Currency Swap: Definition, How It Works & Key Benefits

What Is a Currency Swap?

A currency swap, sometimes referred to as a cross-currency swap, involves the exchange of interest—and sometimes of principal—in one currency for the same in another currency. Interest payments are exchanged at fixed dates through the life of the contract. It is considered to be a foreign exchange transaction and is not required by law to be shown on a company's balance sheet.

Key Takeaways

- A currency swap involves the exchange of interest—and sometimes of principal—in one currency for the same in another currency.

- Companies doing business abroad often use currency swaps to get more favorable loan rates in the local currency than if they borrowed money from a local bank.

- Considered to be a foreign exchange transaction, currency swaps are not required by law to be shown on a company's balance sheet.

- Interest rate variations for currency swaps include fixed rate to fixed rate, floating rate to floating rate, or fixed rate to floating rate.

The Basics of Currency Swaps

Currency swaps were originally done to get around exchange controls, governmental limitations on the purchase and/or sale of currencies. Although nations with weak and/or developing economies generally use foreign exchange controls to limit speculation against their currencies, most developed economies have eliminated controls nowadays.

So swaps are now done most commonly to hedge long-term investments and to change the interest rate exposure of the two parties. Companies doing business abroad often use currency swaps to get more favorable loan rates in the local currency than they could if they borrowed money from a bank in that country.

Currency swaps are important financial instruments used by banks, investors, and multinational corporations.

How a Currency Swap Works

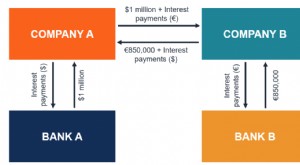

In a currency swap, the parties agree in advance whether or not they will exchange the principal amounts of the two currencies at the beginning of the transaction. The two principal amounts create an implied exchange rate. For example, if a swap involves exchanging €10 million versus $12.5 million, that creates an implied EUR/USD exchange rate of 1.25. At maturity, the same two principal amounts must be exchanged, which creates exchange rate risk as the market may have moved far from 1.25 in the intervening years.

Pricing is usually expressed as London Interbank Offered Rate (LIBOR), plus or minus a certain number of points, based on interest rate curves at inception and the credit risk of the two parties.

Due to recent scandals and questions around its validity as a benchmark rate, LIBOR is being phased out. According to the Federal Reserve and regulators in the UK, LIBOR will be phased out by June 30, 2023, and will be replaced by the Secured Overnight Financing Rate (SOFR). As part of this phase-out, LIBOR one-week and two-month USD LIBOR rates will no longer be published after December 31, 2021.

A currency swap can be done in several ways. Many swaps use simply notional principal amounts, which means that the principal amounts are used to calculate the interest due and payable each period but is not exchanged.

If there is a full exchange of principal when the deal is initiated, the exchange is reversed at the maturity date. Currency swap maturities are negotiable for at least 10 years, making them a very flexible method of foreign exchange. Interest rates can be fixed or floating.

India and Japan signed a bilateral currency swap agreement worth $75 billion in October 2018 to bring stability to forex and capital markets in India.

Exchange of Interest Rates in Currency Swaps

There are three variations on the exchange of interest rates: fixed rate to fixed rate; floating rate to floating rate; or fixed rate to floating rate. This means that in a swap between euros and dollars, a party that has an initial obligation to pay a fixed interest rate on a euro loan can exchange that for a fixed interest rate in dollars or for a floating rate in dollars. Alternatively, a party whose euro loan is at a floating interest rate can exchange that for either a floating or a fixed rate in dollars. A swap of two floating rates is sometimes called a basis swap.

Interest rate payments are usually calculated quarterly and exchanged semi-annually, although swaps can be structured as needed. Interest payments are generally not netted because they are in different currencies.

-

Currency Swap Contracts: Definition & How They Work

A currency swap contract (also known as a cross-currency swap contract) is a derivative contract between two parties that involves the exchange of interest payments, as well as the exchange of princip

-

Swap Rate Explained: Understanding Fixed Exchange Rates in Derivatives

The swap rate is the fixed rate of a swapSwapA swap is a derivative contract between two parties that involves the exchange of pre-agreed cash flows of two financial instruments. The cash flows a

Foreign exchange transactions

- Understanding Prevailing Interest Rates: Definition & Current Rates

- Understanding Tiered Interest Rates: A Comprehensive Guide

- Understanding Foreign Currency: A Comprehensive Guide

- Cross-Currency Swaps: Definition, How They Work & Applications

- Plain Vanilla Swaps: Definition, Types & How They Work

- Currency Swap vs. Interest Rate Swap: Key Differences Explained

- Arrears Swap Explained: Interest Rate Swap with Retroactive Payments

- Delayed Rate Setting Swaps: Definition & How They Work

- Interest Rate Options: Definition & How They Work

-

Interest Rate Swap Valuation: A Comprehensive Guide

Interest Rate Swap Valuation: A Comprehensive GuideInterest rate swaps amount to exchange cash flows, with one flow based on variable payments and the other on fixed payments. To understand whether a swap is a good deal, investors need to figure the p...

-

BBSW: Understanding the Bank Bill Swap Rate in Australia

BBSW: Understanding the Bank Bill Swap Rate in AustraliaWhat Is the Bank Bill Swap Rate (BBSW)? The Bank Bill Swap Rate (BBSW), or Bank Bill Swap Reference Rate, is a short-term interest rate used as a benchmark for the pricing of Australian do...