Half-Year Convention for Depreciation: Understanding the Rules

The half-year convention for depreciation assumes fixed assetsFixed AssetsFixed assets refer to long-term tangible assets that are used in the operations of a business. They provide long-term financial benefits have been in service for one-half of its first year despite when it was actually acquired. This rule is applied by tax authorities to restrict the maximum allowable claim for depreciation to one half of the annual amount.

The other half of the depreciation is applied to the final year the asset is depreciated, also under the assumption that the asset will no longer be used or disposed of halfway through that final year. The half-year convention applies to all forms of depreciation methods, such as straight-line depreciationStraight Line DepreciationStraight line depreciation is the most commonly used and easiest method for allocating depreciation of an asset. With the straight line, sum-of-the-years digits, modified accelerated cost recovery systems, and double-declining balance.

Summary

- The half-year depreciation convention is a tax rule that assumes the asset is obtained and disposed of partly through the acquisition and disposal year. The maximum allowable depreciation amount is therefore half the annual amount.

- It is crucial to remember that deprecation is halved in the first year, with the remainder of that depreciation being taken in the last year of the asset’s useful life.

- Rules created by the U.S. Internal Revenue Service (IRS) aim to prevent manipulation of tax deductions by restricting the maximum allowed.

Half-Year Convention for Depreciation Example

The allocation of depreciation for the half-year convention can be difficult to grasp. To get a better understanding, an example of a half-year convention with a depreciation schedule is shown below.

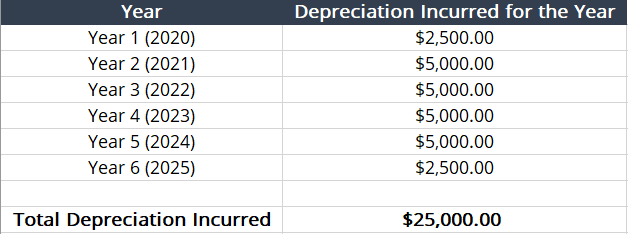

Example: Company A purchases a manufacturing machine for $25,000 on March 1, 2020. The manufacturing machine’s useful life is five years. With the application of a half-year convention, the depreciation schedule is as follows:

- Straight-line Depreciation = Cost of Asset / Useful Life = ($25,000 / 5) = $5,000 per year.

- Application of Half-year Convention = ($5,000 / 2) = $2,500 for first and additional year.

- Depreciation Schedule:

As the table shows, the first year of depreciation is halved due to the half-year convention. To make up for it, an extra year is added to the end of the depreciation scheduleDepreciation ScheduleA depreciation schedule is required in financial modeling to link the three financial statements (income, balance sheet, cash flow) in Excel..

What is a Depreciation Convention?

A depreciation convention is a rule that is used to determine four different criteria:

- The depreciation method you can use

- The depreciation schedule you can use, dependent on the useful life

- The amount of depreciation that can be claimed once the fixed asset is disposed of

- The amount of depreciation that can be claimed in the first and last year of the fixed asset’s recovery period

As a whole, depreciation conventions govern when and how depreciation is calculated.

Types of Depreciation Conventions

As for the types of depreciation conventions, nine conventions govern when and how depreciation is calculated. The conventions are listed and discussed below:

- FM = Full Month: The fixed asset receives a full month of depreciation during the month when it is placed in service. It does not receive depreciation for the month of disposal.

- HM = Modified Half Month: If the fixed asset is put into service during the first half of the month, it receives a full month of depreciation. If it is put into service during the second half of the month, the calculation of depreciation begins the preceding month.

- MM = Mid-Month: The fixed asset receives half a month of depreciation for the month it was placed into service and half a month of depreciation when disposed of.

- NM = Next Month: Depreciation for the fixed asset begins one month after it is placed into service and receives one month of depreciation when disposed of.

- HY = Half-Year: Depreciation is halved for the first and last year once it is in service.

- MY = Modified Half-Year: If put into service before the midpoint of the year, the fixed asset receives a full year of depreciation for the first year, but none on the last. If put into service after the midpoint of the year, depreciation is calculated the following year. Also, a full year of depreciation is received once disposed of.

- FY = Full Year: The fixed asset received a full year of depreciation when put into service and when it is disposed of.

- AD = Actual Days: The fixed asset receives depreciation every day it is in service during a company’s fiscal year.

- MQ = Mid-Quarter: The fixed asset receives half of one quarter’s depreciation for the quarter that it was placed into service. Same situation for disposal.

Tax Implications

How and when depreciation is calculated directly affects an organization’s tax status. A half-year convention does not require taxpayers to prove when the fixed asset was placed into service. Instead, the U.S. Internal Revenue Service (IRS) created a rule that assumes fixed assets are placed into service on July 1st of the year it was actually placed in service.

The IRS created the rule because taxpayers would be enticed to purchase fixed assets in the second half of the year and aggressively claim full depreciation deductions. As for taxpayers, the rule clearly outlines how much depreciation can be deducted in the first year as the asset is assumed to be put into service on July 1st.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Day-Count ConventionDay-Count ConventionA day-count convention is a methodology that determines the number of days that interest accrues between coupon payment days.

- Depreciated CostDepreciated CostDepreciated cost is the remaining cost of an asset after reducing the asset’s original cost by the accumulated depreciation. Understanding

- Double Declining Balance DepreciationDouble Declining Balance DepreciationThe double declining balance depreciation method is a form of accelerated depreciation that doubles the regular depreciation approach. It is

- Depreciation Methods TemplateDepreciation Methods TemplateThis depreciation methods template will show you the calculation of depreciation expenses using four types of commonly use depreciation methods. There are several types of depreciation expense and different formulas for determining the book value of an asset. The most common depreciation methods include: Straight-line

-

Understanding Estate Tax Caps: Federal & State Inheritance Limits

In discussions about death taxes, we sometimes use the terms "estate tax" and "inheritance tax" interchangeably, but they actually describe two distinct taxes. Estate tax is levied

-

Coast FIRE: A Simplified Guide to Early Retirement Savings

The Coast FIRE movement is a new approach to retirement savings. Heres what you need to know about how it could affect your retirement plan. (iStock) There are many different strategies for retirement

Accounting

- Hollister Co. Stock Symbol: ANF | Abercrombie & Fitch

- 3-for-1 Stock Split: Definition, Reasons & Impact

- Understanding Accumulated Depreciation: A Comprehensive Guide

- Allowance for Doubtful Accounts: Definition & Purpose

- Alternative Depreciation System (ADS): Definition & IRS Requirements

- Carrying Amount: Definition, Calculation & Importance

- Understanding Depreciation Methods: A Comprehensive Guide

- Double Declining Balance Depreciation: Definition & Calculation

- The 4% Rule: A Comprehensive Guide to Retirement Withdrawals

-

Land Buying Process: A Comprehensive Guide

Land Buying Process: A Comprehensive GuideWhat Is the Process for Buying Land? The goal of the process is to ultimately buy a piece of land, and this means making a reasonable offer on something up for sale. The process will not be t...

-

Burger King Stock Symbol: Find the Investor Code (BKC)

Burger King Stock Symbol: Find the Investor Code (BKC)What Is the Stock Symbol for Burger King? Burger King is a fast food hamburger restaurant, and is one of the "big three" (along with McDonald's and Wendy's) in the United St...