Relationships

However, you can niche down even further, as I did. My niche is finance, but I’m specifically focused on finance for millennials.

Once you have your niche, it’s time to focus on your content.

In other words, you better make sure your content adds value for your audience before you start pushing products and services their way.

If you need help structuring your content, then check out this content creation guide, X Mastery.

Remember you cannot start pushing products/services without first adding value.

Building trust takes time, so don’t expect your audience to start buying from you, if you’re not adding value to their lives through excellent content.

After trust has been built, it’s time to consider which products or services you would like to affiliate market for.

When it works, affiliate marketing is like a well-greased money printing machine.

When it doesn’t, it is just a bunch of lost time and frustration on your end.

Learn the ropes of social media affiliate marketing by taking the X Mastery course, which can transform your money journey.

Related: How to Make Money on Twitter

4. Build a Solid Budget

If you want to save money fast, then one of the best money hacks is to build a solid budget.

Pros

– Save more money

– Cut out unnecessary costs

– Stay on track with your spending

Cons

– Time-consuming

– Might cause anxiety if you’ve never budgeted before

Best Resource

YNAB (aka You Need A Budget)

Creating a budget, in my opinion, is one of the ultimate money hacks that can change your financial future for the better.

Have you ever gone on a long road trip?

Chances are, if you want to arrive at your destination on time, you’ll probably need a GPS, physical map, iPhone navigation, etc.

Unless you have a photographic memory, you probably won’t make it to your destination on time (if at all) without a map.

Your budget is your financial map.

Here is why you need a budget ASAP:

- Budgets help you cut out unnecessary expenses

- Budgets help you change your spending behavior

- Budgets help you understand your spending patterns

- Budgets help you focus on your long term financial goals

I know that the “b” word probably isn’t a topic that you’re excited about.

In fact, I know a lot of people who tend to shy away from budgeting, because:

- They don’t know how to start

- They don’t completely understand what a budget is

- They’re scared to know how much they’re actually spending

And to be honest, I didn’t know how to start budgeting either, until I started brushing up on my personal finance skills.

Below are the budgeting rules of thumbthat helped me go from carrying $3,000 in credit card debt (back when I was a college student) to paying off all of my debt and saving more than 70% of my gross annual income.

Monthly Housing Debt

< 28% gross monthly income

Total Monthly Consumer Debt

< 20% net monthly income

Total Monthly Debt Payments

< 36% gross monthly income

Retirement & Savings

> 20% gross monthly income

When I mention the “retirement and savings” category, I mean a long-term savings and investing strategy.

As in, don’t plan to touch this money until you’re about to retire.

Think about it this way:

If you want to retire without financial worries, you’re probably going to have to do more than what the “average” rule of thumb suggests you do.

If you want to be above average, then you’ll have to do what the average person won’t.

And that’s where a budget will make a huge difference in your financial picture.

Are you ready to make a change in your life?

Start by creating your profile (it’s free) with YNAB (aka You Need A Budget).

YNAB, in my opinion, is the best budgeting app out there.

It’s 100% free to sign-up and you’ll get a free trial for 34 days (unless you’re a college student, in which case YNAB is completely free for 1 year).

Below are some YNAB pros and cons:

Strictly budgeting app

No reporting

Visual tracking of expenses

Not as intuitive

Customizable

No investing feature

Syncs with 12,000+ banks

Customer service isn’t available by phone

Here’s how much first-time YNABers claim they save with YNAB:

- First 2 months: $600 saved

- First year: $6,000 saved

So, if you want to start saving money, cutting out unnecessary expenses, and moving toward a better financial future, one of the ultimate money hacks is budgeting.

Recommended Reading: YNAB Review

5. Pay Off High-Interest Debt

One of the most critical money hacks is paying off high-interest debt – ASAP.

Pros

– Frees up cash flow

– Saves you money

Cons

– Could strain your cash flow as you pay off your high-interest debt

Best Resource

Tally

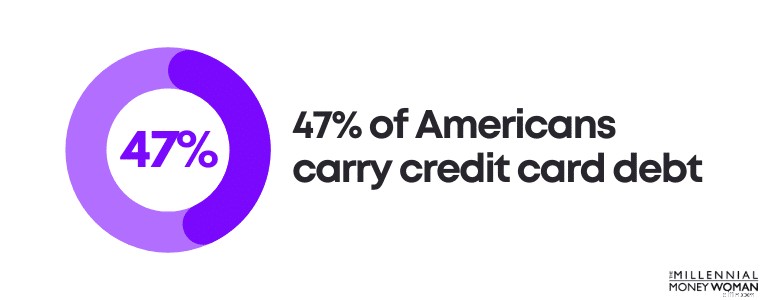

Did you know that 47% of Americans carry credit card debt?

Take a look at the liabilities (aka your debt) that you owe.

Some examples of debt include:

- Car loan

- Mortgage

- Credit cards

But, not all debt is equal.

In fact, some debt is even considered “smart debt.”

Debt with high-interest rates that is used to buy depreciating assets

Debt with low-interest rates that is used to buy appreciating assets

As an example, credit card debt would be considered bad debt while mortgage debt would be considered smart debt.

Not only do credit cards almost always buy depreciating assets (like technology gadgets, clothing, etc.), but credit cards also have very high-interest rates.

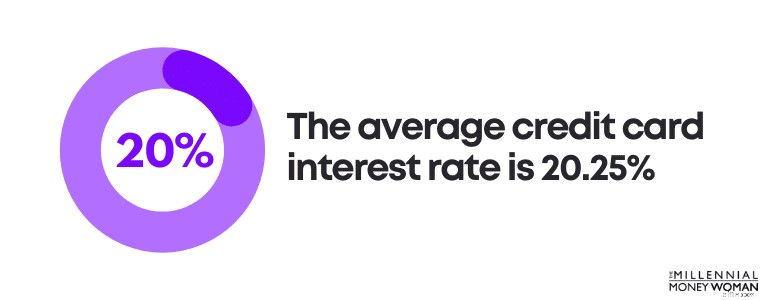

In fact, the average credit card interest rate is 20.25%.

Unfortunately, the average individual credit card debt has increased over the past several years, and it doesn’t appear like that trend will recede anytime soon.

Let’s do some math:

Let’s assume you carry the average credit card debt balance of $6,270 and you pay the average interest rate of 20.25%.

Here’s how much interest you would pay: $1,269.68.

In other words, you would be paying $1,269.68 on top of your original debt – which is $6,270.

That’s why I think it’s key to pay off high-interest debt first.

Below are some strategies you could consider implementing to get rid of credit card debt:

- Consider credit card debt consolidation

- Pay off more than the monthly minimum

- Consider a 0% interest teaser rate credit card balance transfer

- Consider paying off the debt with the highest interest rate first

Personally speaking, I prefer paying off the highest interest rate first (while continuing to make the monthly minimum payments on all the other debts).

Are you feeling overwhelmed with the number of debt payments you have to make?

In that case, you may want to consider debt consolidation.

So, instead of making 7 different payments to 7 different lending companies, you only have to make 1 payment to 1 new lending company.

As with all things, there are pros and cons.

Let’s take a look at the pros and cons of debt consolidation below:

Simplification

Upfront fees

Lower interest rates

Could increase interest rates

Structured repayment plan

Not good if you miss payments

Could reduce monthly payments

Temporary fix

Another benefit of debt consolidation is that assuming you make all payments on time and in full, you have the potential to increase your credit score.

If you’re considering debt consolidation, then I would suggest you check out Tally

Tally makes it simple to stay on top of your credit cards.

You scan your cards. If you qualify, tally gives you a line of credit at a low APR and manages all your payments.

No late fees. No gimmicks. Just a faster way to pay down your balances.

The most important thing that I can say is to figure out a game plan to get out of debt.

This is one of my favorite money hacks because it can help you find peace and move toward your other financial goals.

6. Build an Emergency Savings Fund

One of the easiest money hacks is to prepare for unexpected future expenses by building and maintaining an emergency savings fund.

Pros

– Helps you avoid taking on credit card debt

– Helps relieve you of any stress in the case of financial emergencies

Cons

– Low-interest rates

– Might take a while to fund your emergency account

Best Resource

CIT Bank

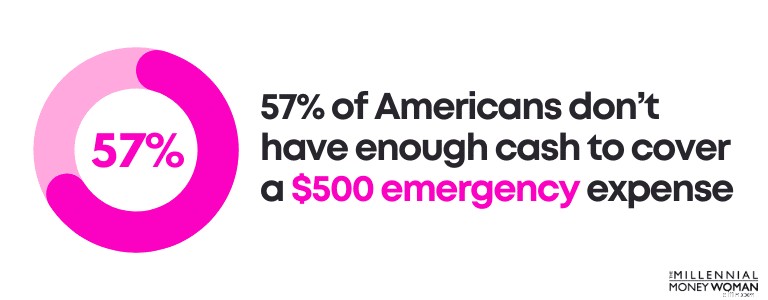

Did you know that 57% of Americans don’t have enough cash to cover a $500 emergency expense?

Unexpected emergencies happen all the time, like:

- A flat tire

- A vet visit

- A leaky roof

Unexpected events are simply part of life – so it’s up to us to get prepared for the surprise curve balls that life will throw us from time to time.

We do so by using an emergency savings fund.

Here’s how to tailor your emergency savings fund account to your personal situation:

- Determine your monthly basic living needs

- Multiply this number by 3-6

You can typically determine your monthly basic living needs by following a budget (if you haven’t yet, check out YNAB, which is free for the first 34 days).

A budget can help you:

- Track your income

- Track your expenses

- Cut out unnecessary costs

Then, it’s time to do some math.

So, let’s say that you found out you spend about $3,000 per month on basic living needs (like rent, utilities, car payments, etc.).

Here’s the range of your emergency savings fund:

$9,000

$18,000

Now, when should you have 6 months’ worth of living expenses saved versus only 3 months’ worth of your living expenses saved?

Let’s take a look:

– You’re healthy

– Your income is stable

– You don’t have much debt

– You could easily find another job

– Your monthly cost of living is low

– Your partner/spouse has a stable income

– You have other sources of money you could use

– You have children

– Your job isn’t stable

– You carry a lot of debt

– Your income fluctuates

– You’ve had some health issues

– It would be hard to find a new job

– Your partner/spouse doesn’t have a job

Make sure you take a bigger picture look at your overall situation.

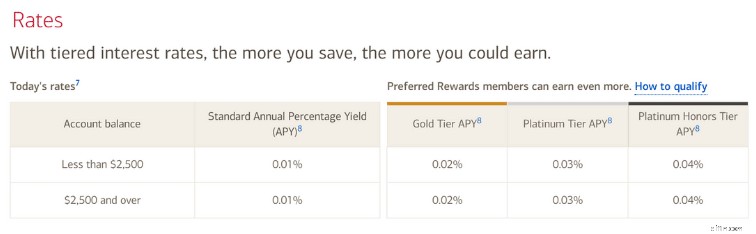

Now, if you want to start saving your cash in an emergency savings fund, I would recommend opening a high-yield online savings account as opposed to a regular bank savings account.

Here’s why:

A regular savings account from a brick-and-mortar bank (like Bank of America) offers minimal interest rates.

As you can see, interest rates range between 0.01% to 0.02%.

That’s peanuts.

Now, if you were to open an online high-yield savings account with CIT Bank (which is free), you could earn 4.05% APY.

That’s a huge difference!

On the other hand, online banks like CIT Bank generally have lower costs than brick-and-mortar stores.

For that reason, online banks can afford to give their customers high-interest rates.

And while a 4.05% interest rate is nothing like the 7% to 10% return you could be getting in the stock market, having some cash on hand for emergencies is a safe money hack to protect yourself against the unexpected.

7. Invest Your Spare Change

If you go shopping and buy something, you typically receive some form of change.

And a simple money hack is to start investing your spare change.

Pros

– Builds long term wealth

– Consistent way of investing

– Small things can make a big difference

Cons

– Slow (but consistent) progress

Best Resource

Acorns

It’s not easy to build a sizeable net worth in today’s world.

In fact, the median net worth of Americans under the age of 35 is $14,000.

If your goal is to retire early, gain financial freedom, or simply build long-term and sustainable wealth, you’ll need to start investing.

Are you ready to start investing – even if it’s just $5 a month?

If yes, then consider opening an account with Acorns 👇

Acorns is an investment platform that gives you the chance to open an account for as little as $5.

And here’s the best part: Acorns offers a feature, called the Round-Up Feature that invests your spare change!

You can also use up to a 10x round-up multiplier to fast-track your investments.

As you spend more money, the round-up feature continues to round up your spare change.

Once the rounded-up change equals $5, Acorns automatically pulls $5 from your linked checking account and invests the $5 in your Acorns account.

You spend, Acorns invests.

And that’s what I like about this money hack: It’s automatic and out of sight, out of mind.

8. Cut Your Subscriptions

Save more money almost immediately by cutting your subscriptions.

Pros

– Save money instantly by reducing your subscription costs

Cons

– Could cause some stress

– Might take some time on the phone with customer service

Best Resource

Rocket Money

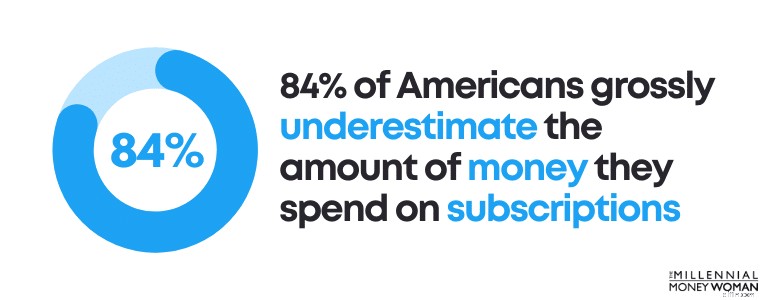

When was the last time you checked how much you pay for your subscriptions?

It’s important to review your monthly subscription spending because recent studies have shown that 84% of Americans grossly underestimate the amount of money they spend on subscriptions.

In fact, most people feel like they spend 197% less on subscription services than they actually are spending!

Why do we underestimate our subscription costs?

Below are a few reasons:

- Subscription costs increase over the months

- Subscription services are very easy to sign up to

- Some subscription costs are so low that you forget about them

Otherwise, cut the fat.

Here’s how you can trim the fat with your subscription costs:

- Review your budget

- Identify all monthly subscription costs

- Determine which subscriptions you use consistently

- Conclude with subscription services you don’t need

Once you’ve figured out which subscriptions you don’t need, you have several options open for you.

Your options may include:

- Cancel your subscription service

- Negotiate your subscription to a lower cost

- Consider sharing the cost with your friends/family

I honestly just keep the most important subscription services.

Below is a condensed list of my monthly subscriptions:

- Wifi

- Netflix

- Amazon

- Cellphone bill

- Anti-virus software

And for me, that’s about it.

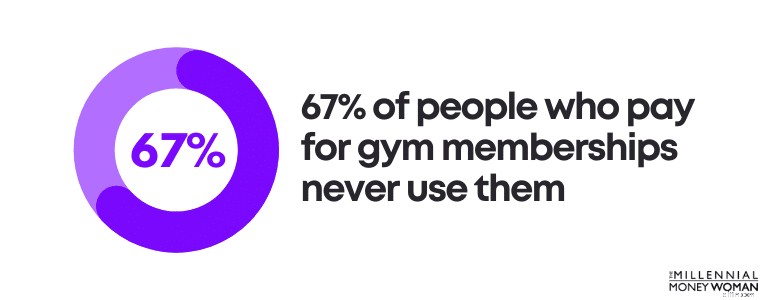

I don’t even have gym memberships – I go running on the sidewalk and I have a DVD that I purchased a very long time ago that I use every morning for training.

In fact, did you know that 67% of people who pay for gym memberships never use them?

But guess what?

You can still lower your subscription costs, even if you already trimmed the fat and cut out unnecessary subscriptions.

One way to save potentially $100’s of dollars per year is by using the service Rocket Money 👇

Rocket Money helps you get control over your subscriptions by:

- Tracking your subscriptions

- Creating a budget that works for you

- Negotiating the best rates on your subscriptions

What I like about Rocket Money is that this app creates a visual for you to better understand how much you are spending and for which subscription service.

Here’s the other cool part about Rocket Money:

It negotiates your subscription costs for you so you get the best possible rates.

Rocket Money could save you money by:

- Lowering your cable bills

- Getting refunds on late fees

- Lowering your cell phone bills

- Getting refunds on overdraft fees

- Lowering your car insurance bills

Cutting your subscription services is one of the best money hacks because you can save so much money in the long run.

9. Get a Cash Back Reward App

If you’re a savvy money saver, then perhaps one of the best money hacks for you is to sign up for a free cash back reward app.

Pros

– With every purchase you make, you earn a little money

Cons

– Only partner stores will give you the cash back offer

– Could take some time getting used to uploading receipts

Best Resource

Drop

Believe it or not, you can actually make money while you go shopping for your everyday items by downloading cash back reward apps.

For example, you can earn money back on things like:

- Travel

- Clothing

- Fast food

- Groceries

…You get my point.

One of the best apps to earn money while you go shopping for your everyday items is the cash back app, Drop (it’s free) 👇

Remember: It’s important to continue with your regular shopping behavior.

Keep in mind that not every store you shop at will offer cash back rewards with Drop.

Whether you earn a cash back reward depends on whether the store you shop at has partnered with cash back rewards apps.

Drop has partnered with over 2,000 retailers, including:

- Kroger

- Staples

- Expedia

- Walmart

- Ulta Beauty

- The Home Depot

Clearly, there is a big list of stores that you can use to shop from.

Cash back rewards could be a great money hack for you to save some extra cash – especially if you shop at the major retailers that are partnered with your cash back apps.

10. Earn Money While Watching TV

One of my favorite money hacks is earning money while watching TV by completing online surveys.

Pros

– Earn money quickly

Cons

– Time-consuming

– Not a fast way to get rich

– You only earn between $0.25 to $0.75 per survey

Best Resource

ySense

I was shocked the first time I heard that I could earn money:

- Watching TV

- In my pajamas

- While eating breakfast

That sounded pretty epic to me.

How can you earn money in such a lazy fashion?

By signing up to survey websites like with ySense (it’s free) 👇

With survey platforms like ySense, you don’t just get paid to take surveys.

In fact, you can get paid if you:

- Play games

- Take surveys

- Review products

- Join focus groups

- Share your opinions

- Share digital browsing activity

I started earning money from online survey platforms back when I was in college – especially on those days where I didn’t have any classes, studying, or work.

It was such a great (and easy) way to earn extra cash.

I should also mention that taking each survey could likely take between 5 to 20 minutes, so this is only a good option if you’re doing something on the side (like watching TV).

With Survey Junkie, (one of the most popular online survey platforms), you get paid in points (typically 1 point = 1 cent) and you can redeem these points for cash by requesting a payout either through:

- PayPal

- Gift cards

Typically speaking, you’ll need at least $10 in your account (or 1,000 points) to redeem and withdraw your cash.

There are other platforms where you could also earn money by completing surveys, watching videos, reading emails, and the like.

These alternative (free) platforms include:

- MyPoints

- Swagbucks

- Zap Surveys

- Inbox Dollars

If you’re looking to earn a few dollars here and there, completing online surveys is definitely a great money hack to consider.

11. Build Your Credit

Did you know that building credit is a money hack that can save you a lot of money down the road?

Pros

– Improved credit could decrease interest rates for big ticket purchases

Cons

– Could take time

– Could hurt more if you miss any payments

Best Resource

Self

Are you a college student with no credit or are you just emerging from a nasty bankruptcy and/or divorce, so your credit took a nosedive?

Then it’s important to rebuild your credit ASAP.

Credit can help you get access to:

- Car loans

- Credit cards

- Business loans

- Mortgage for a home

If you have a good credit score, typically it’s a lot easier to get access to loans – and good credit also typically gives you a lower interest rate on the loans you plan to take out (which means more money in your pocket).

So what is good credit, exactly?

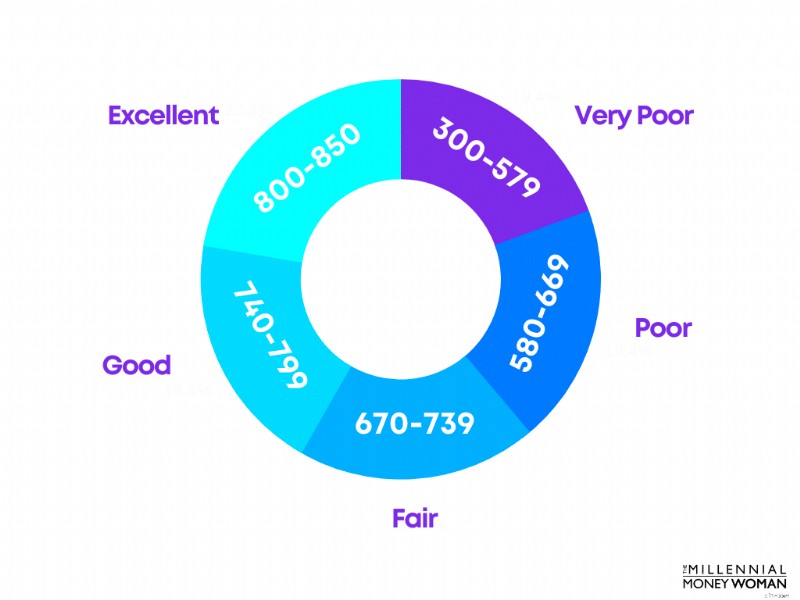

Your credit score is commonly determined by what is known as your FICO® Score, and scores generally range from 300 to 850.

Check out the FICO® Scores below:

You’ll want to aim for a minimum credit score of around 670 to 739.

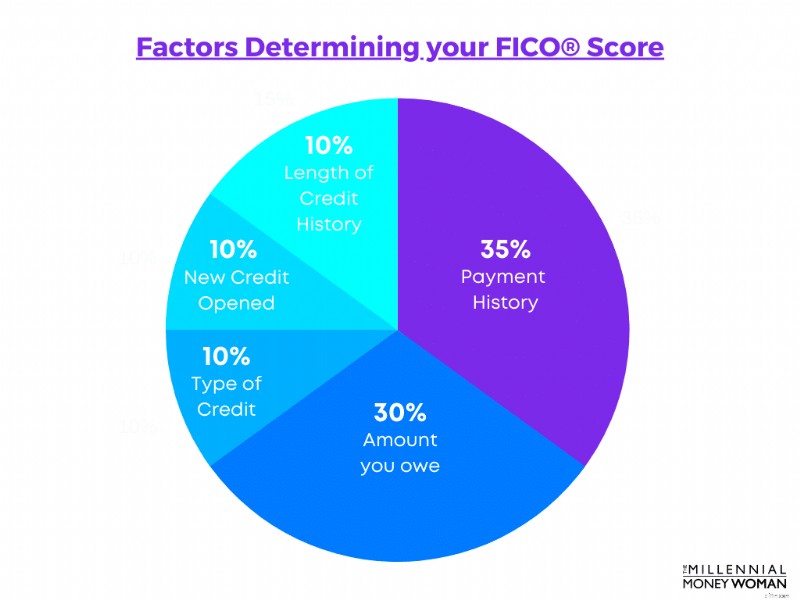

However, building up a good credit score typically takes time, because a large percent of your FICO® Score is based on your payment history.

Take a look at the components making up your FICO® Score, below:

On the bright side, only a very small percent of Americans have a low credit score, with 11.1% of Americans maintaining a FICO® Score below 550.

Good credit scores not only get you access to loans for big-ticket purchases, but good credit scores can also help you save money in the long run.

Here’s a list of reasons why good credit scores can make a difference:

- Can lower car insurance rates

- You can borrow at lower interest rates

- Increased chance for credit card approval

- Faster approval to rent homes/apartments

- Could avoid security deposits for utility services

Well, if you have no credit or if your credit is poor, I have an app for you.

The best DIY credit builder app, in my opinion, is known as Self 👇

Self, in effect, is a credit builder loan.

Here’s how it works:

- You take out a “loan”

- The loan is not immediately deposited into your bank account

- Instead, the loan is held in an FDIC insured CD, in your name

- You make timely payments in full to unlock the loan in the CD

After you’ve made all payments for the loan, the money held in the FDIC insured CD is released to you.

I like credit builder loans because they can help you:

- Establish a payment history

- Establish your credibility to make timely payments

- Help boost your credit score, as your transactions are reported to the credit bureaus

The “loan” itself could be for as little as $600 to $1,800 dollars, and you could repay your loan for either $25 to $150 per month.

You could also pay back your loan early.

Every time you make a payment, your transaction is reported to the 3 credit bureaus, so your credit score increases!

12. Meal Prep

One of the ultimate money hacks is preparing, cooking, and freezing your meals the Sunday before your workweek starts.

Pros

– Saves you hassle

– Saves you money

Cons

– Takes time

– Could be stressful cooking so much food

Did you know that the average American spends about $3,000 per year in just eating out?

You might be thinking that it’s not possible to spend $3,000 on food that’s prepared outside of your home – and that’s where I encourage you to take a look at your budget.

Eating out is expensive.

In fact, restaurants, on average, markup their food by roughly 300% so they make a profit!

I don’t blame restaurants, because they have to make their money somewhere, right?

If you’re going out to eat, then you’re really paying for:

- Service

- Convenience

- The type of food

Instead of paying the 300% markup number and eating food that wasn’t handled by you, consider meal prepping.

Each meal, be it lunch or dinner, is prepared in advance and frozen so that all you have to do, is take out your frozen meal, heat it up, and eat it!

Now, obviously meal prepping isn’t just fun and fashion.

Here are some things that go into meal-prepping:

- Money – you have to buy groceries in bulk

- Time – you have to find time to cook your meals

- Skills – you have to be somewhat comfortable with cooking

- Comfort – you have to be ok bringing lunch to work instead of eating out

When you do go bulk grocery shopping, remember you can use cash back rewards apps like Drop, where you can earn money on everyday grocery items!

If and when you do decide to eat out, I would highly suggest tracking your expenses in a budget.

If you haven’t yet, consider opening an account with YNAB (it’s free for 34 days!) to track your expenses and give you a better idea on your budget.

Below are some of the best foods that I used to meal prep:

- Pasta and meat

- Chicken and rice

- Hard-boiled eggs

- Salad and salmon

- Chicken and salad

Granted, not all of my meals would last for exactly 7 days, sometimes my meal prepping efforts would only last for a few days – which is perfectly ok.

Meal prepping is a great money hack to help you save money and get ahead of your budget.

13. Optimize Your 401k (or 403b) Investing Strategy

Did you know that one of the most important money hacks is optimizing your employer-sponsored retirement plan?

Pros

– Grow your wealth for the long term

Cons

– You have to stay invested even if markets are volatile

Best Resource

Blooom

Employer-sponsored retirement plans are structured to help you prepare and save more money for your retirement.

Employer-sponsored retirement plans include:

- 401(k)’s

- 403(b)’s

- 457(b)’s

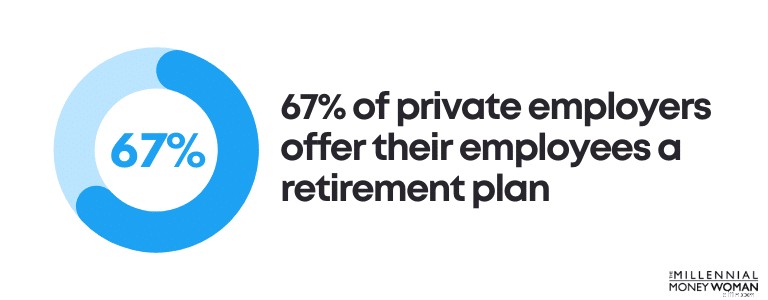

In fact, in the modern-day and age, 67% of private employers offer their employees access to a retirement plan.

Typically speaking, 401(k) plans are the most common type of employer-sponsored retirement plan.

Do you have access to an employer retirement plan?

If so, it’s time to take a look at your investments and how you can optimize your money in the stock market.

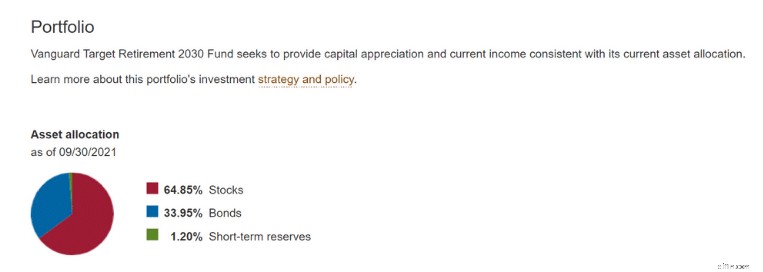

Typically speaking, when you enroll in your employer-sponsored plan, you typically are slotted into a pre-set investment fund, which often is a target-date fund.

In other words, with a target-date fund, you typically don’t have to do anything except continue making your contributions.

The closer the current year to the target date fund year, the more conservatively invested the fund will be.

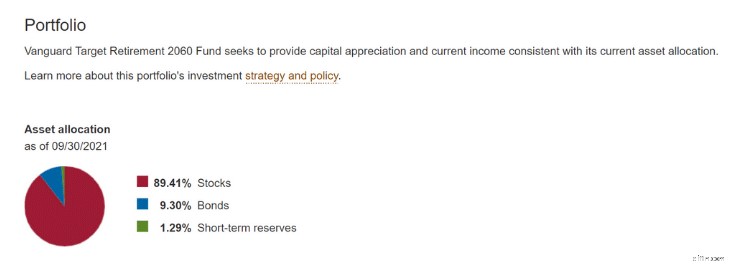

As an example, the 2030 target-date fund (above) has 65% of the assets in stocks and 33% of the assets in bonds.

Now compare the 2030 target-date fund to a 2060 target-date fund, for example.

As you can see, the further out your expected retirement date, the more tilted your asset allocation will be toward stocks.

Stocks offer more growth opportunities in the long run.

So what are the pros and cons of target-date funds?

Simple

Typically more expensive than other investment options

You don’t have to do anything

No flexibility

Professionally managed fund

No customization

Personally speaking, I would not want to pay more for a product that’s not even customized to my risk tolerance and my life goals.

Does that sound like you, too?

If so, then I would suggest you consider downloading the app known as Blooom (yes, that’s with 3 o’s!).

Blooom integrates with your employer-sponsored retirement plan (like a 401(k)) as well as with your Traditional and Roth IRAs, and offers a customized investment management approach to your money.

Here’s why you should use Blooom:

- Reduces your hidden expense ratios

- Builds a customized investment portfolio

- Adjusts your investments throughout the year

- Builds a portfolio based on your financial goals

All you have to do is link your retirement accounts with Blooom, and the investment app helps you stay on track with your portfolio.

While customizing your investment account allocation might not seem like a major money hack today, in the future, having a customized portfolio that helps reduce hidden fees could help you save $100,000’s.

14. Buy Cheap Term Life Insurance

If you’re young and you’re planning to start a family, then buying life insurance should be on your priority list.

Pros

– Financially protect your family

– Pass a death benefit on, tax-free

– Term life insurance is the cheapest form of life insurance

Cons

– May take some time to sign up

– You’ll have to go through underwriting and potentially medical exams

Best Resource

Fabric

One of my all-time favorite money hacks is buying cheap term life insurance as a Millennial to financially protect my family.

If you outlive the term, you don’t get your money back and your life insurance coverage disappears.

If you don’t outlive the term, the death benefit of your life insurance will be passed on to your beneficiaries tax-free.

Here are some of the pros and cons of term life insurance:

Low premiums

Covers only your selected term

Death benefit is tax-free

No cash value

May be converted to whole life insurance in some cases

No flexibility in premium payment options

Very good option for young people

Difficult to apply to term life insurance if you’re no longer healthy

Term life insurance is a great option for Millennials, which is why I am also such a proponent of this type of insurance.

Here is why Millennials should consider term life insurance:

- It’s cheap

- You’re not overspending money on life insurance

- Millennials are typically healthy, so premiums will be even lower

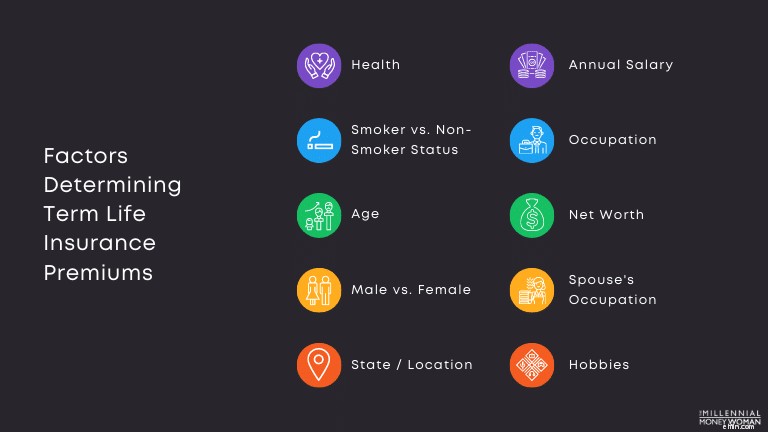

The cost of your term life insurance is not just determined by the status of your health, however.

In fact, there are many additional factors that come into play when determining the cost of your term life insurance premiums, some of which I have listed out below:

Another major factor that determines your premiums is, of course, the amount of death benefit that you select for your term life insurance policy.

Whenever someone says they need a certain “amount” of life insurance, they are actually referring to the death benefit.

While there are many factors that go into determining how much life insurance you need, below are some key pointers to consider:

- Income

- Children

- Total debt

- Work status

- Marital status

Below is a typical formula you can use to determine how much life insurance you’ll actually need:

If you’re ready to take a closer look at life insurance for yourself and your loved ones, then I’d suggest checking out Fabric 👇

With Fabric’s quick 60-second quiz, you can find out what kind of coverage your family needs, and apply for a policy in just 10 minutes.

- No price changes—guaranteed

- $1 million in coverage for less than $1 a day

- Coverage ranging from 10-30 years and policies from $100,000–$5,000,000

- 30-day money back guarantee, and you can cancel at any time

Qualified applicants could go from “Start” to “Covered” in just 10 minutes, no health exam required.

Leave the insurance part to Fabric so you can focus on life.

Money Saving Hacks: The Bottom Line

Yesterday would have been the best time to take action with these money hacks.

Today is the next best option.

While reading and doing your research is important (obviously), it’s not everything.

You cannot win without action.

In the end, it’s important you’re happy with the financial choices you make today for tomorrow.

Implement these money hacks now and your bank accounts will thank me later!

-

Understanding Asset Types: A Comprehensive Guide

An asset is a resource owned or controlled by an individual, corporationCorporationA corporation is a legal entity created by individuals, stockholders, or shareholders, with the purpose of operating

-

2021 Crypto Investment Guide: Top Coins & Predictions

Cryptocurrencies have been on the market for some years now and have undoubtedly proven to be among the most profitable investment opportunities, beating the profits from conventional stocks and com

Personal finance

- Top 10 Remote Jobs for Location Independence & Work-Life Balance

- Financial Readiness: Key Money Questions to Tackle Before 30

- Automate Your Savings: 2 Powerful Benefits & How-To

- Debt Consolidation: A Comprehensive Guide to Benefits & Drawbacks

- Protect Yourself: 3 Steps to Prepare for Potential Rent Increases

- Child Tax Credit Update: Why Extending the Enhanced Credit Matters

- Empowering Financial Independence in Adult Children: A Comprehensive Guide

- Side Hustle Reality Check: 4 Things to Consider Before You Start

- Credit Card Fraud Dispute: A Step-by-Step Guide to Winning

-

New York Considers 3-Year Ban on Bitcoin Mining Due to Energy Concerns

New York Considers 3-Year Ban on Bitcoin Mining Due to Energy ConcernsNew York lawmakers have submitted a bill banning cryptocurrency mining operations for three years.Introduced on Monday, bill S6486 seeks to put a moratorium on the operation of cryptocurrency mining c...

-

DIRECTV STREAM Review 2024: Features, Price & Performance

DIRECTV STREAM Review 2024: Features, Price & PerformanceCanceling cable is a terrific way to save money. Switching to a live TV streaming service can easily shave $100 per month off your entertainment costs. Although on the pricey end of cable replacement...