Understanding Pension Taxes: A Retirement Planning Guide

When it is time to start collecting from your pension upon retirement, you will be faced with many questions. One of the issues that you will face is taxes on your pension withdrawals. How you deal with these pension taxes can go a long way towards determining how much money you have available for retirement. Here are a few things that you should expect when dealing with pension taxes.

Types of Distribution

Each pension is a little bit different depending on the company. You will usually have a number of different options before you as far as when you can retire. If you stay for 30 years, your pension amount will be less than it is when you have been with the company for 40 years. Therefore, you can plan ahead for when you want to retire.

Once you have met your obligation, you are free to retire and receive your pension. You can usually choose between a few different choices for distribution. One of your options is to receive your money in a lump sum. This results in you getting a check for the entire amount in your pension fund.

Another method allows you to put your money into a lifetime annuity. With this method, you get a monthly payment from the annuity for as long as you are alive. This results in a steady monthly payment for you.

The last common method is a combination of the first two methods. You will be able to get a lump sum and an annuity payment. With this method, the larger lump sum that you receive, the lower your annuity payment will be. Therefore, you will have to assess how much of a lump sum you want and how much of a monthly payment you would like to receive.

Taxes on Distribution

Once you decide exactly how you want to withdraw your money, you will be faced with some taxation issues. If you take out a lump sum, you will be faced with the issue of paying for the taxes on all of it at once. Paying taxes on a huge sum like that will most likely bump you up into the highest tax bracket. Therefore, you will pay more of your total retirement in taxes than if you were to use another method.

If you take the distributions through a monthly annuity payment, you will pay taxes on the money as you get it. Therefore, this will be similar to what you are used to now with your job. You will most likely pay taxes in a lower tax bracket and save more of your entire retirement fund.

If you choose the other option with a lump sum and an annuity, you might have to deal with a little bit of both. Depending on how big your lump sum is, you may jump into a higher tax bracket by the end of the year. Therefore, if you plan it carefully, you can choose a lump sum that will keep you in the lower tax bracket.

-

Understanding Actuarial Gains and Losses in Pensions

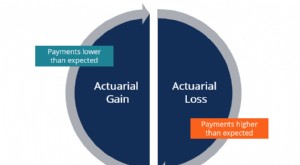

Actuarial gains or losses refer to the differences between an employer’s actual pension payments relative to the expected payments. When the employer’s payments are higher than expected, i

-

Understanding Emerging Markets ETFs: Opportunities & Performance

Emerging markets ETF follow the performance of countries such as Brazil, India and other new opportunity funds in economies and countries that are developing. An emerging markets ETF, or ex

retire

- Understanding Pensions: How They Work & Benefit Calculations

- Union Pension Annuities: A Comprehensive Guide

- Understanding Taxes on Pension Benefits: A Comprehensive Guide

- Understanding Income: Definition, Types & Uses

- Understanding After-Tax Income: A Comprehensive Guide

- NOPLAT Explained: Understanding Adjusted Operating Profit

- Understanding Form 1099-R: Pension & Retirement Income Taxes

- Maximize Retirement Savings: Understanding Tax Benefits of Pension Plans

- FICA Taxes Explained: Social Security & Medicare – Credit Karma Tax

-

401(k) Tax Advantages: What's Excluded from Taxes?

401(k) Tax Advantages: What's Excluded from Taxes?What Taxes Are 401(k)s Exempt From? A 401(k) is an employer-sponsored retirement plan that allows pretax contributions, which provide tax savings. To enable the pretax feature, the plan must ...

-

Rule of 85 Retirement: Early Retirement Eligibility Explained

Rule of 85 Retirement: Early Retirement Eligibility ExplainedIf you work for a company or government agency that offers a defined-benefit pension plan, there might be a provision in the plan rules allowing you to retire early and still qualify for full benefits...