Understanding the Yield Curve: A Guide to Economic Health

What tools can you use to measure how strong the U.S. economy is at any given moment?

You might look at job growth or the unemployment rate. You might study the country’s Gross Domestic Product or the spending habits of consumers.

Or you might look at the Treasury bond yield curve.

The direction of this curve – whether it’s trending up or down – can tell you plenty about whether investors think the economy will continue to grow or whether they’re worried that we are heading for an economic slump.

What Is A Yield Curve?

A yield curve, also known as a treasury yield curve or bond yield curve, is a graph, shaped like a curve, designed to help investors compare the yields of bonds of equal credit but different maturity dates.

The curve might, for instance, compare the yields investors are receiving from bonds that mature in 3 months, 5 years, 10 years, 20 years and 30 years.

Yields are important for investors. They represent the amount of cash they'll get from interest or dividends on their investment. Interest rates tend to be higher – and, because of this, the yield, too – on longer-term bonds.

Paying attention to the yield curve for U.S. Treasury bonds is important: The shape of the curve is a good way to track how bond investors are feeling about the economy.

There are three types of yield curves: normal, inverted and flat.

The first one indicates a national economy that is growing at a normal pace. The second two? They could indicate future economic struggles.

A yield curve is a graphical representation of the yields being offered by Treasury bonds of equal quality but differing maturity dates.

A yield curve might chart the yields offered, say, by a bond that matures in 5 months compared to ones that mature in 12 months, 3 years or 5 years.

The Three Types Of Yield Curve

If you want to study yield curves as a tool to help predict the future direction of the economy, it’s important to know the difference between the three types.

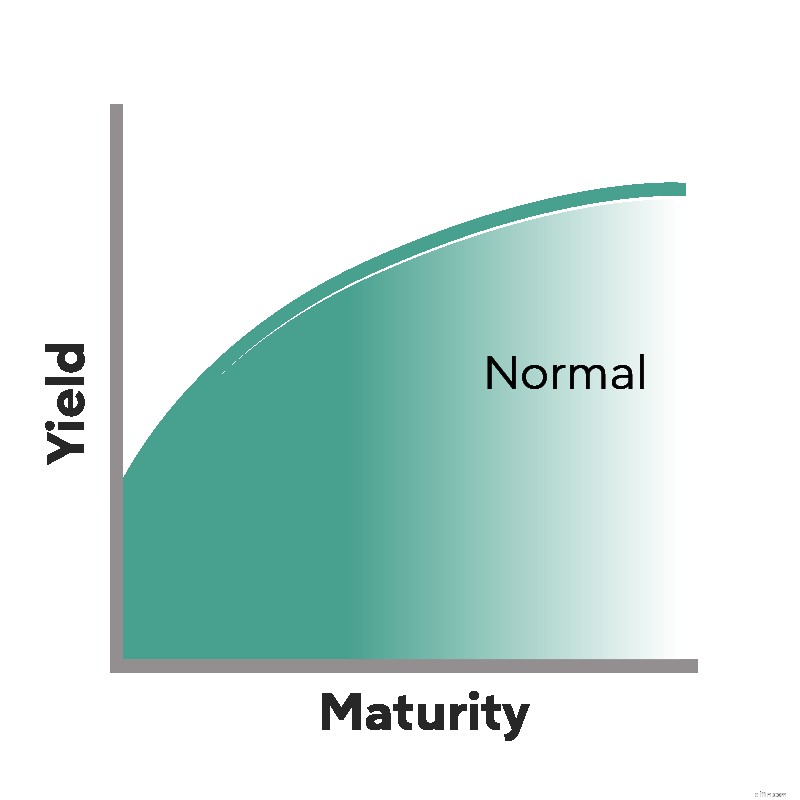

Normal Yield Curve

A normal yield curve slopes upward from left to right. That's because short-term bonds usually produce lower yields than do longer-term ones.

Yields and the interest that bonds generate are higher with longer-term bonds because investors are taking on more risk. The longer investors keep their money in a bond, the greater the risk that they'll lose those funds. Taking on greater risk, though, also comes with the potential for greater reward, or yield. Longer-term bonds pay out more in interest and produce greater yields for investors.

Because yields should rise when investors take on more risk, the yield curve in a normal economic environment should show a slope upward from left to right.

When will you see this type of yield curve? When bond investors are confident that the national economy will grow at a normal pace in the future.

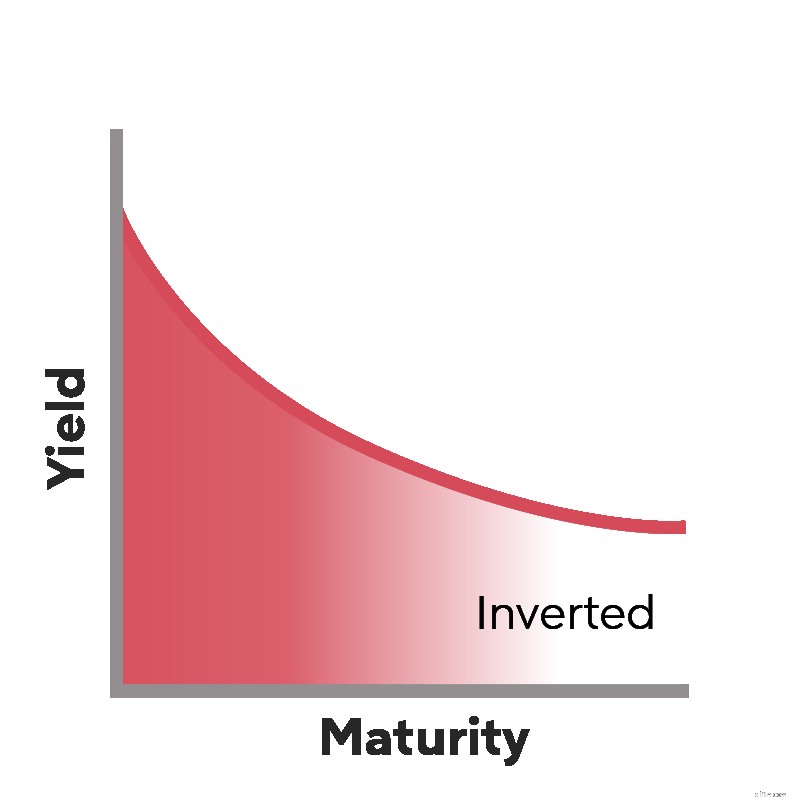

Inverted Yield Curve

As its name suggests, the slope on an inverted curve travels in the opposite direction.

Instead of a curve that slopes upward from left to right as bond maturity dates get longer, the curve in an inverted yield curve slopes downward as bond maturity dates lengthen.

When short-term interest rates are higher than long-term rates. An inverted yield curve could be the sign that an economic slowdown or recession could be on the way.

These curves happen when investors are worried about the future direction of the economy. To protect themselves, they want to lock in safer long-term bonds while they can. This increases demand for these bonds. And when this demand increases, it causes long-term interest rates to fall, resulting in an inverted yield curve.

An example of this came in 2007. The yield curve inverted by the end of 2006 and remained that way into 2007. The Great Recession happened soon after.

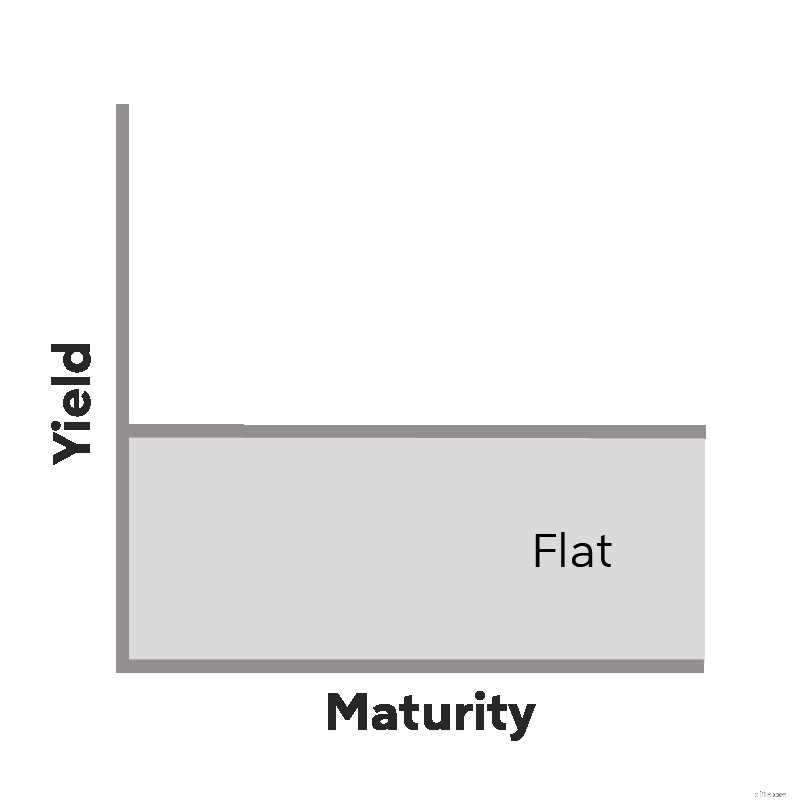

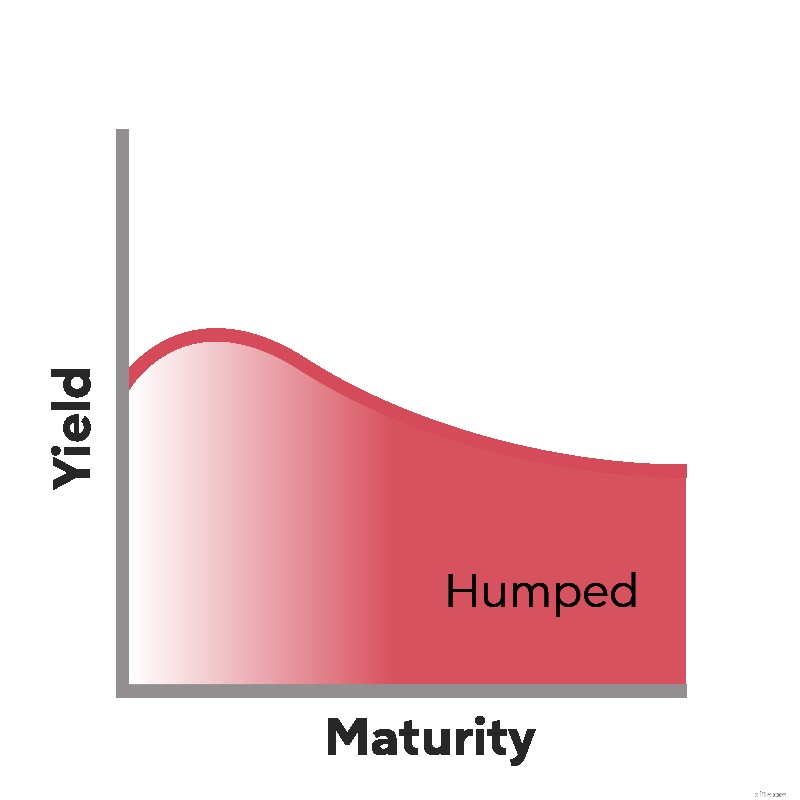

Flat Or Humped Yield Curve

Before it becomes inverted, a yield curve might first transition to a flat or humped curve.

This can happen when the interest rates on short-term bonds are nearly equal to those on long-term rates.

Because there is little difference between the yields on short-term or long-term bonds in these curves, the curve flattens out, with little upward or downward slope from left to right.

If the yields on medium-term bonds are higher than those on lower-term or longer-term ones, this curve will become humped, higher in the middle and lower on the left and right side.

A flat or humped yield curve is a good indication that the economy is going through a transition.

A humped or flat curve isn't a guarantee that the yield curve will become inverted, but is a warning sign that an economic slowdown could be coming.

The Current Yield Curve

You can find information about the current Treasury bond yield curve rates here at the home of the U.S. Department of the Treasury.

When you log on, you'll see the interest rates attached to bonds with varying maturity dates, ranging from 1 month to 30 years. You'll also have the option to view historical yield curve rates.

Yield Curves And Mortgage Rates

If you’re preparing to buy a home, and take out a mortgage to finance it, you’ll want to pay attention to the yield curve. That’s because bonds and mortgage interest rates have historically had an inverse relationship.

When bond interest rates are strong, mortgage interest rates tend to be lower. This is good for home buyers: The lower your mortgage interest rate, the lower your monthly mortgage payment will typically be.

Of course, the yield curve isn’t the only factor that will influence your mortgage interest rate. Your three-digit credit score will also play a major role. Talk to a mortgage expert today to learn about your next home purchase or refinance.

Apply Online with Rocket Mortgage®

Get approved with Rocket Mortgage® and do it all online. You can get a real, customizable mortgage solution based on your unique financial situation. Apply Online-

Understanding Capital Gains Tax on Home Sales: A Comprehensive Guide

Disclosure: This post contains affiliate links, which means we receive a commission if you click a link and purchase something that we have recommended. Pleas

-

IRA Explained: Your Guide to Retirement Savings & Tax Benefits

Disclosure: This post contains affiliate links, which means we receive a commission if you click a link and purchase something that we have recommended. Pleas

Personal finance

- Understanding Inverted Yield Curves: Recession Indicator?

- Understanding the Yield Curve: Definition & Significance

- Understanding 401(k) Plans: A Comprehensive Guide

- Direct Deposit: Benefits, Setup & How It Works

- Understanding Economic Stimulus: Definition, Impact & How It Works

- Hurdle Rate: Definition, Calculation & Investment Uses

- ATM Guide: How ATMs Work & Use - A Comprehensive Explanation

- APR Explained: Understanding the Annual Percentage Rate & Calculation

- Rule of 72: Calculate Investment Growth & Doubling Time

-

Mortgage Forbearance: Understanding Eligibility and Options

Mortgage Forbearance: Understanding Eligibility and OptionsIf youre having trouble making your mortgage payments, contact your lender to see if you qualify for a forbearance. Mortgage forbearance is a temporary pause or reduction in monthly mortgage paym...

-

Personal Loans: A Comprehensive Guide to Understanding and Applying

Ever feel short on cash? If so, a personal loan can help. But what is a personal loan exactly and how does it work in practice? It’s important to do your rese...