Understanding IBAN: Your Guide to International Bank Account Numbers

The International Bank Account Number – typically referred to as IBAN – is a system of identification for bank accounts that is used across national borders. Internationally agreed upon, the IBAN system acts as a facilitator for communicating and processing international transactions, helping to reduce errors in transcription.

Summary:

- The International Bank Account Number (IBAN) is a system of identification for account numbers to ensure that international transactions go smoothly.

- There were several versions of the IBAN system – put out by the International Organization for Standardization (ISO) – before a finalized version was created; the final version was split into two parts.

- IBANs are important because they enable international transactions to occur easily, and significantly help to cut down on transactional errors.

Structure of the International Bank Account Number

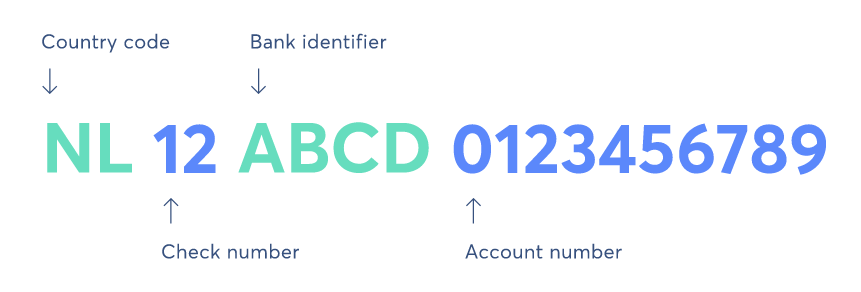

The International Bank Account Number contains the following information:

- Country code – A code that is specific to a certain country

- Check number – A two-digit code used as a redundancy check to detect errors on identification numbers

- Bank identifier – The unique identifier for the domestic bank

- Account number – The bank account identifier

Source

History of the International Bank Account Number

Before the creation of the IBAN system, there were different standards among countries when it came to identifying bank accounts (their branch, bank, account number, and routing codes). This led to a large amount of confusion when it came to international transactions. Important routing information, specifically, was often missing when payments were being made.

The ISO 9362 (otherwise known as the BIC code or SWIFT code) made no specifications for formatting transactions, so each party in a transaction needed to come to an agreement regarding transaction types and identification of accounts. There was a lack of consistency with international trade and resulting confusion.

Then, in 1997, the International Organization for Standardization (ISO) published the ISO 13616:1997 proposal, which was so flexible that it was deemed unworkable by many. They cut the proposal down then, stating that each IBAN must be a fixed length and must only include upper case letters. After much backlash, the ISO withdrew the proposal and created a new one, ISO 13616:2003. This proposal – created in 2003 – was updated again in 2007 and was basically split into two parts – SWIFT and IBAN.

SWIFT System

ISO 13616-2:2007 is officially known as SWIFT (Society for Worldwide Interbank Financial Telecommunication), a network that allows financial institutions around the world to both send and receive financial transaction information securely in a standardized (and therefore reliable) way. SWIFT is not responsible for assistance in making transactions. Instead, it sends payment orders that must be analyzed and settled between the involved accounts. In order to utilize SWIFT, all transactions must be between banks or entities closely associated with banks.

Importance of the IBAN System

The IBAN system provides a flexible yet standardized format that is used to identify accounts, validate transaction data, and create a filter that catches data errors. Routing information is always included; it allows one bank (or financial institution) to send a payment to another. Key information about each bank account is also included, as mentioned above. (The information includes branch codes, country codes, as well as check digits, which are designed to spot errors or completely validate an account number.)

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Checking Accounts vs Savings AccountsChecking Accounts vs Savings AccountsA bank client can choose to open checking accounts vs savings accounts depending on several factors, such as purpose, ease of access, or other attributes. A checking account is a type of bank account that is used for everyday transactions. It is the most basic account that banks, credit unions, and small lenders offer.

- Online Payment CompaniesOnline Payment CompaniesOnline payment companies are responsible for handling online or internet-based methods of payment. Examples include PayPal, Alipay, and Google Pay.

- Retail Bank TypesRetail Bank TypesBroadly speaking, there are three main retail bank types. They are commercial banks, credit unions, and certain investment funds that offer retail banking services. All three work toward providing similar banking services. These include checking accounts, savings accounts, mortgages, debit cards, credit cards, and personal loans.

- Wire TransferWire TransferWire transfer is the electronic transfer of funds between people or entities. It allows people in distant locations around the globe to safely transfer

-

Benefits of a Bank Account: Security, Convenience & Financial Growth

In lieu of hoarding money in your home -- whether its dropping loose change in a piggybank or hiding bricks of cash behind drop ceilings -- placing your money a bank account may be a preferable option

-

Understanding Bank Identification Numbers (BINs): What They Are & Why They Matter

A bank identification number (BIN) represents the first four to six digits on a credit card. The first four to six digits identify the financial institution that issued the card. The BIN is a security

finance

- Account Number Verification: How It Works & Why It's Important

- International Money Transfer: Understanding IBANs & How to Use Them

- Understanding Bank Account Roll Numbers: What You Need to Know

- Understanding Account Numbers: Your Key to Financial Records

- Understanding Bank Overdrafts: Causes, Costs & Solutions

- BIS: Understanding the Bank for International Settlements - Role & Impact

- Understanding Bank Statements: A Comprehensive Guide

- Nostro Accounts Explained: A Comprehensive Guide

- Understanding Vostro Accounts: Correspondent Banking Explained

-

Checking Account Overdraft Limits: What You Need to Know

There are no federal laws that limit the amount an account holder can overdraw a checking account. Additionally, there are no restrictions on the overall amount of fees a bank can levy on an overdrawn...

-

Routing Number Explained: What It Is & How to Find It

Of all the passwords, authentication codes, logon numbers, and PINs you have to remember, its likely your bank or credit unions routing number might slip from your memory from time to time. (Or, more ...