Currency Swap Contracts: Definition & How They Work

A currency swap contract (also known as a cross-currency swap contract) is a derivative contract between two parties that involves the exchange of interest payments, as well as the exchange of principal amountsPrincipal PaymentA principal payment is a payment toward the original amount of a loan that is owed. In other words, a principal payment is a payment made on a loan that reduces the remaining loan amount due, rather than applying to the payment of interest charged on the loan. in certain cases, that are denominated in different currencies. Although currency swap contracts generally imply the exchange of principal amounts, some swaps may require only the transfer of the interest payments.

Breaking Down Currency Swap Contracts

A currency swap consists of two streams (legs) of fixed or floating interest payments denominated in two currencies. The transfer of interest payments occurs on predetermined dates. In addition, if the swap counterparties previously agreed to exchange principal amounts, those amounts must also be exchanged on the maturity date at the same exchange rateFixed vs. Pegged Exchange RatesForeign currency exchange rates measure one currency's strength relative to another. The strength of a currency depends on a number of factors such as its inflation rate, prevailing interest rates in its home country, or the stability of the government, to name a few..

Currency swaps are primarily used to hedge potential risks associated with fluctuations in currency exchange rates or to obtain lower interest rates on loans in a foreign currency. The swaps are commonly used by companies that operate in different countries. For example, if a company is conducting business abroad, it would often use currency swaps to retrieve more favorable loan rates in their local currency, as opposed to borrowing money from a foreign bank.

For example, a company may take a loan in the domestic currency and enter a swap contract with a foreign company to obtain a more favorable interest rateInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. on the foreign currency that is otherwise is unavailable.

How Do Currency Swap Contracts Work?

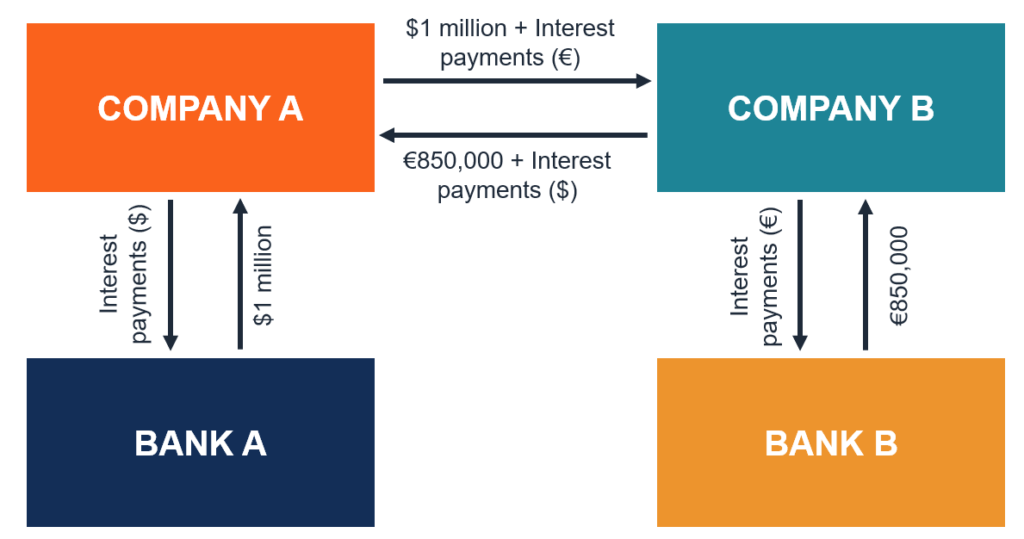

In order to understand the mechanism behind currency swap contracts, let’s consider the following example. Company A is a US-based company that is planning to expand its operations in Europe. Company A requires €850,000 to finance its European expansion.

On the other hand, Company B is a German company that operates in the United States. Company B wants to acquire a company in the United States to diversify its business. The acquisition deal requires US$1 million in financing.

Neither Company A nor Company B holds enough cash to finance their respective projects. Thus, both companies will seek to obtain the necessary funds through debt financingDebt vs Equity FinancingDebt vs Equity Financing - which is best for your business and why? The simple answer is that it depends. The equity versus debt decision relies on a large number of factors such as the current economic climate, the business' existing capital structure, and the business' life cycle stage, to name a few.. Company A and Company B will prefer to borrow in their domestic currencies (that can be borrowed at a lower interest rate) and then enter into the currency swap agreement with each other.

The currency swap between Company A and Company B can be designed in the following manner. Company A obtains a credit line of $1 million from Bank A with a fixed interest rate of 3.5%. At the same time, Company B borrows €850,000 from Bank B with the floating interest rate of 6-month LIBORLIBORLIBOR, which is an acronym of London Interbank Offer Rate, refers to the interest rate that UK banks charge other financial institutions for. The companies decide to create a swap agreement with each other.

According to the agreement, Company A and Company B must exchange the principal amounts ($1 million and €850,000) at the beginning of the transaction. In addition, the parties must exchange the interest payments semi-annually.

Company A must pay Company B the floating rate interest payments denominated in euros, while Company B will pay Company A the fixed interest rate payments in US dollars. On the maturity date, the companies will exchange back the principal amounts at the same rate ($1 = €0.85).

Types of Currency Swap Contracts

Similar to interest rate swaps, currency swaps can be classified based on the types of legs involved in the contract. The most commonly encountered types of currency swaps include the following:

- Fixed vs. Float: One leg of the currency swap represents a stream of fixed interest rate payments while another leg is a stream of floating interest rate payments.

- Float vs. Float (Basis Swap): The float vs. float swap is commonly referred to as basis swap. In a basis swap, both swaps’ legs both represent floating interest rate payments.

- Fixed vs. Fixed: Both streams of currency swap contracts involve fixed interest rate payments.

For example, when conducting a currency swap between USD to CAD, a party that decides to pay a fixed interest rate on a CAD loan can exchange that for a fixed or floating interest rate in USD. Another example would be concerning the floating rate. If a party wishes to exchange a floating rate on a CAD loan, they would be able to trade it for a floating or fixed rate in USD as well.

The interest rate payments are calculated on a quarterly or semi-annually basis.

How a Currency Swap is Priced

Pricing is expressed as a value based on LIBOR +/- spread, which is based on the credit risk between the exchanging parties. LIBOR is considered a benchmark interest rate that major global banks lend to each other in the interbank market for short-term borrowings. The spread stems from the credit risk, which is a premium that is based on the likelihood that the party is capable of paying back the debt that they had borrowed with interest.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Interest Rate SwapInterest Rate SwapAn interest rate swap is a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another

- Credit RiskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally,

- Floating Interest RateFloating Interest RateA floating interest rate refers to a variable interest rate that changes over the duration of the debt obligation. It is the opposite of a fixed rate.

- International Fisher Effect (IFE)International Fisher Effect (IFE)The International Fisher Effect (IFE) states that the difference between the nominal interest rates in two countries is directly proportional

-

Understanding Acquisition Cost: Definitions & Applications

Acquisition cost is the cost of purchasing an asset. It is generally used in three different contexts in business, which include the following:Mergers and acquisitionsFixed assetsCustomer acquisition&

-

Advertising Budget: Definition, Planning & Best Practices

An advertising budget is a company’s allocation of promotional expenditures over a specified time period. It is a measure of a company’s planned expenditure on accomplishing marketing obje

finance

- Acquirer Definition: Understanding Corporate Acquisitions

- Understanding Clawbacks: Protecting Stakeholders from Failed Performance

- Commodity Swaps: Definition, Uses & Hedging Strategies

- Debt/Equity Swap: Understanding Financial Restructuring

- Equity Swap Contracts: Definition, Mechanics & Applications

- Cross Currency Swaps: Definition, Mechanics & Benefits

- Non-Deliverable Swaps (NDS): Definition, Function & How They Work

- Quanto Swap Explained: A Comprehensive Guide for Investors

- Volatility Swaps: A Comprehensive Guide for Investors

-

Understanding the Backing of the U.S. Dollar: History & Current System

Understanding the Backing of the U.S. Dollar: History & Current SystemA detail of the U.S. one-dollar bill. To improve the public's confidence in the U.S. dollar and encourage its use in financial transactions, the Federal Reserve used to hold a specific am...

-

Understanding Stocks: A Beginner's Guide to Share Ownership

Understanding Stocks: A Beginner's Guide to Share OwnershipWhen a person owns stock in a company, the individual is called a shareholder and is eligible to claim part of the company’s residual assets and earnings (should the company ever have to dissolv...