Understanding Asset Types: A Comprehensive Guide

An asset is a resource owned or controlled by an individual, corporationCorporationA corporation is a legal entity created by individuals, stockholders, or shareholders, with the purpose of operating for profit. Corporations are allowed to enter into contracts, sue and be sued, own assets, remit federal and state taxes, and borrow money from financial institutions., or government with the expectation that it will generate a positive economic benefit. Common types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and classifying the types of assets is critical to the survival of a company, specifically its solvency and associated risks.

The International Financial Reporting Standards (IFRS) framework defines an asset as follows: “An asset is a resource controlled by the enterprise as a result of past events and from which future economic benefits are expected to flow to the enterprise.”

Examples of assets include:

- Cash and cash equivalents

- Accounts Receivable

- InventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a

- Investments

- PPE (Property, Plant, and Equipment)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

- Vehicles

- Furniture

- Patents (intangible asset)

Properties of an Asset

There are three key properties of an asset:

- Ownership: Assets represent ownership that can be eventually turned into cash and cash equivalents

- Economic Value: Assets have economic value and can be exchanged or sold

- Resource: Assets are resources that can be used to generate future economic benefits

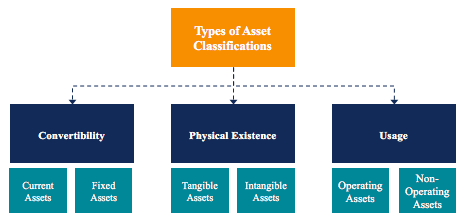

Classification of Assets

Assets are generally classified in three ways:

- Convertibility: Classifying assets based on how easy it is to convert them into cash.

- Physical Existence: Classifying assets based on their physical existence (in other words, tangible vs. intangible assets).

- Usage: Classifying assets based on their business operation usage/purpose.

Classification of Assets: Convertibility

If assets are classified based on their convertibility into cash, assets are classified as either current assets or fixed assets. An alternative expression of this concept is short-term vs. long-term assets.

1. Current Assets

Current assets are assets that can be easily converted into cash and cash equivalents (typically within a year). Current assets are also termed liquid assets and examples of such are:

- Cash

- Cash equivalents

- Short-term deposits

- Accounts receivables

- Inventory

- Marketable securities

- Office supplies

2. Fixed or Non-Current Assets

Non-current assets are assets that cannot be easily and readily converted into cash and cash equivalents. Non-current assets are also termed fixed assets, long-term assets, or hard assets. Examples of non-current or fixed assets include:

- Land

- Building

- Machinery

- Equipment

- Patents

- Trademarks

Classification of Assets: Physical Existence

If assets are classified based on their physical existence, assets are classified as either tangible assets or intangible assets.

1. Tangible Assets

Tangible assets are assets with physical existence (we can touch, feel, and see them). Examples of tangible assets include:

- Land

- Building

- Machinery

- Equipment

- Cash

- Office supplies

- Inventory

- Marketable securities

2. Intangible Assets

Intangible assets are assets that lack physical existence. Examples of intangible assets include:

- Goodwill

- Patents

- Brand

- Copyrights

- Trademarks

- Trade secrets

- Licenses and permits

- Corporate intellectual property

Classification of Assets: Usage

If assets are classified based on their usage or purpose, assets are classified as either operating assets or non-operating assets.

1. Operating Assets

Operating assets are assets that are required in the daily operation of a business. In other words, operating assets are used to generate revenue from a company’s core business activities. Examples of operating assets include:

- Cash

- Accounts receivable

- Inventory

- Building

- Machinery

- Equipment

- Patents

- Copyrights

- Goodwill

2. Non-Operating Assets

Non-operating assets are assets that are not required for daily business operations but can still generate revenue. Examples of non-operating assets include:

- Short-term investments

- Marketable securities

- Vacant land

- Interest income from a fixed deposit

Importance of Asset Classification

Classifying assets is important to a business. For example, understanding which assets are current assets and which are fixed assets is important in understanding the net working capital of a company. In the scenario of a company in a high-risk industry, understanding which assets are tangible and intangible helps to assess its solvency and risk.

Determining which assets are operating assets and which assets are non-operating assets is important to understanding the contribution of revenue from each asset, as well as in determining what percentage of a company’s revenues comes from its core business activities.

Related Readings

We hope you’ve enjoyed reading CFI’s guide to types of assets. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst.

To keep advancing your career, the additional resources below will be useful:

- Net Identifiable AssetsNet Identifiable AssetsNet Identifiable Assets consist of assets acquired from a company whose value can be measured, used in M&A for Goodwill and Purchase Price Allocation.

- Marketable SecuritiesMarketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion.

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

-

Capital Expenditures (CAPEX): Definition & Examples

Capital expenditures refer to funds that are used by a company for the purchase, improvement, or maintenance of long-term assetsLong Term AssetsLong term assets are assets that a company uses in its p

-

Understanding Cash Equivalents: Definition & Examples

Cash includes legal tender, bills, coins, checks received but not deposited, and checking and savings accounts. Cash equivalents are any short-term investment securities with maturity periods of 90 da

Accounting

- Cash Budget: Benefits & How to Limit Expenses - [Year]

- Understanding Intangible Assets: Key Characteristics & Value

- Understanding Audit Opinions: Types and What They Mean

- Biological Assets: Definition, Examples & Accounting

- Understanding Depreciation Methods: A Comprehensive Guide

- Understanding Financial Assets: Definitions & Types

- Understanding Intangible Assets: Definition & Importance

- Understanding Liability Types: Current, Non-Current & Contingent

- Liquid Assets: Definition, Importance & Examples | [Your Brand Name]

-

Understanding Accounting Transactions: A Comprehensive Guide

Understanding Accounting Transactions: A Comprehensive GuideAccounting transactions refer to any business activity that results in a direct effect on the financial status and financial statementsThree Financial StatementsThe three financial statements are the ...

-

Understanding Life Insurance Types: Term vs. Whole Life & More

Understanding Life Insurance Types: Term vs. Whole Life & MoreThe decision to purchase life insurance is daunting enough without considering the many types of life insurance. The purpose of life insurance is to protect your family’s financial future if you pass ...