Weighted Average Cost (WAC): Definition & Calculation

In accounting, the Weighted Average Cost (WAC) method of inventory valuation uses a weighted average to determine the amount that goes into COGSCost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct and inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a. The weighted average cost method divides the cost of goods available for sale by the number of units available for sale. The WAC method is permitted under both GAAP and IFRSIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world accounting.

Weighted Average Cost (WAC) Method Formula

The formula for the weighted average cost method is as follows:

Where:

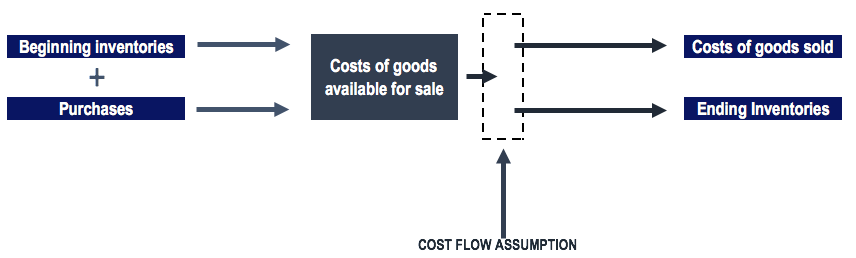

- Costs of goods available for sale is calculated as beginning inventory value + purchases.

- Units available for sale are the number of units a company can sell or the total number of units in inventory and is calculated as beginning inventory in units + purchases in units.

Understanding Costs of Goods Available for Sale

The bundling of costs is referred to as the cost of goods available for sale. The costs of goods available for sale are either allocated to COGS or ending inventory. Allocating the costs of goods available for sale is referred to as a cost flow assumption. There are several cost flow assumptions, such as:

- FIFO (first-in, first-out)

- LIFO (last-in, first-out)

- WAC (weighted average cost)

The WAC Method under Periodic and Perpetual Inventory Systems

Using the weighted average cost method yields different allocation of inventory costs under a periodic and perpetual inventory system.

In a periodic inventory system, the company does an ending inventory count and applies product costs to determine the ending inventory cost. COGS can then be determined by combining the ending inventory cost, beginning inventory cost, and the purchases throughout the period.

A perpetual inventory system keeps continual tracking of inventories and COGS. The perpetual inventory system provides more timely information for the management of inventory levels. However, this method of inventory tracking can be costly for a company. In a perpetual inventory system, the weighted average cost method is referred to as the “moving average cost method.”

Below, we will use the weighted average cost method and identify the difference in the allocation of inventory costs under a periodic and perpetual inventory system.

Example of the WAC Method

At the beginning of its January 1 fiscal year, a company reported a beginning inventory of 300 units at a cost of $100 per unit. Over the first quarter, the company made the following purchases:

- January 15 purchase of 100 units at a cost of $130 = $13,000

- February 9 purchase of 200 units at a cost of $150 = $30,000

- March 3 purchase of 150 units at a cost of $200 = $30,000

In addition, the company made the following sales:

- End of February sales of 100 units

- End of March sales of 70 units

Under the periodic inventory system, we would determine the cost of goods available for sale and the units available for sale at the end of the first quarter:

For the sale of 170 units over the January-March period, we would allocate $137.33 per unit sold. The rest would go into ending inventory. Therefore:

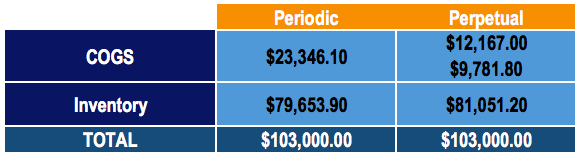

- 170 x $137.33 = $23,346.10 in COGS

- $103,000 – $23,346.10 = $79,653.90 in ending inventory

Note: The numbers may be slightly off due to rounding off.

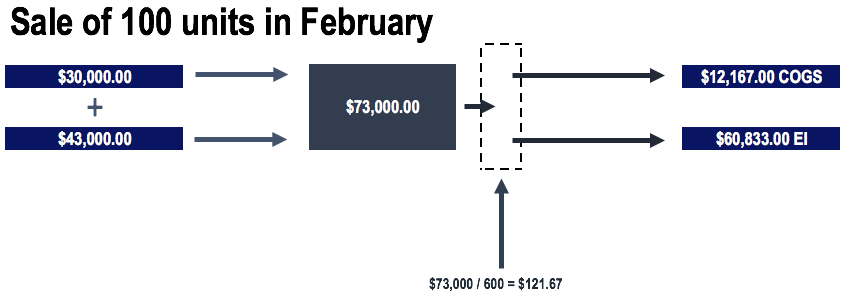

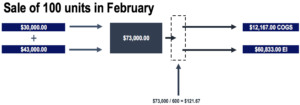

Under the perpetual inventory system, we would determine the average before the sale of units.

Therefore, before the sale of 100 units in February, our average would be:

For the sale of 100 units in February, the costs would be allocated as follows:

- 100 x $121.67 = $12,167 in COGS

- $73,000 – $12,167 = $60,833 remain in inventory

Note: The numbers may be slightly off due to rounding off.

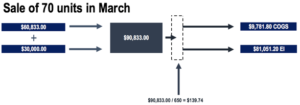

Before the sale of 70 units in March, our average would be:

For the sale of 70 units in March, the costs would be allocated as follows:

- 70 x $139.74 = $9,781.80 in COGS

- $90,833 – $9,781.0 = $81,051.20 in ending inventory

Note: The numbers may be slightly off due to rounding off.

The diagrams would look as follows under the perpetual inventory system:

Comparing the WAC Method under the Periodic and Perpetual Inventory Systems

Comparing the costs allocated to COGS and inventory, we can see that the costs are allocated differently depending on whether it is a periodic or perpetual inventory system. However, notice that the total costs remain the same (as they should).

In our example, the inventories purchased experienced a price appreciation. January purchase costs per unit were $130, February purchase costs per unit were $150, and March purchase costs per unit were $200. Therefore, since the periodic system uses the costs of goods available for sale over the entire quarter, more is allocated to the costs of goods sold for the sale of inventory.

Related Reading

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following CFI resources will be helpful:

- Days Inventory Outstanding (DIO)Days Inventory OutstandingDays inventory outstanding (DIO) is the average number of days that a company holds its inventory before selling it. The days inventory

- Inventory TurnoverInventory TurnoverInventory turnover, or the inventory turnover ratio, is the number of times a business sells and replaces its stock of goods during a given period. It considers the cost of goods sold, relative to its average inventory for a year or in any a set period of time.

- Cost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

-

Attic Insulation Costs: Average Prices & Savings

Insulating an attic is cheapest when done at the same time as other house insulation. When most homes are built, attics are insulated along with the rest of the house. But in some cases attic

-

Understanding Allowed Depreciation: Tax Deductions for Businesses

Allowed depreciation refers to the depreciation that a business is allowed to deduct from its tax liabilities. The annual depreciation of assets needs to be considered while calculating an individual&

Accounting

- Understanding Average Cost Basis: A Comprehensive Guide

- Understanding Inventory Age: A Key Metric for Business Efficiency

- Understanding Average Inventory: Definition & Calculation

- Understanding Cost of Goods Manufactured (COGM): A Managerial Accounting Guide

- Understanding Lower of Cost or Market (LCM) Inventory Valuation

- Understanding the Next-In, First-Out (NIFO) Inventory Method

- Perpetual Inventory System: Definition, Benefits & How It Works

- Weighted Average Cost Method: A Comprehensive Guide for Small Businesses

- Average Vacation Cost: A Comprehensive Breakdown for 2024

-

Window & Siding Replacement Costs: Average Prices & Factors

Window & Siding Replacement Costs: Average Prices & FactorsWhile windows and siding are two very different parts of the house, not uncommonly homeowners will replace both at the same time. Both have a strong visual impact and are often considered when renovat...

-

Average Cost Inventory Method: Definition, Calculation & Benefits

You have a business, and just like many business owners, you want to improve your bottom-line. You will need evaluation methods most common in eCommerce accounting to achieve your g...