Principal Payments Explained: Understanding Loan Repayment

A principal payment is a payment toward the original amount of a loan that is owed. In other words, a principal payment is a payment made on a loanBullet LoanA bullet loan is a type of loan in which the principal that is borrowed is paid back at the end of the loan term. In some cases, the interest expense is that reduces the remaining loan amount due, rather than applying to the payment of interest charged on the loan. In accountingFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will and finance, a principal payment applies to any payment that reduces the amount due on a loan.

Bond Principals are further analyzed on CFI’s Fixed Income Fundamentals Course.

The Basics of a Loan

Understanding the components of a loan is very important. Every loan comprises two components – the principal and the interestInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also. The principal is the amount borrowed, while the interest is the fee paid to borrow the money.

Consider an individual who saved $400,000 to pay for a $1,000,000 home. They would need to borrow $600,000 from the bank to complete the transaction. The $600,000 is the principal amount – the money borrowed. A bank may require 5% annual interest on the principal amount – the fee paid to borrow the money.

The individual in the situation above would need to make an annual total payment that consists of both principal and interest payments. The principal payment goes to reducing the outstanding principal amount due, while the interest payment goes to paying the fee to borrow the money.

There are generally two types of loan repayment schedulesDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows:

- Even principal payments

- Even total payments

Even Principal Payments

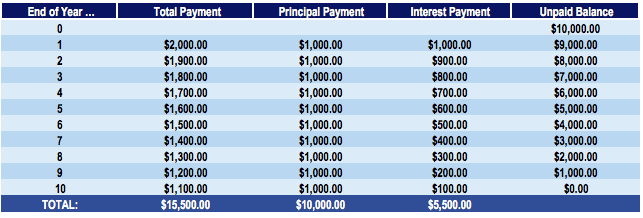

In an even principal payment loan, the principal payment amount is the same every period. Consider John, who takes a $10,000 loan with a 10% annual interest over 10 annual payments. The loan repayment schedule would look as follows:

In the loan repayment schedule above, the loan amortizes over 10 years with even principal payments of $1,000. In 10 years, the unpaid balance is $0.

The principal payment each year goes to reducing the unpaid balance. Since this amount each year is $1,000, the unpaid balance is reduced by $1,000 yearly. The interest payment is calculated on the unpaid balance. For example, the end of year one interest payment would be $10,000 x 10% = $1,000. Note that while the payment of principal remains the same, the total payment due each year, including interest, changes.

Even Total Payments

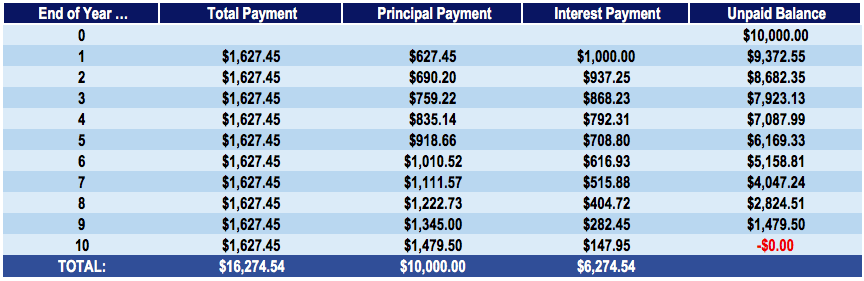

In an even total payment loan, the total payment amount is the same every period. Consider John, who takes a $10,000 loan with a 10% annual interest over 10 annual payments. The loan repayment schedule would look as follows:

In the loan repayment schedule above, the loan amortizes over 10 years with even total payments of $1,627.45. In 10 years, the unpaid balance is $0.

As opposed to an even principal payment schedule, the amount paid to principal here increases yearly. This is due to much of the initial total payment going toward paying interest rather than principal. In the first year, the amount of interest would be $10,000 x 10% = $1,000. With a total payment of $1627.45, the unpaid principal balance is only reduced by $1627.45 – $1,000 = $627.45. In such a schedule, interest payments decrease and payments on the principal increase over time.

Even Principal Payments vs. Even Total Payments

Over the amortization of the loan, the total of payments in an even principal payment schedule is $15,500 while the total payment in an even total payment schedule is $16,274.54. This indicates that by repaying a higher principal amount each year, an individual saves money over the amortization of the loan.

A higher principal payment on a loan reduces the amount of interest owed and, in turn, reduces the total amount paid over the life of the loan. Therefore, principal payments play a significant role in the amount an individual must pay over the lifetime of a loan.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Effective Annual Interest RateEffective Annual Interest RateThe Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective

- Loan CovenantLoan CovenantA loan covenant is an agreement stipulating the terms and conditions of loan policies between a borrower and a lender. The agreement gives lenders leeway in providing loan repayments while still protecting their lending position. Similarly, due to the transparency of the regulations, borrowers get clear expectations of

- PrepaymentPrepaymentA Prepayment is any payment that is made before its official due date. Prepayments may be made for goods and services or towards the settlement of debt. They can be categorized into two groups: Complete Prepayments and Partial Prepayments.

- Simple InterestSimple InterestSimple interest formula, definition and example. Simple interest is a calculation of interest that doesn't take into account the effect of compounding. In many cases, interest compounds with each designated period of a loan, but in the case of simple interest, it does not. The calculation of simple interest is equal to the principal amount multiplied by the interest rate, multiplied by the number of periods.

-

Calculate Your Loan Principal Repayment: A Simple Guide

Each payment you make on a loan goes partly to interest and partly to principal. Calculating how much of your payment goes to principal requires you to know how many payments you make per year, the in

-

Understanding 'Paid in Arrears': Definition & Examples

While the term, "paid in arrears" might sound as though you're late on a payment, that typically isn't the case. Some payments are paid or due in arrears -- after the employee has wo

finance

- Principal Curtailment: Definition, Benefits & Tax Implications

- Advance Payment Explained: Definition, Purpose & Structure

- Understanding Arrears: Definition, Causes & Management

- Automatic Bill Payment: A Comprehensive Guide

- Understanding Continuously Compounded Interest & Key Financial Ratios

- Understanding Down Payments: A Comprehensive Guide

- Online Payment Companies: A Comprehensive Guide

- Stop Payment Orders: Definition, Process & How to Request

- Single Payment Loans: Definition, How They Work & Key Features

-

Understanding Regulation Z: Your Rights as a Borrower

Understanding Regulation Z: Your Rights as a BorrowerRegulation Z is a consumer-protection regulation that compels lenders to disclose the cost of credit in a clear way for consumers. Whether you’re applying for a mortgage or dealing...

-

Annuities Explained: A Simple Guide to Retirement Income

So you're wondering what is an annuity? There are dozens of different flavours of annuities that perform different functions and pay their holders out in different ways, but for our purposes let’...