Understanding Bad Debt: Definition and Financial Statement Impact

First, let’s determine what the term bad debt means. Sometimes, at the end of the fiscal periodFiscal Year (FY)A fiscal year (FY) is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to formulate annual, when a company goes to prepare its financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are, it needs to determine what portion of its receivables is collectible. The portion that a company believes is uncollectible is what is called “bad debt expense.” The two methods of recording bad debt are 1) direct write-off method and 2) allowance method.

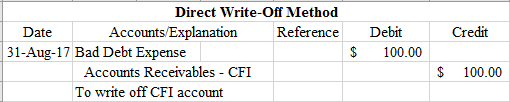

Bad Debt Direct Write-Off Method

The method involves a direct write-off to the receivablesAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow account. Under the direct write-off method, bad debt expense serves as a direct loss from uncollectibles, which ultimately goes against revenues, lowering your net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through. For example, in one accounting period, a company can experience large increases in their receivables account. Then, in the next accounting period, a lot of their customers could default on their payments (not pay them), thus making the company experience a decline in its net income. Therefore, the direct write-off method can only be appropriate for small immaterial amounts. We will demonstrate how to record the journal entries of bad debt using MS Excel.

Bad Debt Allowance Method

When it comes to large material amounts, the allowance method is preferred compared to the direct write-off method. However, many companies still use the direct write-off for small amounts. The reason for the preference is because the method involves a contra asset account that goes against accounts receivables. A contra asset account is basically an account with an opposite balance to accounts receivables and is recorded on the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. as such:

The reason why this contra account is important is that it exerts no effect on the income statement accounts. It means, under this method, bad debt expense does not necessarily serve as a direct loss that goes against revenues.

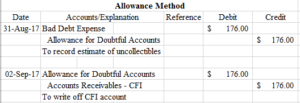

The three primary components of the allowance method are as follows:

- Estimate uncollectible receivables.

- Record the journal entry by debiting bad debt expense and crediting allowance for doubtful accounts.

- When you decide to write off an account, debit allowance for doubtful accountsAllowance for Doubtful AccountsThe allowance for doubtful accounts is a contra-asset account that is associated with accounts receivable and serves to reflect the true value of accounts receivable. The amount represents the value of accounts receivable that a company does not expect to receive payment for. and credit the corresponding receivables account.

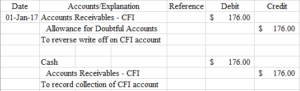

Sometimes, people or businesses pay back the amount but at a later date, which means that you need to reverse the write off you made and record the collection of the receivables. It would involve the following entry:

How to Estimate Accounts Receivables

As mentioned earlier in our article, the amount of receivables that is uncollectible is usually estimated. Why? This is because it is hard, almost impossible, to estimate a specific value of bad debt expense. Companies cannot control how or when people pay. Sometimes people encounter hardships and are unable to meet their payment obligations, in which case they default. The same thing happens to companies as well. Therefore, there is no guaranteed way to find a specific value of bad debt expense, which is why we estimate it within reasonable parameters.

The two methods used in estimating bad debt expense are 1) Percentage of sales and 2) Percentage of receivables.

1. Percentage of Sales

Percentage of sales involves determining what percentage of net credit sales or total credit sales is uncollectible. It is usually determined by past experience and anticipated credit policy. Once management calculates the percentage, they multiply it by their net credit sales or total credit sales to determine bad debt expense. Here’s an example:

On March 31, 2017, Corporate Finance Institute reported net credit sales of $1,000,000. Using the percentage of sales method, they estimated that 1% of their credit sales would be uncollectible.

As you can see, $10,000 ($1,000,000 * 0.01) is determined to be the bad debt expense that management estimates to incur.

2. Percentage of Receivables

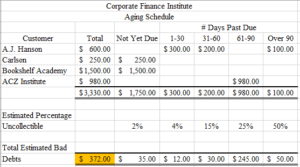

Under the percentage of receivables method of estimating bad debt expense, companies prepare an aging schedule, as shown below:

Again, the percentages are determined by past experience and past data. The most important part of the aging schedule is the number highlighted in yellow. It represents the amount that is required to be in the allowance of doubtful accounts. However, if there is already a credit balance existing in the allowance of doubtful accounts, then we only need to adjust it. For example, let’s assume that there was a $100 credit already existing in the allowance account. In order to record the adjustment, we simply take the $372 and subtract the $100, giving us $272 and we record it as follows:

What if, instead of a credit balance in the allowance account, we posted a debit balance prior to the adjustment? Well, in this case, we would simply add. For example, let’s say there was a $175 debit existing in the allowance account. In order to record the adjustment, we simply take the $372 and add the $175 to get $547 and we record it as follows:

Importance of Bad Debt Expense

Every fiscal year or quarter, companies prepare financial statements. The financial statements are viewed by investors and potential investors, and they need to be reliable and must possess integrity. Investors are putting their hard-earned money into the company and if companies are not providing truthful financial statements, it means that they are cheating investors into placing money into their company based on false information.

Bad debt expense is something that must be recorded and accounted for every time a company prepares its financial statements. When a company decides to leave it out, they overstate their assets and they could even overstate their net income.

Bad debt expense also helps companies identify which customers default on payments more often than others. If a company does decide to use a loyalty system or a credibility system, they can use the information from the bad debt accounts to identify which customers are creditworthy and offer them discounts for their timely payments.

Learn More

If you think you have mastered bad debt expense and how to record it, make sure to check out these related articles to get a deeper understanding of other accounting concepts:

- Debt ScheduleDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows

- Guide to Journal EntriesJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits)

- Net DebtNet DebtNet debt = total debt - cash. Net debt is a financial liquidity metric that measures a company’s ability to pay all its debts if they were due today. Compares a company’s total debt with its liquid assets.

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

Understanding Current Debt: Definition & Implications

Current debt includes the formal borrowings of a company outside of accounts payableAccounts PayableAccounts payable is a liability incurred when an organization receives goods or services from its su

-

Understanding Debt: Is All Debt Bad?

There are different types of debt, and it’s easy to try to lump debt into two distinct Wizard of Oz witch-like categories: good debt and bad debt. Debt can’t be that bad for you, right? E

Accounting

- Understanding Personal Debt: Definition, Types & Impact

- Understanding Debt: Types, Impact & Management

- Understanding Delinquent Debt: Causes, Consequences, and Solutions

- Understanding Capital: Types, Categories & Value Creation

- Understanding Debt: Types, Obligations & Financial Implications

- Understanding Debt Capacity: A Guide for Businesses

- Understanding Bad Debt Expense: Accounting & Methods

- Understanding Debt: Types, Impact & How to Manage It

- Understanding Bad Debt: Definition, Causes & Accounting

-

Venture Debt: A Comprehensive Guide for Startups

Venture Debt: A Comprehensive Guide for StartupsVenture debt is a type of debt financing obtained by early-stage companies and startupsStartup Valuation Metrics (for internet companies)Startup Valuation Metrics for internet companies. This guide ou...

-

Margin Debt Explained: Understanding Brokerage Loans for Investing

Margin Debt Explained: Understanding Brokerage Loans for InvestingMargin debt represents the amount that an investor owes a broker in their margin account. When a broker approves a margin account for an investor, the margin account is granted a line of credit that c...