Banker's Acceptance: Definition, Function & Key Features

A banker’s acceptance refers to a financial instrument that represents a promised future payment from a bank. It states the name of the entity to which the funds need to be transferred, along with the amount and date of payment. Banker’s acceptances are short-term instruments that generally come with a maturity between 30 days and 180 days.

Summary

- A banker’s acceptance is a short-term financial instrument that represents a promised future payment from a bank and with a maturity of between 30 and 180 days.

- The application process for a banker’s acceptance is similar to that of a short-term loan and involves various credit and collateral checks.

- Once the bank accepts a banker’s acceptance, the liability immediately transfers from the issuer of the banker’s acceptance to the bank.

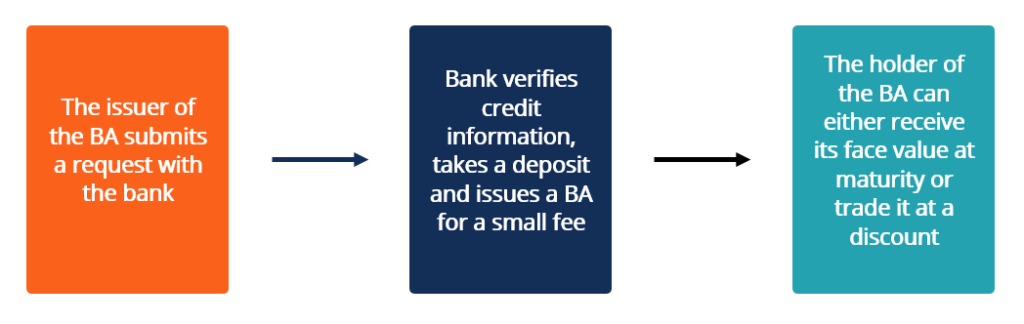

How Does a Banker’s Acceptance Work?

The issuer of a banker’s acceptance deposits the future payment with a bank. The bank charges a small fee and issues a time draft against the deposit, representing a guaranteed future payment by the bank. Upon acceptance from the bank, the liability transfers from the issuer of the banker’s acceptance and becomes an obligation of the bank. As such, the credit rating of a banker’s acceptance is generally the same as that of the bank that promised the payment.

Since banker’s acceptances are short-term instruments, the application process for the securities is similar to that of short-term loansShort-Term DebtShort-term debt is defined as debt obligations that are due to be paid either within the next 12-month period or the current fiscal year.. The bank will assess the creditworthiness of the borrower using its internally set criteria to ensure that the borrower holds sufficient funds to cover the deposit for the future payment. Depending on the size of the banker’s acceptance, the borrower may or may or not need to provide collateral. The bank charges the borrower a small percentage on the amount.

Banker’s Acceptance vs. Time Drafts

A banker’s acceptance essentially serves the same purpose as time drafts and postdated checks. The key difference is that a banker’s acceptance can be traded in the secondary market before maturity and is thus seen as an investment tool.

Another difference is the way the instruments are used. Unlike time drafts, banker’s acceptances are frequently used in international tradeInternational TradeInternational trade is an exchange involving a good or service conducted between at least two different countries. The exchanges can be. Due to the bank’s guarantee, a banker’s acceptance substantially reduces the risk of not receiving the payment for the seller.

It is especially important when there is not a strong relationship between the buyer and seller. As a result, banker’s acceptances are commonly used by importing and exporting businesses, where the importer issues the banker’s acceptance to pay the exporter.

Banker’s Acceptance as an Investment

Banker’s acceptances are exchanged in a liquid secondary marketSecondary MarketThe secondary market is where investors buy and sell securities from other investors. Examples: New York Stock Exchange (NYSE), London Stock Exchange (LSE). and are traded like debt instruments. The instruments are traded through banks and securities dealers and cannot be purchased on an exchange. Since a banker’s acceptance does not provide the holder with a coupon payment, it always trades at a discount to its face value.

The difference between the face value and the price represents the return or yield the buyer will receive. The holder of a banker’s acceptance can either hold the instrument until maturity and receive the face value of the security or sell the security before its maturity, at a discount. The strategy is similar to the one involved in trading zero-coupon bonds.

The price of these securities is often negotiated with the buyers and is largely influenced by the credit ratingCredit RatingA credit rating is an opinion of a particular credit agency regarding the ability and willingness an entity (government, business, or individual) to fulfill its financial obligations in completeness and within the established due dates. A credit rating also signifies the likelihood a debtor will default. of the bank that promised the payment. Since the instruments promise a payment from a financial institution, they are considered relatively safe.

Learn More

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)®Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Credit RiskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally,

- Debt InstrumentDebt InstrumentA debt instrument is a fixed-income asset that legally obligates the debtor to provide the lender interest and principal payments

- Quality of CollateralQuality of CollateralQuality of collateral is related to the overall condition of a certain asset that a company or an individual wants to put as collateral when borrowing funds

- Zero-Coupon BondZero-Coupon BondA zero-coupon bond is a bond that pays no interest and trades at a discount to its face value. It is also called a pure discount bond or deep discount bond.

-

Understanding Average Return: A Simple Guide

Average return is the mathematical average of a sequence of returns that have accrued over time. In its simplest terms, average return is the total return over a time period divided by the number of p

-

Backtesting: A Comprehensive Guide to Strategy Validation

Backtesting involves applying a strategy or predictive model to historical data to determine its accuracy. It can be used to test and compare the viability of trading strategies so tradersSix Essentia

invest

- PC Banking: A Comprehensive Guide to Online Banking Security & Features

- IRA CDs: Secure Retirement Savings with FDIC Insurance

- Understanding the DU: Your Mortgage Approval Explained

- Decentralized Finance (DeFi): A Comprehensive Overview

- Investment Banking: Roles, Responsibilities & Top Employers

- Jumbo CDs: Higher Rates & Deposits Explained

- Understanding Cryptocurrency: A Beginner's Guide to Digital Currency

- DB(k) Plans: A Hybrid Retirement Solution for Employers & Employees

- Understanding Regulation Z: Your Rights as a Borrower

-

Understanding Auction Markets: How Prices Are Determined

Understanding Auction Markets: How Prices Are DeterminedAn auction market is a market where the price is determined by the highest price the buyer is willing to pay (bids), and the lowest price the seller is willing to take (offers). Bids and offers are ma...

-

Understanding Loan Lifespan: What is Average Life?

Understanding Loan Lifespan: What is Average Life?Average life is the length of time that each unit of unpaid principal is expected to remain outstanding. The average life of mortgagesMortgageA mortgage is a loan – provided by a mortgage lender...