Understanding Reinsurance: Protecting the Insurance Industry

Reinsurance companies, also known as reinsurers, are companies that provide insurance to insurance companies. In other words, reinsurance companies are companies that receive insurance liabilities from insurance companies.

It is important to realize that, similar to any other businesses, insurance companies require protection against riskSystematic RiskSystematic risk is that part of the total risk that is caused by factors beyond the control of a specific company or individual. Systematic risk is caused by factors that are external to the organization. All investments or securities are subject to systematic risk and therefore, it is a non-diversifiable risk.. Insurance companies manage their risk through a reinsurance company.

Quick Summary:

- Reinsurance companies, or reinsurers, are companies that provide insurance to insurance companies.

- Reinsurers play a major role for insurance companies as they allow the latter to help transfer risk, reduce capital requirements, and lower claimant payouts.

- Reinsurers generate revenue by identifying and accepting policies that they believe are less risky and reinvesting the insurance premiums they receive.

Understanding Reinsurance Companies

Recall that reinsurance companies provide insurance to insurance companies. How exactly does it work?

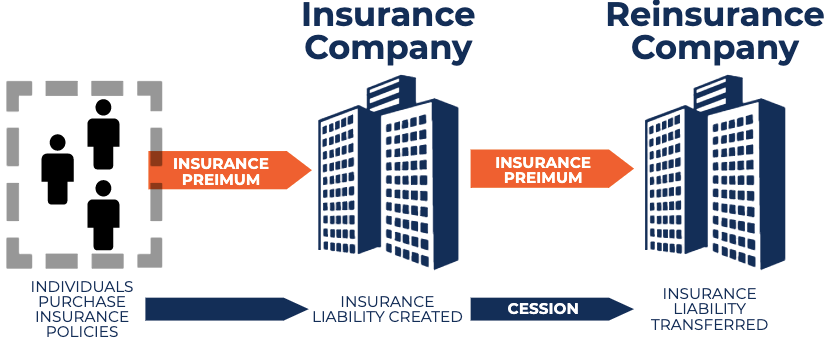

A primary insurer (the insurance company) transfers policies (insurance liabilities) to a reinsurer (the reinsurance company) through a process called cession. Cession simply refers to the portion of the insurance liabilities transferred to a reinsurer.

Similar to the way individuals pay insurance premiumsInsurance ExpenseInsurance expense is the amount that a company pays to get an insurance contract and any additional premium payments. to insurance companies, insurance companies pay insurance premiums to reinsurers for the transfer of insurance liabilities. The diagram below depicts such a relationship.

Roles of Reinsurance Companies

Reinsurance companies are used by insurance companies to:

1. Transfer risk

Insurance companies can issue policies with higher limits due to some of the risk being offset to the reinsurer.

2. Smooth income

The income of insurance companies can be more predictable by transferring highly risky insurance liabilities to reinsurers to absorb potentially large losses.

3. Keep less capital at hand

By offsetting the risk of loss in insurance liabilities, insurance companies do not need to keep as much capitalCapitalCapital is anything that increases one’s ability to generate value. It can be used to increase value across a wide range of categories, such as financial, social, physical, intellectual, etc. In business and economics, the two most common types of capital are financial and human. on hand to cover potential losses. Thus, they can invest the capital elsewhere to increase their revenues.

4. Underwrite more policies

Reinsurance enables insurance companies to underwrite more policies, due to a portion of their liabilities being transferred to reinsurers. This enables insurance companies to take on more risk.

5. Lower claimant payout during natural disasters

Natural disasters such as earthquakes and hurricanes can cause claims to be abnormally high. In such cases, an insurance company can potentially go bankrupt by having to issue out payments to all the claimants. By shifting part of the insurance liabilities to reinsurers, insurance companies are able to remain afloat in such extreme events.

6. Realize arbitrage opportunities

Insurance companies can potentially purchase reinsurance coverage from reinsurers at a rate lower than what they charge their clients. Reinsurers use their own models to evaluate the riskiness of policies. Therefore, reinsurers may accept a lower insurance premium from the insurance company if they deem it as less risky.

Revenue Generation in Reinsurance Companies

Reinsurance companies generate revenue by reinsuring policies that they believe are less risky than expected.

For example, an insurance company may require a yearly insurance premium payment of $1,000 to insure an individual. A reinsurance company may believe that insuring that individual is not as risky as determined by the original insurance company and, therefore, offer to take that insurance liability from the insurance company at a yearly insurance premium payment of $800. The insurance company would be willing to transfer that insurance liability, as they would net $200 yearly from receiving $1,000 to insure the individual and transferring the policy to the reinsurer for only $800. The reinsurer would accept this, as they believe the risk profile of the policy is not as high as determined by the original insurance company.

Additionally, reinsurance companies generate revenue by investing the insurance premiums that they receive. The reinsurer will only need to liquidate its securities if they need to pay out losses. A company that’s been adopting this practice to perfection is Berkshire Hathaway Reinsurance Group.

Lastly, reinsurers generate revenues from insurance companies offloading some of their insurance liabilities related to natural disasters to lower the potential amount of claimant payouts during such unforeseen events.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Commercial Insurance BrokerCommercial Insurance BrokerA commercial insurance broker is an individual tasked with acting as an intermediary between insurance providers and customers.

- Insurance DeductibleInsurance DeductibleInsurance deductible pertains to the amount of money on an insurance claim that you would pay before the coverage kicks in and the insurer pays. In other

- Mortgage BankMortgage BankA mortgage bank is a bank specializing in mortgage loans. It can be involved in originating or servicing mortgage loans, or both. The banks loan their own capital to borrowers and either collect payments in installments along with a certain rate of interest or sell their loans in the secondary market.

- SubrogationSubrogationSubrogation refers to the practice of substituting one party for another in a legal setting. Essentially, subrogation provides a legal right to a third

-

Specialty Insurance: Understanding Unique Coverage Options

Individuals, businesses and other organizations buy specialty insurance to provide protection against financial losses. This type of insurance coverage goes beyond ordinary policies and often centers

-

Understanding Agency Costs: Protecting Shareholder Interests

Agency costs are internal costs incurred due to the competing interests of shareholders Stockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a companys balance s

finance

- Bancassurance Explained: How Banks and Insurance Partner

- Understanding Life & Health Insurance: A Comprehensive Guide

- Online Payment Companies: A Comprehensive Guide

- Understanding Property & Casualty (P&C) Insurance: A Comprehensive Guide

- Understanding Public Companies: A Comprehensive Guide

- Understanding the S&P Sectors: A Comprehensive Guide

- Understanding Affiliated Companies: Definition & Key Differences

- Understanding Insurance Terms: A Clear Guide for Consumers

- Comprehensive Car Insurance: What It Covers & Why You Need It

-

Stand-Alone Insurance: A Comprehensive Guide for Businesses & Individuals

Stand-Alone Insurance: A Comprehensive Guide for Businesses & IndividualsInsurance, in its many forms, is one of the basic costs associated with running a business and a potentially valuable form of protection for private individuals and families. The first step when shopp...

-

Understanding Insurance Waivers: Liability Release & Coverage Options

Understanding Insurance Waivers: Liability Release & Coverage OptionsA waiver is a legal form or document that releases someone, or some organization, from liability. Insurance waivers usually are offered to, or requested to be signed by, individuals by organizations o...