Understanding Property & Casualty (P&C) Insurance: A Comprehensive Guide

Property and casualty (P&C) insurers are companies that provide coverage on assetsTangible AssetsTangible assets are assets with a physical form and that hold value. Examples include property, plant, and equipment. Tangible assets are (e.g., house, car, etc.) and also liability insurance for accidents, injuries, and damage to other people or their belongings.

Summary

- Property and casualty (P&C) insurers are companies that provide coverage on assets, as well as liability insurance for accidents, injuries, and damage to others or their belongings.

- P&C insurers cover a number of things, including auto insurance, home insurance, marine insurance, and professional liability insurance.

- Customers pay P&C insurers an insurance premium for their desired coverage.

Coverage for Property and Casualty Insurers

Outlined in the Canadian Institute of Actuaries, property and casualty insurers focus on risks that result in losses to property and possessions. Examples include:

- Auto insurance: Covering losses to individuals and properties arising from auto accidents and other unforeseen auto events.

- Home insurance: Covering losses to residences and property arising from extreme weather, fire, theft, or other incidents. In addition, covering liability to third parties from actions by the insured.

- Marine insurance: Covering losses to shipping vehicles.

- Professional liability insurance: Covering losses to professional clients arising from negligence.

Scenarios That Property and Casualty Insurers Cover

The following are several scenarios in which property and casualty insurance provide coverage:

1. A visitor fractures their leg on your property due to your negligence

Josh, an insured individual, forgets to shovel his front yard after a snowy day and causes a stranger to fall and fracture their leg. The property and casualty insurer can help John cover the medical costsHMO vs PPO: Which is Better?Getting the best healthcare often requires choosing between an HMO vs PPO. You need to be able to make an informed decision on which plan will work best. related to the stranger, as well as damages for pain and suffering.

2. Property is vandalized and damaged

Tim, an insured individual, comes home to find his property vandalized. The property and casualty insurer can help Tim cover the cost related to repairing the damage done to the property.

3. Property is damaged from extreme weather

Dan, an insured individual, lives in Florida, and his property was damaged due to a hurricane recently. The property and casualty insurer can help Dan cover the costs related to damage to the property.

How Does Property and Casualty Insurance Work?

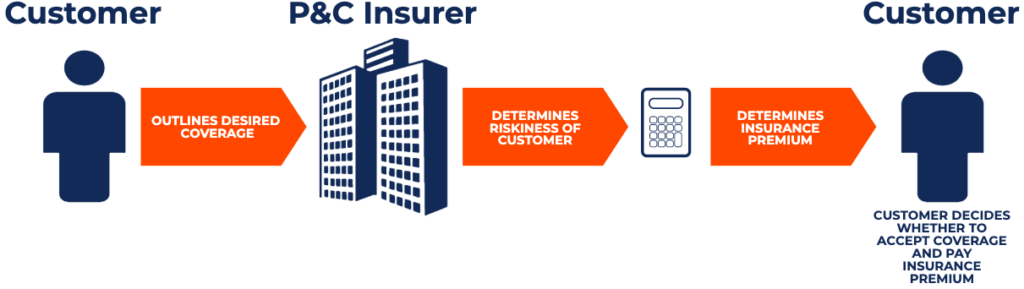

Property and casualty insurers offer insurance to customers for risks, up to a certain coverage amount, in exchange for insurance premiums. Insurance premiums are cash outflows made by the customer in exchange for insurance coverage.

Similar to other insurers, when property and casualty insurers offer coverage to a customer, they must determine an insurance premium the customer will pay by looking at the riskinessSystematic RiskSystematic risk is that part of the total risk that is caused by factors beyond the control of a specific company or individual. Systematic risk is caused by factors that are external to the organization. All investments or securities are subject to systematic risk and therefore, it is a non-diversifiable risk. of the customer. An insurer would commonly look at the likelihood of the customer making a claim and the potential amount of the claim when calculating the amount of insurance premium they should charge. A diagram is provided below to outline the process:

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Commercial Insurance BrokerCommercial Insurance BrokerA commercial insurance broker is an individual tasked with acting as an intermediary between insurance providers and customers.

- IndemnityIndemnityIndemnity is used to protect an individual or entity from potential losses and damages that may result from negligence, legal claims, or other unavoidable

- Insurance DeductibleInsurance DeductibleInsurance deductible pertains to the amount of money on an insurance claim that you would pay before the coverage kicks in and the insurer pays. In other

- Reinsurance CompaniesReinsurance CompaniesReinsurance companies, also known as reinsurers, are companies that provide insurance to insurance companies. In other words, reinsurance companies are companies that receive insurance liabilities from insurance companies.

-

Rental Property Supplies: What's Tax-Deductible?

Materials for roof repairs are generally classifed as rental property supplies. A wide range of items are classified as rental property supplies, which allow you to efficiently manage your in

-

Property Insurance Settlements & Taxes: What You Need to Know

Claimants, both individuals and businesses, may wonder how their insurance settlements will impact their tax liabilities. You may want to consult a tax professional to determine the implications of yo

finance

- Understanding Property & Casualty Insurance Rate Calculation

- Understanding Life & Health Insurance: A Comprehensive Guide

- Understanding Reinsurance: Protecting the Insurance Industry

- Property, Plant & Equipment (PP&E): Definition & Financial Significance

- Title Insurance: Protection & Coverage Explained

- Inland Marine Insurance: Protecting Your Goods During Transit

- Find the Right Property & Casualty Insurance Agent | Protect Your Assets

- Understanding Your Property & Casualty Insurance Policy: A Comprehensive Guide

- SR-22 Insurance: What It Is & Who Needs It - [Year]

-

Life Insurance Medical Exams: Understanding the Process & Preparing

Life Insurance Medical Exams: Understanding the Process & PreparingA few years ago, I bought my very first term life insurance policy. As part of the approval process, I was asked to submit to a medical exam. Even though I am fairly young and in great h...

-

SEP IRA: Employer-Sponsored Retirement Plan Explained & Contribution Limits

SEP IRA: Employer-Sponsored Retirement Plan Explained & Contribution LimitsWhat is a SEP IRA? A SEP IRA stands for a simplified employee pension individual retirement arrangement. It is a type of employer-sponsored retirement plan that can be set ...