Understanding Credit Ratings: A Comprehensive Guide

A credit rating is an opinion of a particular credit agency regarding the ability and willingness an entity (government, business, or individual) to fulfill its financial obligations in completeness and within the established due dates. A credit rating also signifies the likelihood a debtor will default. It is also representative of the credit riskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally, carried by a debt instrument – whether a loan or a bond issuance.

A credit rating is, however, not an assurance or guarantee of a kind of financial performance by a certain instrument of debt or a specific debtor. The opinions provided by a credit agency do not replace those of a financial advisorFinancial AdvisorA Financial Advisor is a finance professional who provides consulting and advice about an individual’s or entity’s finances. Financial advisors can help individuals and companies reach their financial goals sooner by providing their clients with strategies and ways to create more wealth or portfolio managerPortfolio ManagerPortfolio managers manage investment portfolios using a six-step portfolio management process. Learn exactly what does a portfolio manager do in this guide. Portfolio managers are professionals who manage investment portfolios, with the goal of achieving their clients’ investment objectives..

Who Evaluates Credit Ratings?

A credit agency evaluates the credit rating of a debtor by analyzing the qualitative and quantitative attributes of the entity in question. The information may be sourced from internal information provided by the entity, such as audited financial statements, annual reports, as well as external information such as analyst reports, published news articles, overall industry analysis, and projections.

A credit agency is not involved in the transaction of the deal and, therefore, is deemed to provide an independent and impartial opinion of the credit risk carried by a particular entity seeking to raise money through loans or bond issuance.

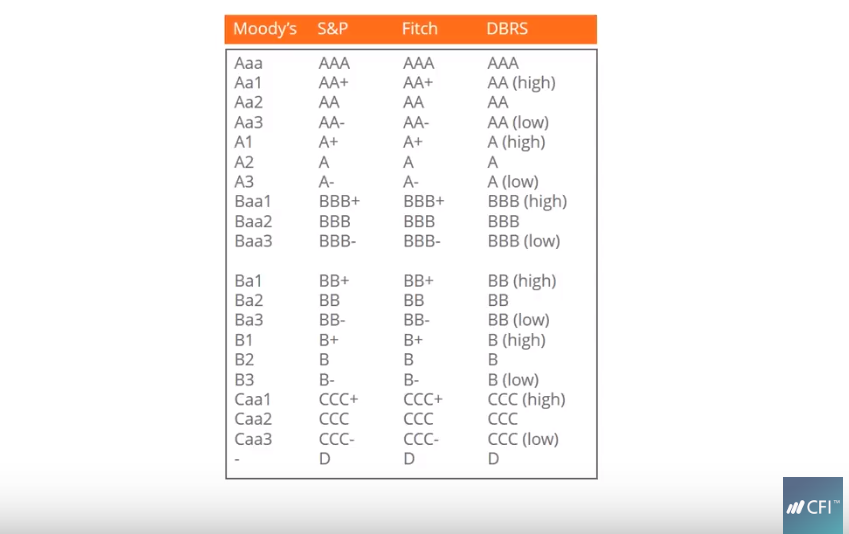

Presently, there are three prominent credit agencies that control 85% of the overall ratings market: Moody’s Investor Services, Standard and Poor’s (S&P), and Fitch Group. Each agency uses unique, but strikingly similar, rating styles to indicate credit ratings.

Types of Credit Ratings

Each credit agency uses its own terminology to determine credit ratings. That said, the notations are strikingly similar among the three credit agencies. Ratings are bracketed into two groups: investment grade and speculative grade.

- Investment grade ratings mean the investment is considered solid by the rating agency, and the issuer is likely to honor the terms of repayment. Such investments are typically less competitively priced in comparison to speculative grade investments.

- Speculative grade investments are high risk and, therefore, offer higher interest rates to reflect the quality of the investments.

Users of Credit Ratings

Credit ratings are used by investors, intermediaries such as investment banksList of Top Investment BanksList of the top 100 investment banks in the world sorted alphabetically. Top investment banks on the list are Goldman Sachs, Morgan Stanley, BAML, JP Morgan, Blackstone, Rothschild, Scotiabank, RBC, UBS, Wells Fargo, Deutsche Bank, Citi, Macquarie, HSBC, ICBC, Credit Suisse, Bank of America Merril Lynch, issuers of debt, and businesses and corporations.

- Both institutional and individual investors use credit ratings to assess the risk related to investing in a specific issuance, ideally in the context of their entire portfolio.

- Intermediaries such as investment bankers utilize credit ratings to evaluate credit risk and further derive pricing of debt issues.

- Debt issuers such as corporations, governments, municipalities, etc., use credit ratings as an independent evaluation of their creditworthiness and credit risk associated with their debt issuance. The ratings can, to some extent, provide prospective investors with an idea of the quality of the instrument and what kind of interest rate they should be expecting from it.

- Businesses and corporations that are looking to evaluate the risk involved with a certain counterparty transaction also use credit ratings. They can help entities that are looking to participate in partnerships or ventures with other businesses evaluate the viability of the proposition.

Credit Score

A credit rating is used to determine an entity’s creditworthiness, wherein an entity could be an individual, a business, a corporation or a sovereign country. In case of a loan, the rating is used to establish whether a loan should be rendered in the first place. If the process goes further, it helps in deciding the term of the loan such as dates of repayment, interest rate, etc.

In the case of bond issuance, the credit rating indicates the worthiness of the corporation or sovereign country’s ability to repay the bond payments in due time. It helps the investor evaluate whether to invest in the bond or not.

A credit score, however, is strictly for indicating an individual’s personal credit health. It indicates the individual’s ability to undertake a certain load and his or her ability to honor the terms and conditions of the loan, including the interest rate and dates of repayment. A credit score for individuals is used by banks, credit card companies, and other lending institutions that serve individuals.

Additional Resouces

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Bond IssuersBond IssuersThere are different types of bond issuers. These bond issuers create bonds to borrow funds from bondholders, to be repaid at maturity.

- Debt CapacityDebt CapacityDebt capacity refers to the total amount of debt a business can incur and repay according to the terms of the debt agreement.

- FICO ScoreFICO ScoreA FICO score, more commonly known as a credit score, is a three-digit number that is used to assess how likely a person is to repay the credit if the individual is given a credit card or if a lender loans them money. FICO scores are also used to help determine the interest rate on any credit extended

- Loan CovenantLoan CovenantA loan covenant is an agreement stipulating the terms and conditions of loan policies between a borrower and a lender. The agreement gives lenders leeway in providing loan repayments while still protecting their lending position. Similarly, due to the transparency of the regulations, borrowers get clear expectations of

-

Understanding FICO Scores: Your Key to Creditworthiness

A FICO score, more commonly known as a credit score, is a three-digit number that is used to assess how likely a person is to repay the credit if the individual is given a credit card or if a lenderTo

-

Hope Credit: Understanding Your Post-Secondary Education Tax Credit

The Hope Credit is one of the lifetime education tax credits in the U.S. that provides financial assistance to taxpayers or their children who are pursuing post-secondary education. The creation of th

finance

- Understanding A1 Credit Ratings: A Guide to Financial Strength

- Intraday Credit: Understanding Short-Term Account Overdrafts

- Credit Amnesty: Understanding the Truth & Avoiding Scams

- Understanding B Credit Ratings: What They Mean for Businesses

- Understanding Bank Ratings: A Guide to Financial Stability

- Cashback Credit Cards: A Comprehensive Guide

- Credit Analysis: A Comprehensive Guide to Assessing Credit Risk

- Understanding Credit Scores: What They Are & Why They Matter

- HELOCs Explained: Flexible Home Equity Financing

-

Understanding Credit Risk: Definition & Implications

Understanding Credit Risk: Definition & ImplicationsCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally, the failure to make required payments on loans...

-

Credit Unions Explained: What They Are & How They Benefit You

Credit Unions Explained: What They Are & How They Benefit YouA credit union is a type of financial organization that is owned and governed by its members. Credit unions provide members with a variety of financial services, including checking and savings account...