Understanding Depreciation Methods: A Comprehensive Guide

There are several types of depreciation expenseDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in. and different formulas for determining the book valueBook ValueBook value is a company’s equity value as reported in its financial statements. The book value figure is typically viewed in relation to the of an asset. The most common depreciation methods include:

- Straight-line

- Double declining balance

- Units of production

- Sum of years digits

Depreciation expense is used in accounting to allocate the cost of a tangible assetTangible AssetsTangible assets are assets with a physical form and that hold value. Examples include property, plant, and equipment. Tangible assets are over its useful life. In other words, it is the reduction in the value of an asset that occurs over time due to usage, wear and tear, or obsolescence. The four main depreciation methods mentioned above are explained in detail below.

1. Straight-Line Depreciation Method

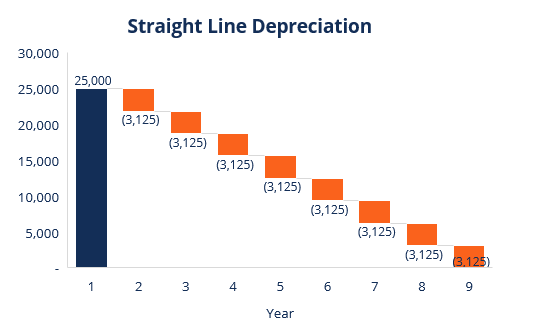

Straight-line depreciationStraight Line DepreciationStraight line depreciation is the most commonly used and easiest method for allocating depreciation of an asset. With the straight line is a very common, and the simplest, method of calculating depreciation expense. In straight-line depreciation, the expense amount is the same every year over the useful life of the asset.

Depreciation Formula for the Straight Line Method:

Depreciation Expense = (Cost – Salvage value) / Useful life

Example

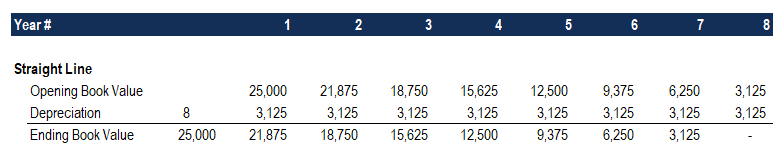

Consider a piece of equipment that costs $25,000 with an estimated useful life of 8 years and a $0 salvage value. The depreciation expense per year for this equipment would be as follows:

Depreciation Expense = ($25,000 – $0) / 8 = $3,125 per year

2. Double Declining Balance Depreciation Method

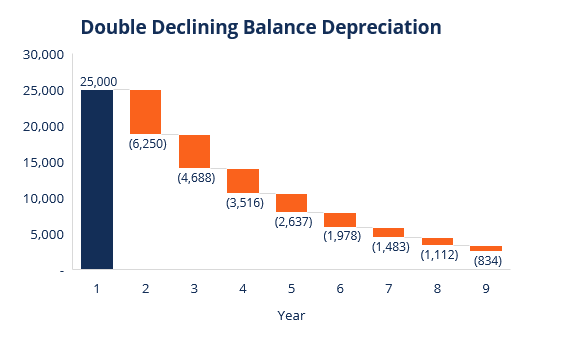

Compared to other depreciation methods, double-declining-balance depreciationDouble Declining Balance DepreciationThe double declining balance depreciation method is a form of accelerated depreciation that doubles the regular depreciation approach. It is results in a larger amount expensed in the earlier years as opposed to the later years of an asset’s useful life. The method reflects the fact that assets are typically more productive in their early years than in their later years – also, the practical fact that any asset (think of buying a car) loses more of its value in the first few years of its use. With the double-declining-balance method, the depreciation factor is 2x that of the straight-line expense method.

Depreciation formula for the double-declining balance method:

Periodic Depreciation Expense = Beginning book value x Rate of depreciation

Example

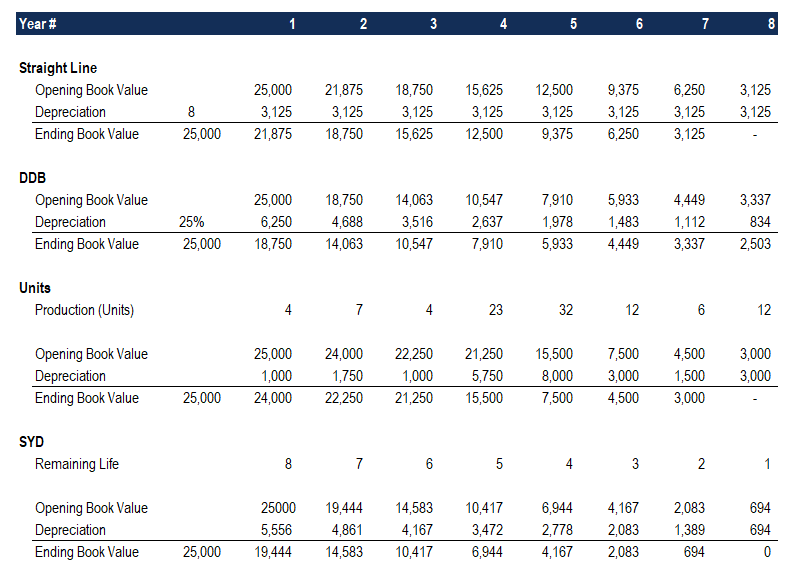

Consider a piece of property, plant, and equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex, that costs $25,000, with an estimated useful life of 8 years and a $2,500 salvage value. To calculate the double-declining balance depreciation, set up a schedule:

The information on the schedule is explained below:

- The beginning book value of the asset is filled in at the beginning of year 1 and the salvage value is filled in at the end of year 8.

- The rate of depreciation (Rate) is calculated as follows:

Expense = (100% / Useful life of asset) x 2

Expense = (100% / 8) x 2 = 25%

Note: Since this is a double-declining method, we multiply the rate of depreciation by 2.

3. Multiply the rate of depreciation by the beginning book value to determine the expense for that year. For example, $25,000 x 25% = $6,250 depreciation expense.

4. Subtract the expense from the beginning book value to arrive at the ending book value. For example, $25,000 – $6,250 = $18,750 ending book value at the end of the first year.

5. The ending book value for that year is the beginning book value for the following year. For example, the year 1 ending book value of $18,750 would be the year 2 beginning book value. Repeat this until the last year of useful life.

Learn more in CFI’s Accounting Courses.

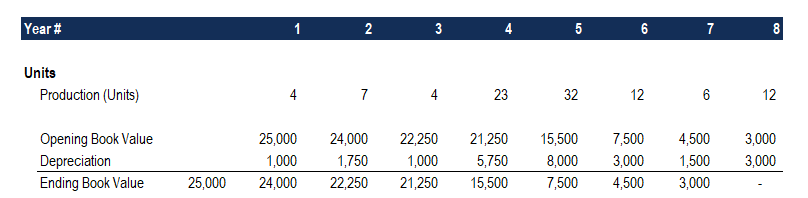

3. Units of Production Depreciation Method

The units-of-production depreciation method depreciates assets based on the total number of hours used or the total number of units to be produced by using the asset, over its useful life.

The formula for the units-of-production method:

Depreciation Expense = (Number of units produced / Life in number of units) x (Cost – Salvage value)

Example

Consider a machine that costs $25,000, with an estimated total unit production of 100 million and a $0 salvage value. During the first quarter of activity, the machine produced 4 million units.

To calculate the depreciation expense using the formula above:

Depreciation Expense = (4 million / 100 million) x ($25,000 – $0) = $1,000

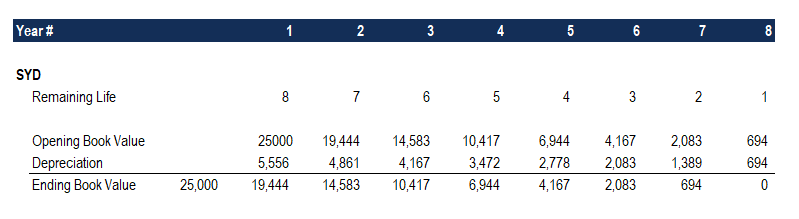

4. Sum-of-the-Years-Digits Depreciation Method

The sum-of-the-years-digits method is one of the accelerated depreciation methods. A higher expense is incurred in the early years and a lower expense in the latter years of the asset’s useful life.

In the sum-of-the-years digits depreciation methodAccountingOur Accounting guides and resources are self-study guides to learn accounting and finance at your own pace. Browse hundreds of guides and resources., the remaining life of an asset is divided by the sum of the years and then multiplied by the depreciating base to determine the depreciation expense.

The depreciation formula for the sum-of-the-years-digits method:

Depreciation Expense = (Remaining life / Sum of the years digits) x (Cost – Salvage value)

Consider the following example to more easily understand the concept of the sum-of-the-years-digits depreciation method.

Example

Consider a piece of equipment that costs $25,000 and has an estimated useful life of 8 years and a $0 salvage value. To calculate the sum-of-the-years-digits depreciation, set up a schedule:

The information in the schedule is explained below:

- The depreciation base is constant throughout the years and is calculated as follows:

Depreciation Base = Cost – Salvage value

Depreciation Base = $25,000 – $0 = $25,000

2. The remaining life is simply the remaining life of the asset. For example, at the beginning of the year, the asset has a remaining life of 8 years. The following year, the asset has a remaining life of 7 years, etc.

3. RL / SYD is “remaining life divided by sum of the years.” In this example, the asset has a useful life of 8 years. Therefore, the sum of the years would be 1 + 2 + 3 + 4 + 5 + 6 + 7 + 8 = 36 years. The remaining life in the beginning of year 1 is 8. Therefore, the RM / SYD = 8 / 36 = 0.2222.

4. The RL / SYD number is multiplied by the depreciating base to determine the expense for that year.

5. The same is done for the following years. In the beginning of year 2, RL / SYD would be 7 / 36 = 0.1944. 0.1944 x $25,000 = $4,861 expense for year 2.

Learn more in CFI’s Accounting Courses.

Summary of Depreciation Methods

Below is the summary of all four depreciation methods from the examples above.

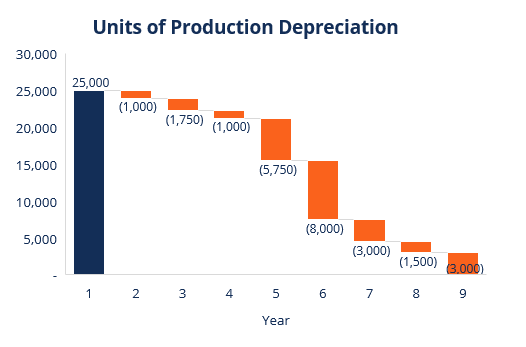

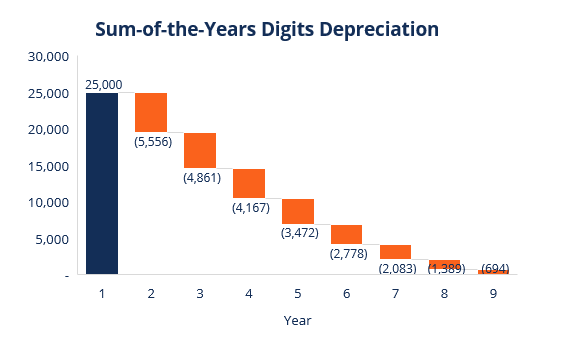

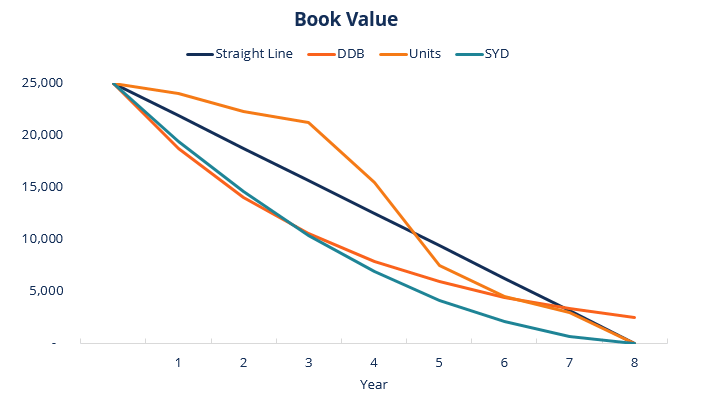

Here is a graph showing the book value of an asset over time with each different method.

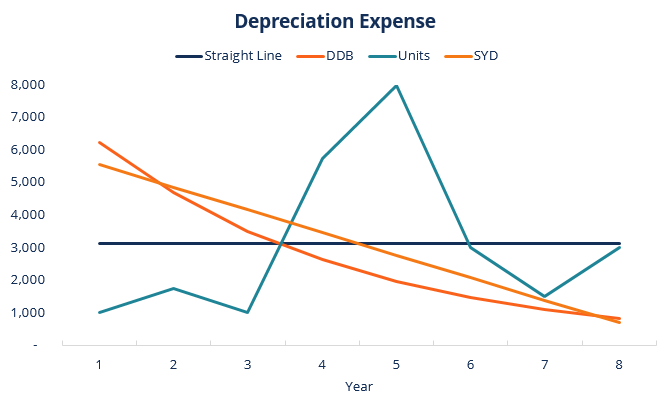

Here is a summary of the depreciation expense over time for each of the 4 types of expense.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Video Explanation of Depreciation Methods

Below is a short video tutorial that goes through the four types of depreciation outlined in this guide. While the straight-line method is the most common, there are also many cases where accelerated methodsAccelerated DepreciationAccelerated depreciation is a depreciation method in which a capital asset reduces its book value at a faster (accelerated) rate than it would are preferable, or where the method should be tied to usage, such as units of production.

Video: CFI’s Financial Analysis Courses.

More Resources

Thank you for reading this CFI guide to the 4 main types of depreciation. CFI is a global provider of financial modeling courses and financial analyst certificationBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!. To help you become a world-class financial analyst, these additional CFI resources will be helpful:

- Depreciation ScheduleDepreciation ScheduleA depreciation schedule is required in financial modeling to link the three financial statements (income, balance sheet, cash flow) in Excel.

- Depreciation ExpenseDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in.

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Property, Plant & Equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

-

Understanding Intangible Assets: Key Characteristics & Value

Assets come in three main forms: tangible, intangible and monetary. The two main characteristics of an intangible asset are that it is not physical, meaning it exists as a legal power, and that it is

-

Alternative Depreciation System (ADS): Definition & IRS Requirements

The Alternative Depreciation System (ADS) is a method of calculating the depreciation of certain types of assets in special circumstances. The ADS system is required by the Internal Revenue Service (I

Accounting

- Understanding Bank Drafts: Types, Security & How They Work

- Key Characteristics of a Successful Budget: Planning & Savings

- Understanding Currency Depreciation: Causes & Economic Factors

- Understanding Corporate Stock Classes: Common vs. Preferred

- Understanding Audit Opinions: Types and What They Mean

- Carrying Amount: Definition, Calculation & Importance

- Double Declining Balance Depreciation: Definition & Calculation

- Understanding Asset Types: A Comprehensive Guide

- Understanding Liability Types: Current, Non-Current & Contingent

-

Understanding HMO Plans: Types, Benefits & Limitations

Understanding HMO Plans: Types, Benefits & LimitationsHealth maintenance organizations, or HMOs, provide contractually defined medical services to individual patients in the U.S. Advocates point out that HMOS may provide patients with superior care at a ...

-

Understanding Cryptocurrency Wallets: A Comprehensive Guide

Understanding Cryptocurrency Wallets: A Comprehensive GuideTo buy and invest in cryptocurrencies like bitcoin, the first step is to choose the right cryptocurrency wallet. There are many digital currencies like Bitcoin, Dash, Litecoin, Ethereum, and more, a...