Credit Valuation Adjustment (CVA): Understanding Counterparty Risk

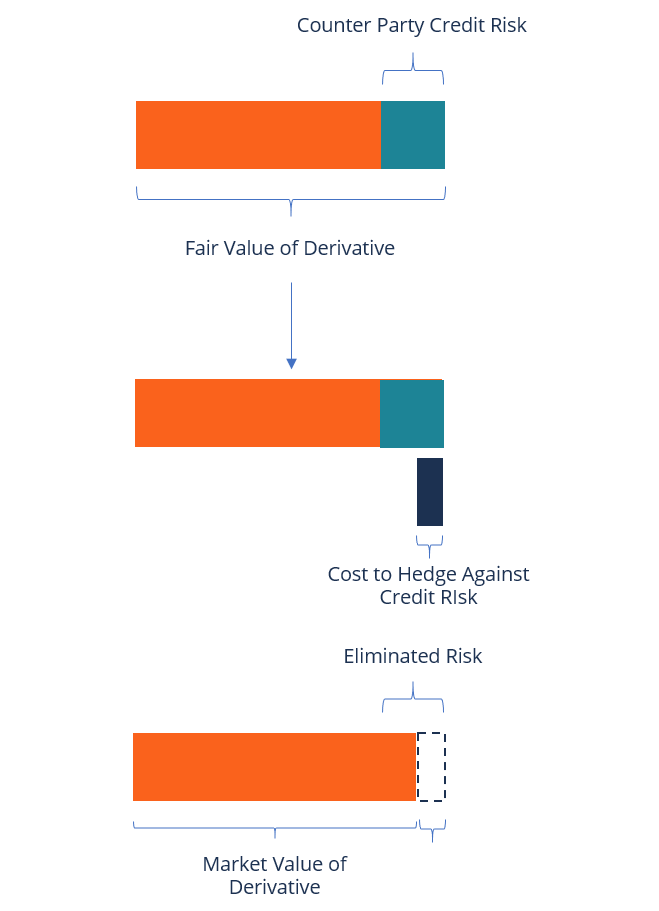

Credit Valuation Adjustment (CVA) is the price that an investor would pay to hedge the counterparty credit risk of a derivative instrumentDerivativesDerivatives are financial contracts whose value is linked to the value of an underlying asset. They are complex financial instruments that are. It reduces the mark to market value of an asset by the value of the CVA.

Credit Valuation Adjustment was introduced as a new requirement for fair value accounting during the 2007/08 Global Financial Crisis. Since its introduction, it has attracted dozens of derivatives market participants, and most of them have incorporated CVA in deal pricing.

Formula for Calculating Credit Valuation Adjustment

The formula for calculating CVA is written as follows:

Where:

- T = Maturity period of the longest transaction

- Bt = Future value of one unit of the base currency invested at the current interest rate at T maturity

- R = Fraction of the portfolio value that can be removed in case of default

- T = Time of default

- dPD(0,t)= Risk-neutral probability of counterparty default (between times s and t)

- E(t) = Exposure at time T

History of Credit Valuation Adjustment

The concept of credit risk management, which includes credit valuation adjustment, was developed due to the increased number of country and corporate defaults and financial falloutsTop Accounting ScandalsThe last two decades saw some of the worst accounting scandals in history. Billions of dollars were lost as a result of these financial disasters. In this. In recent times, there have been cases of sovereign entity defaults, such as Argentina (2001) and Russia (1998). At the same time, a high number of large companies collapsed before, during, and after the financial crisis of 2007/08, including WorldCom, Lehman Brothers, and Enron.

Initially, research in credit riskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally, focused on the identification of such a risk. Specifically, the focus was on counterparty credit risk, which refers to the risk that a counterparty may default on its financial obligations.

Prior to the 2008 financial crisis, market participants treated large derivative counterparties as too big to fail and, therefore, never considered their counterparty credit risk. The risk was often ignored due to the high credit rating of counterparties and the small size of derivative exposures. The assumption was that the counterparties could not default on their financial obligations like other parties.

However, during the 2008 financial crisis, the market experienced dozens of corporate collapses, including large derivative counterparties. As a result, market participants started incorporating credit valuation adjustment when calculating the value of over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of securities between two counter-parties executed outside of formal exchanges and without the supervision of an exchange regulator. OTC trading is done in over-the-counter markets (a decentralized place with no physical location), through dealer networks. derivative instruments.

Challenges to Counterparty Credit Risk

Derivative instruments can be classified as either unilateral or bilateral, depending on the nature of the payoff.

1. Unilateral derivate instruments

For a unilateral derivative instrument holder, exposure to loss occurs if a counterparty defaults on their financial obligations. The amount of loss that an investor incurs is equal to the fair value of the instrument at the time of default.

2. Bilateral derivative instruments

Bilateral derivatives are more complex than unilateral derivatives, since the former includes two-way counterparty risk. This means that both the counterparty and the investor are exposed to counterparty risk. The advantage of bilateral derivatives is that the derivative may adopt an asset or liability position at any valuation date.

For example, if Counterparty A is at a positive asset position today, it is exposed to Counterparty B. If A defaults on his obligation, he will owe the positive asset to B. The same applies if B is in a negative liability position because, in case of default, he owes the negative liability position to A.

CVA Valuation Methods

There are several methods that are used to value derivatives, and they vary from simple to advanced methodologies. Determining the credit valuation adjustment method to use depends on the organization’s sophistication and resources available to the market participants.

1. Simple approach

The simple method calculates the mark to market value of the instrument. The calculation is then repeated to adjust the discount rates by the counterparty’s credit spread. Calculate the difference between the two resulting values to obtain the credit valuation adjustment.

2. Swaption-type valuation

The swaption-type is a more complex credit valuation adjustment methodology that requires advanced knowledge of derivative valuations and access to specific market data. It uses the counterparty credit spread to estimate the replacement value of the asset.

3. Simulation modeling

This involves the simulation of market risk factors and risk factor scenarios. The derivatives are then revalued using multiple simulation scenarios. The expected exposure profile of each counterparty is determined by aggregating the resulting matrix. Each counterparty’s expected exposure profile is adjusted to derive the collateralized expected exposure profile.

More Resources

We hope you’ve enjoyed CFI’s explanation of a credit valuation adjustment. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Basis RiskBasis RiskBasis risk is the risk that the futures price might not move in normal, steady correlation with the price of the underlying asset, so as to negate the effectiveness of a hedging strategy in minimizing a trader's exposure to potential loss. Basis risk is accepted in an attempt to hedge away price risk.

- Credit Default Swap (CDS)Credit Default SwapA credit default swap (CDS) is a type of credit derivative that provides the buyer with protection against default and other risks. The buyer of a CDS makes periodic payments to the seller until the credit maturity date. In the agreement, the seller commits that, if the debt issuer defaults, the seller will pay the buyer all premiums and interest

- Hedging ArrangementHedging ArrangementHedging arrangement refers to an investment whose aim is to reduce the level of future risks in the event of an adverse price movement of an asset. Hedging provides a sort of insurance cover to protect against losses from an investment.

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

-

Understanding Credit Card BINs & IINs: Issuer Identification Explained

A BIN tells you what institution issued a credit card. On a credit card, BIN is the Bank Identification Number. The BIN is embedded within the credit card number and tells which financial ins

-

Understanding A1 Credit Ratings: A Guide to Financial Strength

The term A-1 or A1 credit is a rating of financial strength of companies and other entities issuing bonds and other forms of debt. The exact meaning of the term varies, but is a general indication of

invest

- Intraday Credit: Understanding Short-Term Account Overdrafts

- Credit Amnesty: Understanding the Truth & Avoiding Scams

- Understanding B Credit Ratings: What They Mean for Businesses

- Cashback Credit Cards: A Comprehensive Guide

- Commodity Valuation: Understanding Intrinsic Value & Market Pricing

- Understanding the Credit Curve: A Guide for Investors

- Credit Valuation Adjustment (CVA): Understanding Counterparty Risk

- Understanding Probability of Default (PD): A Comprehensive Guide

- Stock Valuation: A Comprehensive Guide for Investors

-

Understanding Credit Card CVN: What It Is & Why It's Important

CVN is an acronym for "card verification number" used to assist merchants with fraud prevention. The credit card CVN is a three-digit number on the back of the credit card for MasterCard and...

-

Understanding R1 & I1 Credit Report Codes: What They Mean

The credit reporting industry sometimes uses what seem like "secret codes" on your report for the status of an account. R1 and I1 are the most critical codes to build your credit score, and ...