Capital Allocation Line (CAL) & Optimal Portfolio Construction

The Capital Allocation Line (CAL) is a line that graphically depicts the risk-and-reward profile of assets, and can be used to find the optimal portfolio. The process to construct the CAL for a collection of portfolios is described below.

Portfolio expected return and variance

For the sake of simplicity, we will construct a portfolio with only two risky assets.

The portfolio’s expected return is a weighted average of its individual assets’ expected returns, and is calculated as:

E(Rp) = w1E(R1) + w2E(R2)

Where w1, w2 are the respective weights for the two assets, and E(R1), E(R2) are the respective expected returns.

Levels of variance translate directly with levels of risk; higher variance means higher levels of risk and vice versa. The variance of a portfolio is not just the weighted average of the variance of individual assets but also depends on the covariance and correlation of the two assets. The formula for portfolio variance is given as:

Var(Rp) = w21Var(R1) + w22Var(R2) + 2w1w2Cov(R1, R2)

Where Cov(R1, R2) represents the covariance of the two asset returns. Alternatively, the formula can be written as:

σ2p = w21σ21 + w22σ22 + 2ρ(R1, R2) w1w2σ1σ2, using ρ(R1, R2), the correlation of R1 and R2.

The conversion between correlation and covariance is given as: ρ(R1, R2) = Cov(R1, R2)/ σ1σ2.

The variance of portfolio return is greater when the covariance of the two assets is positive, and less when negative. Since variance represents risk, the portfolio risk is lower when its asset components possess negative covariance. Diversification is a technique that minimizes portfolio risk by investing in assets with negative covariance.

In practice, we do not know the returns and standard deviations of individual assets, but we can estimate these values based on these assets’ historical values.

The efficient frontier

A portfolio frontier is a graph that maps out all possible portfolios with different asset weight combinations, with levels of portfolio standard deviation graphed on the x-axis and portfolio expected return on the y-axis.

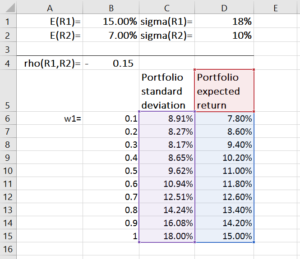

To construct a portfolio frontier, we first assign values for E(R1), E(R2), stdev(R1), stdev(R2), and ρ(R1, R2). Using the above formulas, we then calculate the portfolio expected return and variance for each possible asset weight combinations (w2=1-w1). This process can be done easily in Microsoft Excel, as shown in the example below:

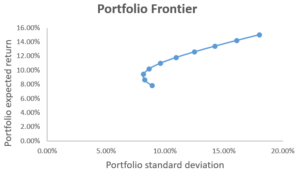

We then use the scatter chart with smooth lines to plot the portfolio’s expected return and standard deviation. The result is shown on the graph below, where each dot on the plot represents a portfolio constructed under an asset weight combination.

So how do we know which portfolios are attractive to investors? To answer this, we introduce the concept of mean-variance criterion, which states that Portfolio A dominates Portfolio B if E(RA) ≥ E(RB) and σA ≤ σB (i.e. portfolio A offers a higher expected return and lower risk than portfolio B). If such is the case, then investors would prefer A to B.

From the graph, we can infer that portfolios on the downward-sloping portion of the portfolio frontier are dominated by the upward-sloping portion. As such, the points on the upward-sloping portion of the portfolio frontier represent portfolios that investors find attractive, while points on the downward-sloping portion represent portfolios that are inefficient.

According to the mean-variance criterion, any investor would optimally select a portfolio on the upward-sloping portion of the portfolio frontier, which is called the efficient frontier, or minimum variance frontier. The choice of any portfolio on the efficient frontier depends on the investor’s risk preferences.

A portfolio above the efficient frontier is impossible, while a portfolio below the efficient frontier is inefficient.

Complete portfolio and capital allocation line

In constructing portfolios, investors often combine risky assets with risk-free assets (such as government bonds) to reduce risks. A complete portfolio is defined as a combination of a risky asset portfolio, with return Rp, and the risk-free asset, with return Rf.

The expected return of a complete portfolio is given as:

E(Rc) = wpE(Rp) + (1 − wp)Rf

And the variance and standard deviation of the complete portfolio return is given as:

Var(Rc) = w2pVar(Rp), σ(Rc) = wpσ(Rp),

where wp is the fraction invested in the risky asset portfolio.

While the expected excess return of a complete portfolio is calculated as:

E(Rc) – Rf,

if we substitute E(Rc) with the previous formula, we get wp(E(Rp) − Rf).

The standard deviation of the complete portfolio is σ(Rc) = wpσ(Rp), which gives us:

wp = σ(Rc)/σ(Rp)

Therefore, for each complete portfolio:

Or E(Rc) = Rf + Spσ(Rc), where Sp =

The line E(Rc) = Rf + Spσ(Rc) is the capital allocation line (CAL). The slope of the line, Sp, is called the Sharpe ratioSharpe RatioThe Sharpe Ratio is a measure of risk-adjusted return, which compares an investment's excess return to its standard deviation of returns. The Sharpe Ratio is commonly used to gauge the performance of an investment by adjusting for its risk., or reward-to-risk ratio. The Sharpe ratio measures the increase in expected return per unit of additional standard deviation.

Optimal portfolio

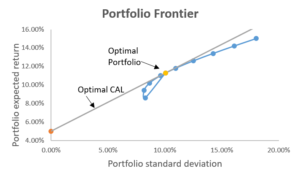

The optimal portfolio consists of a risk-free asset and an optimal risky asset portfolio. The optimal risky asset portfolio is at the point where the CAL is tangent to the efficient frontier. This portfolio is optimal because the slope of CAL is the highest, which means we achieve the highest returns per additional unit of risk. The graph below illustrates this:

The tangent portfolio weights are calculated as follows:

Summary of capital allocation line

Investors use both the efficient frontier and the CAL to achieve different combinations of risk and return based on what they desire. The optimal risky portfolio is found at the point where the CAL is tangent to the efficient frontier. This asset weight combination gives the best risk-to-reward ratio, as it has the highest slope for CAL.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Additional resources

Thank you for reading CFI’s guide to the capital allocation line. To advance your career as a Financial Modeling and Valuation AnalystBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!, these additional resources will be helpful:

- Portfolio management career profilePortfolio Management Career ProfilePortfolio management is managing investments and assets for clients, which include pension funds, banks, hedge funds, family offices. The portfolio manager is responsible for maintaining the proper asset mix and investment strategy that suits the client's needs. Salary, skills,

- Market risk premiumMarket Risk PremiumThe market risk premium is the additional return an investor expects from holding a risky market portfolio instead of risk-free assets.

- Sharpe ratio definitionSharpe RatioThe Sharpe Ratio is a measure of risk-adjusted return, which compares an investment's excess return to its standard deviation of returns. The Sharpe Ratio is commonly used to gauge the performance of an investment by adjusting for its risk.

- Sharpe ratio calculatorSharpe Ratio CalculatorThe Sharpe Ratio Calculator allows you to measure an investment's risk-adjusted return. Download CFI's Excel template and Sharpe Ratio calculator. Sharpe Ratio = (Rx - Rf) / StdDev Rx. Where: Rx = Expected portfolio return, Rf = Risk free rate of return, StdDev Rx = Standard deviation of portfolio return / volatility

-

Building a Profitable Stock Portfolio: A Beginner's Guide

Chances are, you probably know what stocks are — but what about a stock portfolio? And more importantly, how do you go about building a stock portfolio? What is a Stock Portfolio? A stock portfolio is

-

Building a Strong Financial Portfolio: A Step-by-Step Guide

If you have invested any of your money in financial instruments like stocks and bonds, then you own a financial portfolio. The following are steps you can take to further build and refine your financi

finance

- Capital vs. Money Markets: Key Differences & Similarities

- Optimal Capital Structure: Balancing Debt & Equity for Maximum Value

- Working Capital: Definition, Calculation & Importance for Business Stability

- Dynamic Asset Allocation: A Comprehensive Guide

- Portfolio Rebalancing: A Guide to Optimal Asset Allocation

- Understanding Optimal Portfolio Theory: A Beginner's Guide

- Understanding Portfolio Income and Tax Implications

- Portfolio Management & Risk: Strategies for Successful Investing

- Asset Allocation: Diversify Your Portfolio for Optimal Returns & Risk Management

-

Understanding Working Capital: Definition & Calculation

Working capital is essentially the short term capital that is at work for the company. Net working capital is usually calculated as accounts receivable plus short term assets minus accounts paya...

-

Diversifying Your Investment Portfolio: A Guide to Secure Retirement

Diversifying Your Investment Portfolio: A Guide to Secure RetirementFor decades, experts have warned Americans not to rely on Social Security as a viable way to support themselves during retirement. The Federal Government implemented Social Security in 1935...