The Hot Hand Effect: Understanding Cognitive Bias in Performance

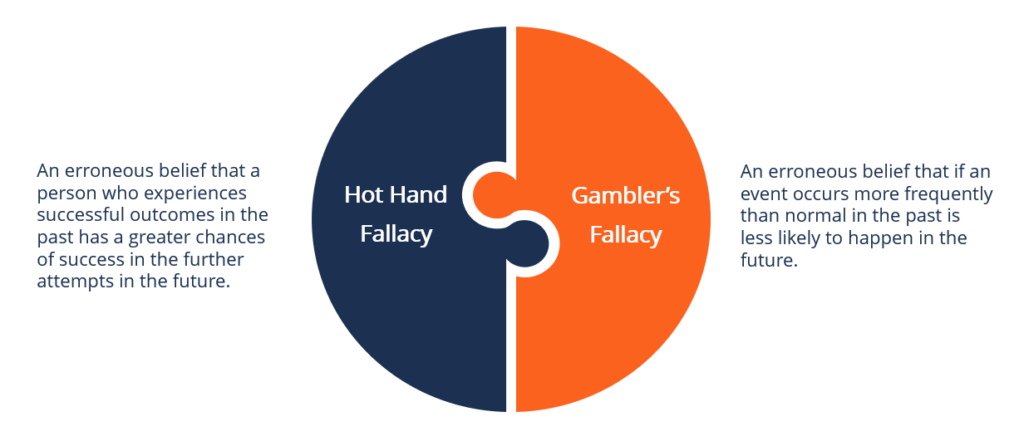

Hot hand is a cognitive social bias where an individual believes that a successful past performance can be used to predict success in future attempts. People who believe in the hot hand phenomenon expect a trend to continue in the future. Such a line of thinking is not true since past results do not change the conditional independence of events occurring in the future.

The hot hand and gambler’s fallacy are two important behavioral biases in financial marketsFinancial MarketsFinancial markets, from the name itself, are a type of marketplace that provides an avenue for the sale and purchase of assets such as bonds, stocks, foreign exchange, and derivatives. Often, they are called by different names, including "Wall Street" and "capital market," but all of them still mean one and the same thing. that affect investment decisions. Hot hand belief is also common in sports, especially in basketball, where it is believed that when a player’s performance during a particular time period is significantly better based on his or her streaks of successful shots. The concept seems to affect the choice of players and the selection of the play.

Summary

- The hot hand belief occurs when an individual erroneously assumes that a recent past results are a good predictor of future outcomes, when the events are independent of each other.

- Investors are susceptible to the hot hand fallacy, and they will buy more funds or hold more diversified portfolios with the expectation of a continuous positive performance record.

- Investment groups are less prone to the hot hand fallacy compared to individual investment decisions.

The Hot Hand Theory Explained

The hot hand fallacy theory was pioneered by Thomas Gilovich, Amos Tversky, and Robert Vallone in their famous “The Hot Hand in Basketball: On the Misperception of Random Sequences” (1985). The study, which investigated people’s intuitive conception of the belief in “hot hand” and “streak shooting,” drew from mathematical psychology, decision-making behaviors and heuristics, and cognitive psychology.

According to the study, outcomes of consecutive basketball shots are independent. The three men looked at the people’s inability to understand randomness and random events and how statistical information judgment triggers the wrong assumption regarding the random events.

Such kinds of thought patterns produced two related biases when applied to a coin toss. The first of the biases is the gambler’s fallacy, which makes an individual assume that a long sequence of either the head or tail increases the probability of getting a head or tail, respectively. Second, it leads to the rejection of randomness due to the belief that a streak of either outcome is non-representative. Economists refer to the hot hand concept as extrapolation bias.

Hot Hand in Investment Decisions

The hot hand belief is at play when investors think of buying and selling in the financial markets. The bias is common among investors who delegate decisions to professional fund managersFamous Fund ManagersThe following article lists some of the fund managers that have been regarded as exceptional. This list includes investors that have created funds or managed very profitable funds. Fund managers included are Peter Lynch, Abigail Johnson, John Templeton, and John Bogle.. With the hot hand phenomenon, investors tend to purchase funds that were successful in the past, believing that the manager will prolong the performance record.

However, given the inconsistencies in fund performance, the hot hand fallacy may lead to a biased decision. Individuals with the fallacy believe that a particular person is hot and not a specific outcome. For example, investors tend to believe that if a professional manager purchased successful funds in the past, then whatever funds they settle on are likely to be profitable in the future.

A similar tendency is also manifest in lottery settings. The tendency of gamblers to redeem lottery tickets for more tickets instead of cash is consistent with the hot hand phenomenon; since individuals who enjoyed successive wins in the past believe that they are more likely to win again.

The hot hand belief emanates from illusion control, where people believe that they or others exert control over randomly determined events. Essentially, the hot hand fallacy surmises that, after a series of wins, investors will increase the number of shares they invest in and, after a loss, decrease them. It is done without factoring in the discounted future values of assets.

Hot Hand Belief in Individuals vs. Investment Groups

Investment groups are less prone to the hot hand fallacy and tend to decide more optimally than individuals in strategic and non-strategic settings. Even so, both groups and individuals alike exhibit hot hand beliefs. Investors who fall prey to such behavioral bias tend to hold less diversified portfolios, which can influence their risk exposure and, consequently, their expected returnsExpected ReturnThe expected return on an investment is the expected value of the probability distribution of possible returns it can provide to investors. The return on the investment is an unknown variable that has different values associated with different probabilities.. The behavioral biases that affect the investment decisions are based on the investment strategy, which differs between individuals and groups.

Investors who join investment groups can overcome their exposure to the hot hand fallacy. Under such an approach, amateur investors combine their investable holdings through a limited liability company or partnership in order to make a decision together and split the profits. Investment groups are different from mutual funds since, in the latter, shareholders hire professional fund managers to exercise rights on their behalf.

Purchasing and selling behaviors are also susceptible to the hot hand fallacy. The behavior can be seen when a customer misinterprets random market events and is influenced that a small sample represents the underlying process. Investors are more likely to purchase stock with positive trends in earnings. In the same manner, consumers are more likely to sell the stock with an adverse earning history.

Additional Resources

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)™Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Decision Analysis (DA)Decision Analysis (DA)Decision analysis is a form of decision-making that involves identifying and assessing all aspects of a decision, and taking actions based on the decision

- Homogeneous ExpectationsHomogeneous ExpectationsHomogeneous expectations is a subjective belief, entrenched in the Modern Portfolio Theory (MPT) proposed by American economist Harry

- Overconfidence BiasOverconfidence BiasOverconfidence bias is a false and misleading assessment of our skills, intellect, or talent. In short, it's an egotistical belief that we're better than we actually are. It can be a dangerous bias and is very prolific in behavioral finance and capital markets.

- Herd MentalityHerd MentalityIn finance, herd mentality bias refers to investors' tendency to follow and copy what other investors are doing. They are largely influenced by emotion and instinct, rather than by their own independent analysis. This guide provides examples of herd bias

-

Anchoring Bias: Understanding How First Impressions Influence Decisions

Anchoring bias occurs when people rely too much on pre-existing information or the first information they find when making decisions. For example, if you first see a T-shirt that costs $1,200 –

-

The Hot Hand Effect: Understanding Cognitive Bias in Performance

Hot hand is a cognitive social bias where an individual believes that a successful past performance can be used to predict success in future attempts. People who believe in the hot hand phenomenon exp

invest

- PC Banking: A Comprehensive Guide to Online Banking Security & Features

- IRA CDs: Secure Retirement Savings with FDIC Insurance

- Understanding Hot IPOs: A Guide to Initial Public Offerings

- Understanding Hot Issues: IPOs with Exceptional Demand

- Understanding Hot Money Investments: Strategies & Capital Gains Yield

- Hot Wallets Explained: Security, Risks & How They Work

- Understanding Days of Inventory on Hand (DOH): A Comprehensive Guide

- Understanding Cryptocurrency: A Beginner's Guide to Digital Currency

- Hot vs. Cold Wallets: Understanding Cryptocurrency Security

-

Annuities Explained: A Simple Guide to Retirement Income

Annuities Explained: A Simple Guide to Retirement IncomeSo you're wondering what is an annuity? There are dozens of different flavours of annuities that perform different functions and pay their holders out in different ways, but for our purposes let’...

-

Weeks on Hand: Definition, Calculation & Importance for Businesses

Weeks on Hand: Definition, Calculation & Importance for BusinessesWeeks on hand refers to the average amount of time it takes a business to sell the inventory it has on hold. For businesses where there is high, recurring demand, this metric can also be measured in d...