Retained Earnings: Definition, Calculation & Importance

Retained Earnings (RE) are the accumulated portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations.

Retained Earnings are reported on the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. under the shareholder’s equity section at the end of each accounting period. To calculate RE, the beginning RE balance is added to the net income or reduced by a net loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period.

The Purpose of Retained Earnings

Retained earnings represent a useful link between the income statement and the balance sheet, as they are recorded under shareholders’ equity, which connects the two statements. The purpose of retaining these earnings can be varied and includes buying new equipment and machines, spending on research and development, or other activities that could potentially generate growth for the company. This reinvestment into the company aims to achieve even more earnings in the future.

If a company does not believe it can earn a sufficient return on investment from those retained earnings (i.e., earn more than their cost of capital), then they will often distribute those earnings to shareholders as dividends or conduct a share buybacks.

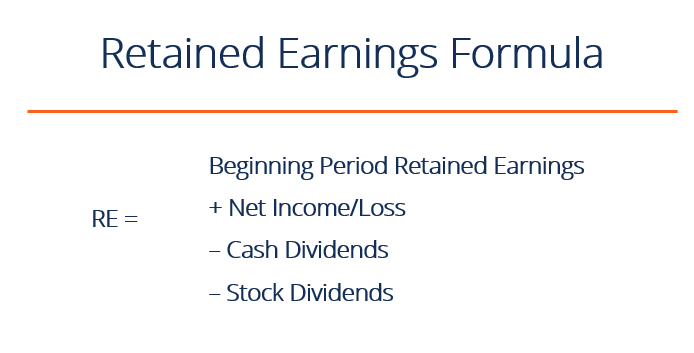

What is the Retained Earnings Formula?

The RE formula is as follows:

RE = Beginning Period RE + Net Income/Loss – Cash Dividends – Stock Dividends

Where RE = Retained Earnings

Beginning of Period Retained Earnings

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number, as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

How Net Income Impacts Retained Earnings

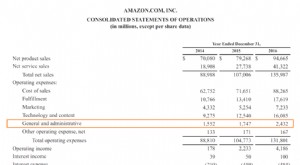

Any changes or movement with net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through will directly impact the RE balance. Factors such as an increase or decrease in net income and incurrence of net loss will pave the way to either business profitability or deficit. The Retained Earnings account can be negative due to large, cumulative net losses. Naturally, the same items that affect net income affect RE.

Examples of these items include sales revenue, cost of goods sold, depreciation, and other operating expenses. Non-cash items such as write-downs or impairments and stock-based compensation also affect the account.

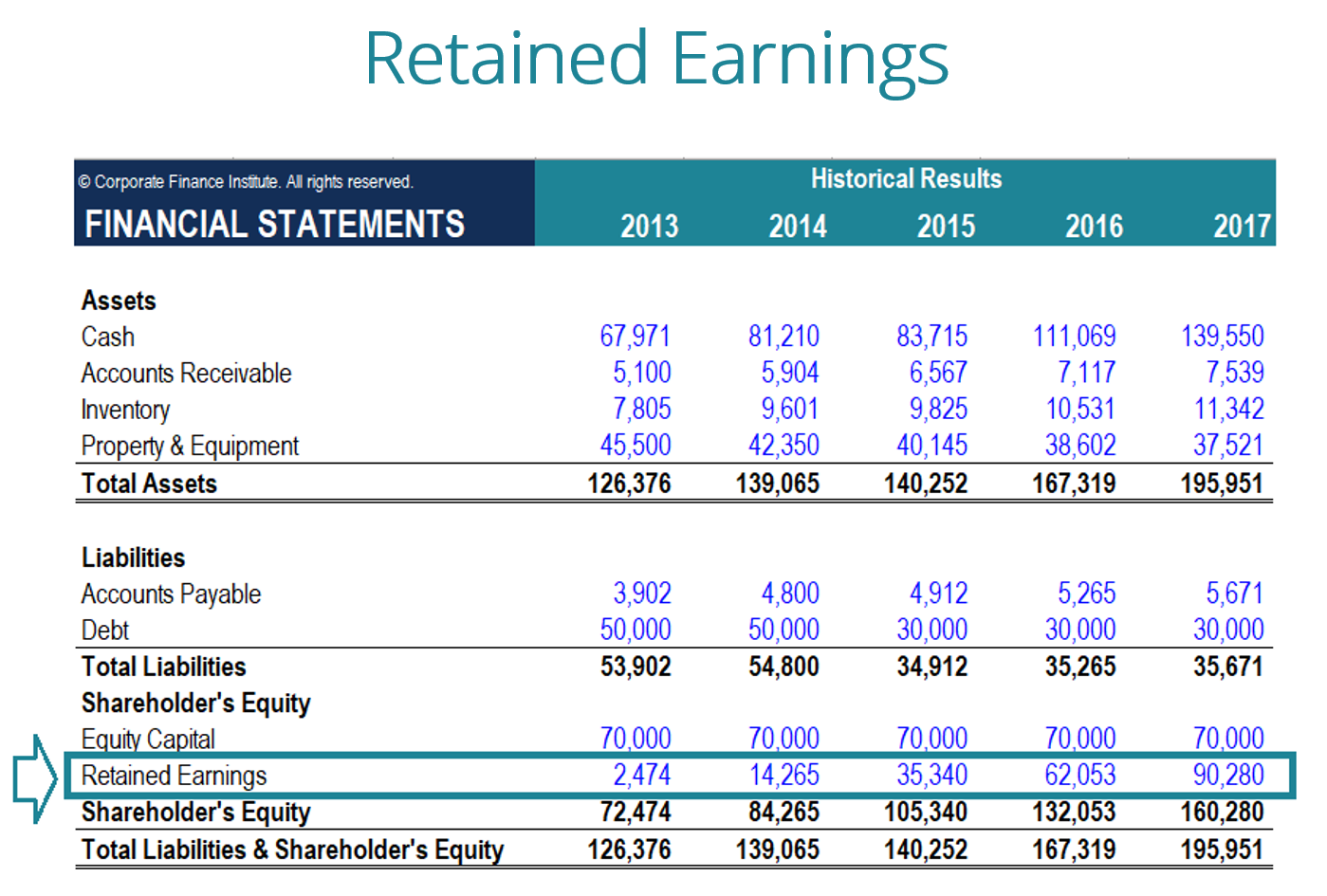

Image: CFI’s Financial Modeling Course.

How Dividends Impact Retained Earnings

Distribution of dividends to shareholders can be in the form of cash or stock. Both forms can reduce the value of RE for the business. Cash dividends represent a cash outflow and are recorded as reductions in the cash account. These reduce the size of a company’s balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. and asset value as the company no longer owns part of its liquid assets.

Stock dividends, however, do not require a cash outflow. Instead, they reallocate a portion of the RE to common stock and additional paid-in capital accounts. This allocation does not impact the overall size of the company’s balance sheet, but it does decrease the value of stocks per share.

Learn more: how to forecast a company’s balance sheetProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate.

End of Period Retained Earnings

At the end of the period, you can calculate your final Retained Earnings balance for the balance sheet by taking the beginning period, adding any net income or net loss, and subtracting any dividends.

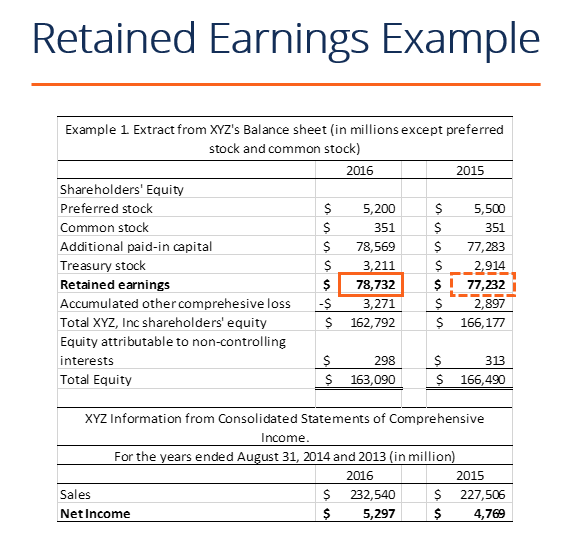

Example Calculation

In this example, the amount of dividends paid by XYZ is unknown to us, so using the information from the Balance Sheet and the Income Statement, we can derive it remembering the formula Beginning RE – Ending RE + Net income (-loss) = Dividends

We already know:

Beginning RE: $77,232

Ending RE: $78,732

Net Income: $5,297

So, $77,232 – $78,732 + $5,297= $3,797

Dividends paid = $3,797

We can confirm this is correct by applying the formula of Beginning RE + Net income (loss) – dividends = Ending RE

We have then $77,232 + $5,297 – $3,797 = $78,732, which is in fact our figure for Ending Retained Earnings

Video Explanation of Retained Earnings

Below is a short video explanation to help you understand the importance of retained earnings from an accounting perspective.

This video is taken from CFI’s Financial Analysis Fundamentals Course.

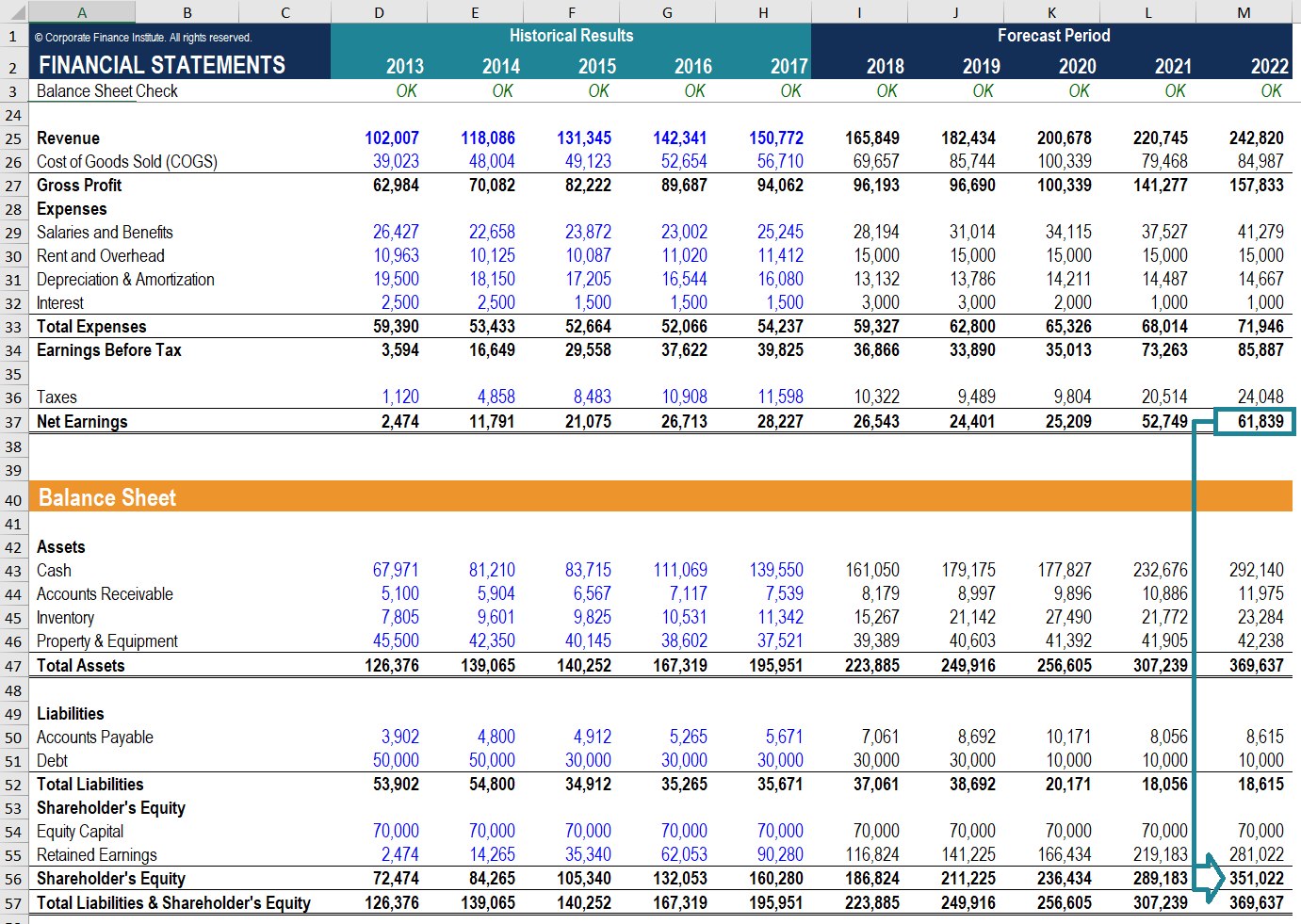

Applications in Financial Modeling

In financial modeling, it’s necessary to have a separate schedule for modeling retained earnings. The schedule uses a corkscrew type calculation, where the current period opening balance is equal to the prior period closing balance. In between the opening and closing balances, the current period net income/loss is added and any dividends are deducted. Finally, the closing balance of the schedule links to the balance sheet. This helps complete the process of linking the 3 financial statements in ExcelHow the 3 Financial Statements are LinkedHow are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and.

To learn more, check out our video-based financial modeling courses.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To help you advance your career, check out the additional CFI resources below:

- Three Financial StatementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are

- 3-Statement Model3 Statement ModelA 3 statement model links the income statement, balance sheet, and cash flow statement into one dynamically connected financial model. Examples, guide

- Income Statement TemplateIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or

- Guide to Financial ModelingFree Financial Modeling GuideThis financial modeling guide covers Excel tips and best practices on assumptions, drivers, forecasting, linking the three statements, DCF analysis, more

-

Understanding Assurance Services: Risk Reduction & Improved Decisions

Assurance services are an independent examination of a company’s processes and controls. Assurance aims to reduce information risk by improving the quality or context of the information. &n

-

Balance Sheet Explained: A Comprehensive Guide for Finance Professionals

The balance sheet is one of the three fundamental financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash fl

Accounting

- Balance Sheet Reconciliation: A Comprehensive Guide for Business Owners

- Understanding Earnings: A Guide to Financial Profitability

- Headline Earnings: Understanding Core Business Performance

- Understanding Non-GAAP Earnings: A Comprehensive Guide

- Understanding Normalized Earnings: A Guide for Investors

- Understanding Earnings Surprises: What Are They?

- Retained Earnings: Definition, Calculation & Significance

- Retained Earnings: Definition, Calculation & Importance

- Retained Earnings: Definition, Calculation & Importance

-

Understanding Accounting Ratios: A Comprehensive Guide

Understanding Accounting Ratios: A Comprehensive GuideAccounting ratios cover a wide array of ratios that are used by accountants and act as different indicators that measure profitability, liquidityLiquidityIn financial markets, liquidity refers to how ...

-

Understanding Administrative Expenses: A Comprehensive Guide

Understanding Administrative Expenses: A Comprehensive GuideAdministrative expenses refer to the costs incurred by a company or organization that include, but are not limited to, the salaries and benefitsRemunerationRemuneration is any type of compensation or ...