Understanding Accumulated Other Comprehensive Income (AOCI)

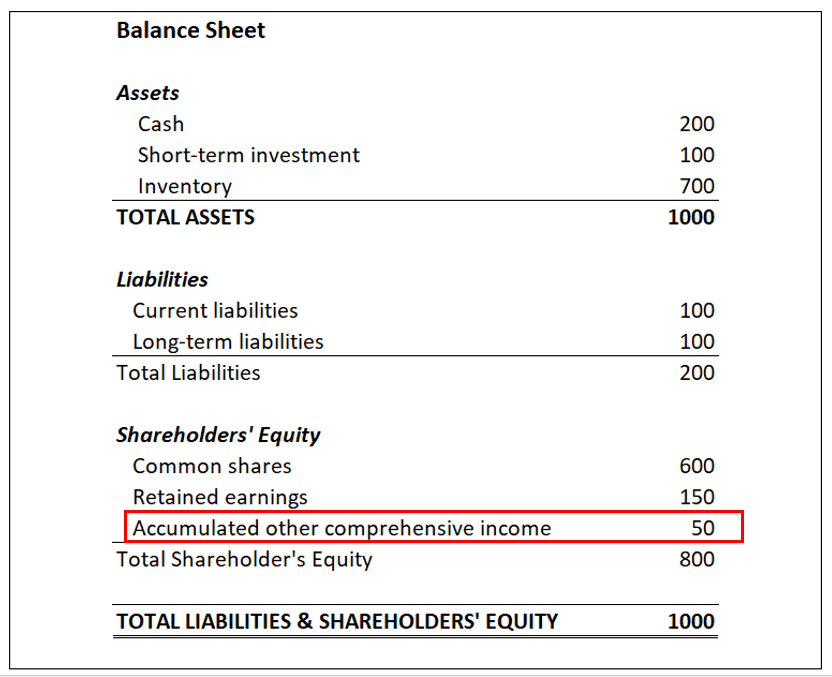

Accumulated Other Comprehensive Income (AOCI) are special gains and losses that are listed as special items in the shareholder equity section of a company’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting.. The AOCI account is the designated space for unrealized profits or losses on items that are placed in the other comprehensive income category. Any transaction – whether it is a loss (deduction) or a profit (credit) – is deemed “unrealized” when it has not been completed.

For example: If a company makes investments in the stock marketStock MarketThe stock market refers to public markets that exist for issuing, buying and selling stocks that trade on a stock exchange or over-the-counter. Stocks, also known as equities, represent fractional ownership in a company, the open profits or losses on the investments are properly listed in the other comprehensive income section of the balance sheet until the stocks are sold, at which time the profits/losses are realized.

Breaking Down an AOCI Account

Several types of profits or losses are eligible to be listed in an Accumulated Other Comprehensive Income account. They include profits or losses related to foreign currency transactions, unrealized profits or losses that are yet to reach maturity, and costs related to operating a pension plan.

After a profit or loss is realized, it is moved from the AOCI account into the net income section of the company’s balance sheet.

The use of AOCI accounts is mandatory, except in the case of privately-held companiesPrivately Held CompanyA privately held company is a company’s whose shares are owned by individuals or corporations and that does not offer equity interests to investors in the form of stock shares traded on a public stock exchange. and non-profit organizations. As long as financial statements don’t need to be submitted to outside parties, a company is not required to use AOCI accounts.

Regulations Surrounding AOCI Accounts

The Financial Accounting Standards Board (FASB) issued a new standard in 1997, requiring a comprehensive accounting of all income, including “other” or special types of income, specifically the profits and losses that are, in the present, not finalized. The ruling made AOCI accounts mandatory for all publicly-traded companies in the US.

Reporting Accumulated Other Comprehensive Income accounts thoroughly and accurately on a balance sheet is important because the gains and losses affect the balance sheet as a whole and the comprehensive income of a business. The items, however, do not affect net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through, retained earnings, or the income statement in terms of actual, finalized income until the transactions are completed and are moved to a different section of the balance sheet.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Journal Entries GuideJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits)

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Statement of Comprehensive IncomeStatement of Comprehensive IncomeThe Statement of Comprehensive Income provides a summary of a company’s net assets over a given period of time. In other words, the statement

-

Accounting Conservatism: Definition, Examples & Importance

Accounting conservatism refers to financial reporting guidelines that require accountants to exercise a high degree of verification and utilize solutions that show the least aggressive numbers when fa

-

Understanding After-Tax Income: A Comprehensive Guide

After-tax income refers to the net income after deducting all applicable taxes. Therefore, the after-tax income is simply one’s gross income minus taxes. For individuals and corporations, the af

Accounting

- Net Interest Income (NII): Definition & Calculation

- Accounting Explained: Understanding Financial Records & Reporting

- Understanding Accounting Income: A Key Financial Metric

- Accrued Income Explained: Definition & Accounting

- Understanding Accumulated Depreciation: A Comprehensive Guide

- Understanding Financial Audits: A Comprehensive Guide

- Understanding Other Comprehensive Income (OCI): A Comprehensive Guide

- Understanding the Statement of Comprehensive Income: A Comprehensive Guide

- FAFSA Income Limits: What You Need to Know for College Aid

-

Understanding the Role of an Accountant: Key Responsibilities & Importance

Understanding the Role of an Accountant: Key Responsibilities & ImportanceAn accountant plays a very crucial role in an organizationTypes of OrganizationsThis article on the different types of organizations explores the various categories that organizational structures can ...

-

Understanding the Three Core Financial Statements

Understanding the Three Core Financial StatementsThe three financial statements are: (1) the Income StatementIncome StatementThe Income Statement is one of a companys core financial statements that shows their profit and loss over a period of time.&...