Sukuk: Understanding Islamic Bonds and Their Function

Sukuk (Islamic bond or “Sharia-compliant” bond) is an Islamic financial certificate that represents a portion of ownership in a portfolio of eligible existing or future assetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and. They can be considered as an Islamic version of conventional bondsBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period..

Sharia (Islamic law) prohibits lending with interest payments (riba), which is considered usurious and exploitative in nature. Thus, bonds are forbidden in Islamic finance.

Sukuk does not represent a debt obligationCurrent DebtOn a balance sheet, current debt is debts due to be paid within one year (12 months) or less. It is listed as a current liability and part of. Upon its issuance, the issuer sells certificates to investors. Then, the issuer uses the proceeds from the certificates to purchase the asset, and investors receive partial ownership of the asset. The investors are also entitled to part of the profits generated by the asset.

Sukuk vs. Bonds

Sukuk is an alternative to conventional bonds. Islamic and conventional bonds share the following characteristics:

- Investors receive a stream of payments: Conventional bonds provide investors with interest payments, while Sukuk allows investors to receive profit generated by the underlying asset.

- Less risky investments than equity: Sukuk and bonds are considered less risky investments relative to equities.

- Initially sold by the issuers: Both are initially sold by the issuers to the investors. Afterward, both securities are traded over the counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of securities between two counter-parties executed outside of formal exchanges and without the supervision of an exchange regulator. OTC trading is done in over-the-counter markets (a decentralized place with no physical location), through dealer networks..

Despite the similarities, there are few important differences between Islamic and conventional bonds, as summarized in the table below:

Sukuk Bonds OwnershipPartial ownership of the assetDebt obligationComplianceComplies with ShariaComplies with country/region of issuancePricingBased on the value of the underlying assetBased on issuer's creditworthiness

Issuing Process for Sukuk Certificates

The unique nature of Sukuk requires a specific issuing process for the financial instrument. The following steps are common in the issuance process:

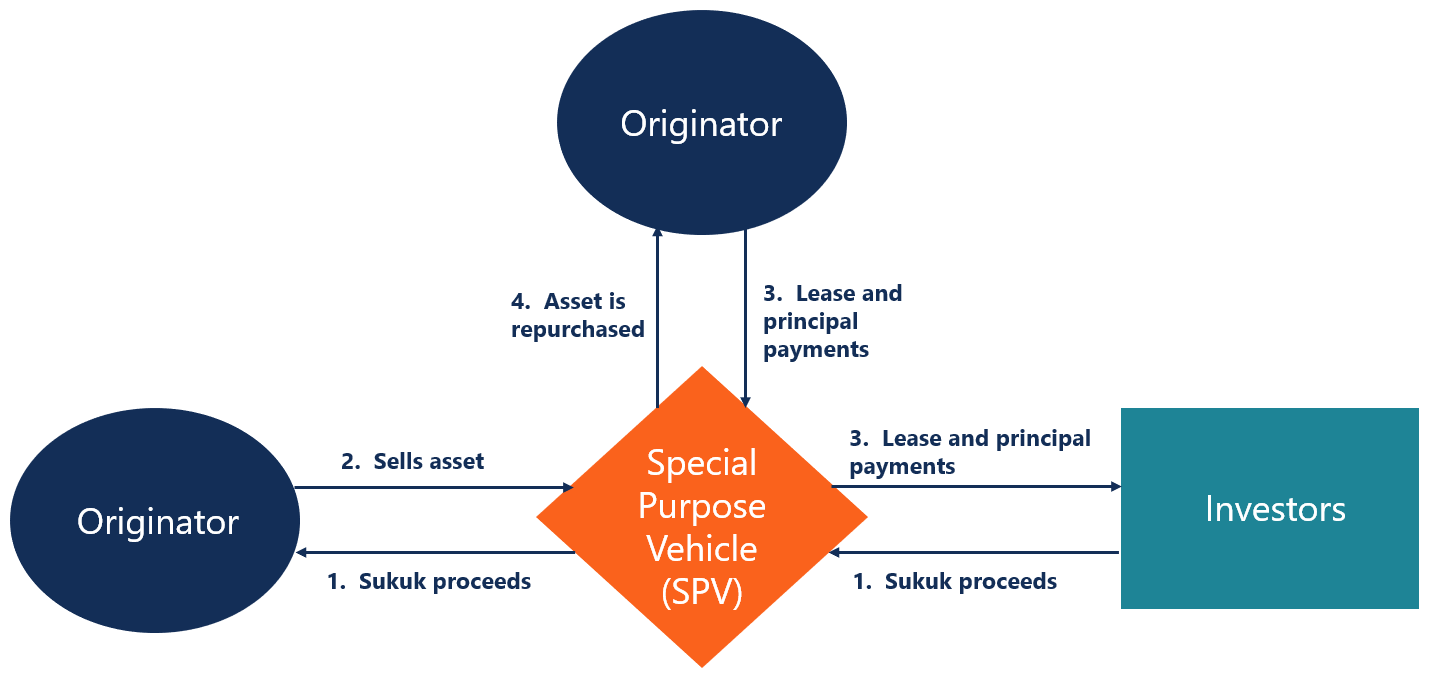

- A company that requires capital (referred to as the “originator”) establishes a special purpose vehicle (SPV)Special Purpose Vehicle (SPV)A Special Purpose Vehicle/Entity (SPV/SPE) is a separate entity created for a specific and narrow objective, and that is held off-balance sheet. SPV is a. The SPV protects the underlying assets from creditors if the originator suffers from financial problems.

- This special purpose vehicle (SPV) issues Sukuk certificates that are sold to the investors.

- Then the originator purchases the required asset, using the proceeds from the sale of the certificates to the investors.

- The SPV buys the asset from the originator.

- SPV pays the asset sale proceeds to the originator.

- The SPV sets up the lease of the asset to the originator. Then the originator makes lease payments to the SPV, which later distributes the payments among the holders as lease income.

- On the termination date of the lease, the originator purchases the asset back from the SPV at its nominal value. The SPV distributes the proceeds to the certificate holders.

Additional Resources

Thank you for reading CFI’s explanation of Sukuk. CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Bond IssuersBond IssuersThere are different types of bond issuers. These bond issuers create bonds to borrow funds from bondholders, to be repaid at maturity.

- Fixed Income GlossaryFixed Income GlossaryThis fixed income glossary covers the most important bond terms and definitions required for financial analysts. These terms are covered in detail in CFI's Fixed Income Fundamentals Course.. Constant Perpetuity, Correlation, Coupon Rate, Covariance, Credit Spread

- Investing: A Beginner’s GuideInvesting: A Beginner's GuideCFI's Investing for Beginners guide will teach you the basics of investing and how to get started. Learn about different strategies and techniques for trading

- Junk BondsBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period.

-

Backtesting: A Comprehensive Guide to Strategy Validation

Backtesting involves applying a strategy or predictive model to historical data to determine its accuracy. It can be used to test and compare the viability of trading strategies so tradersSix Essentia

-

Banker's Acceptance: Definition, Function & Key Features

A banker’s acceptance refers to a financial instrument that represents a promised future payment from a bank. It states the name of the entity to which the funds need to be transferred, along wi

invest

- PC Banking: A Comprehensive Guide to Online Banking Security & Features

- IRA CDs: Secure Retirement Savings with FDIC Insurance

- Understanding the DU: Your Mortgage Approval Explained

- Decentralized Finance (DeFi): A Comprehensive Overview

- Jumbo CDs: Higher Rates & Deposits Explained

- Special Purpose Vehicles (SPVs): Definition, Types & Assets

- Understanding Cryptocurrency: A Beginner's Guide to Digital Currency

- DB(k) Plans: A Hybrid Retirement Solution for Employers & Employees

- Understanding Regulation Z: Your Rights as a Borrower

-

Understanding Loan Lifespan: What is Average Life?

Understanding Loan Lifespan: What is Average Life?Average life is the length of time that each unit of unpaid principal is expected to remain outstanding. The average life of mortgagesMortgageA mortgage is a loan – provided by a mortgage lender...

-

Understanding Average Return: A Simple Guide

Understanding Average Return: A Simple GuideAverage return is the mathematical average of a sequence of returns that have accrued over time. In its simplest terms, average return is the total return over a time period divided by the number of p...