Mastering FP&A: A Guide to Understanding the Core Financial Statements

Anyone working in the financial planning and analysis (FP&A) department should be very familiar with the three financial statements in FP&A – Income StatementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or, Balance SheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting., and Cash Flow StatementCash Flow StatementA cash flow Statement contains information on how much cash a company generated and used during a given period.. Each of the financial statements provides important financial figures, during certain time periods, for the internal and external stakeholdersStakeholderIn business, a stakeholder is any individual, group, or party that has an interest in an organization and the outcomes of its actions. Common examples of a company.

The income statement reveals the profitability of a company by displaying the revenue, cost of goods soldCost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct, net income, and various expenses. A balance sheet states a company’s assets, liabilities, and shareholders’ equityStockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus at a particular point in time. The cash flow statement displays cash flows from operations, financing, and investing activities both into and outside of the business.

Why Should an FP&A Analyst Know About the Three Financial Statements?

While it is not necessary that an FP&A analyst be capable of producing and maintaining the three financial statements in FP&A, he/she should understand the basic components of these statements and the meaning behind each of the figures. It is especially critical for FP&A analysts who are responsible for financial modeling, financial analysis, and forecasting a business’s future profitability, which requires the extraction of historical data.

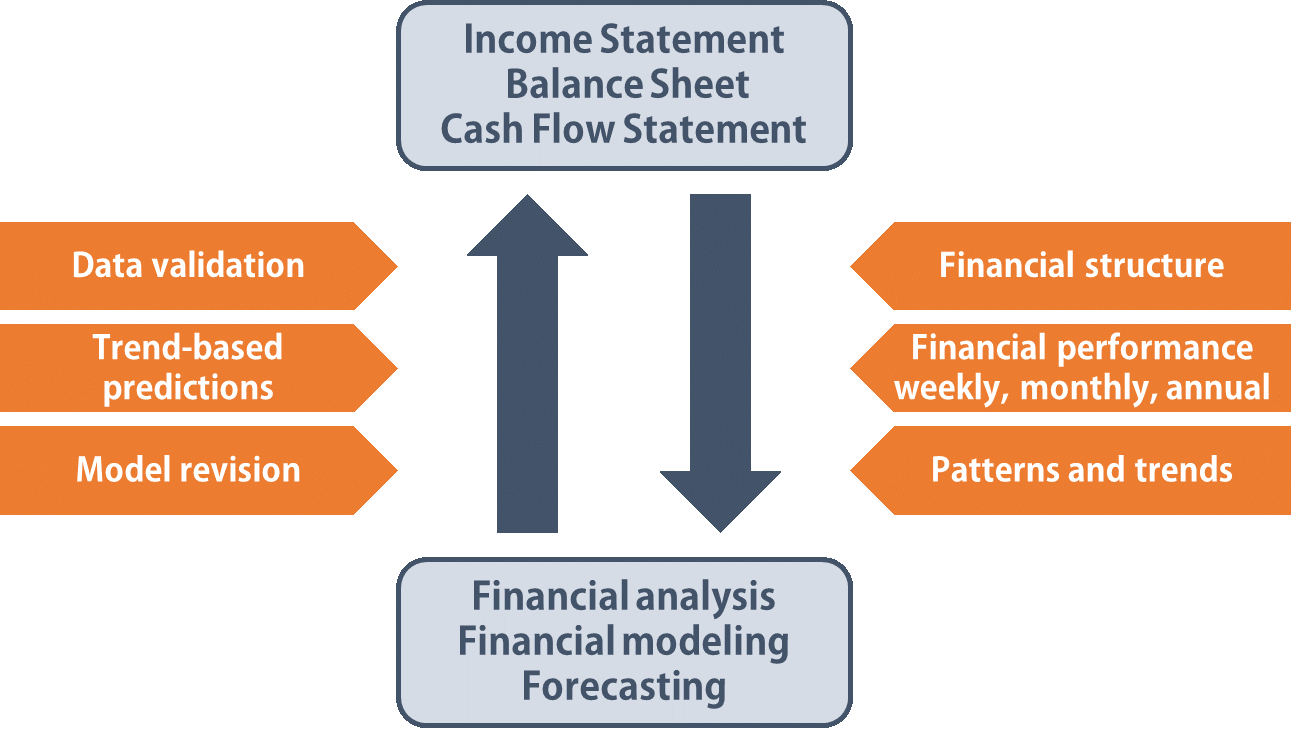

1. The statements help an FP&A analyst understand the financial structure and past performance.

It is an essential first step for an FP&A analyst to learn about a company’s financial status and structure before beginning any analysis. The three financial statements summarize all the significant numbers an analyst needs to know, ranging from the revenue streams from which a business generates its earnings, to the composition of its cost structures and methods of allocating costs.

The FP&A analyst would also want to find out how the company performed over the past years in order to understand growth or decline in its operating efficiency. With this information, an analyst can already get a sense of earnings and cost trends ahead of performing analyses.

2. The statements provide necessary information for financial modeling.

Information found on the three financial statements is constantly used in different kinds of financial analysis and forecasting processes. For example, an FP&A analyst has to extract information such as the revenue and expenses of the entire business and each individual department from the income statement to build a consolidation model.

For large companies, their financial statements can be very comprehensive yet long to search through. An FP&A analyst should be able to pick from the statements the right numbers to use in their calculations and quickly realize variances in these data.

3. Constant updates on financial data are needed for the forecasting process.

Forecasting is the process of looking at historical data and analyzing patterns to predict a business’ short-term performance going forward, on a weekly or monthly basis. Maintaining a forecasting model requires frequent monitoring and revising by an FP&A analyst, and therefore, he/she should continually collect data from monthly financial statements and refine the forecasting model with the latest information to produce an accurate prediction.

The financial statements also help an FP&A analyst realize the opportunities and risks the company is facing. For example, a leverage risk to a company may be signaled when it raises a large amount of capital through short-term and long-term debt.

An FP&A analyst should factor this into their forecast since higher interest expenses and larger cash outflows to service debt are expected as the company repays its principal and interest. A good analysis can help company management exercise proper caution when planning to take on large projects or invest in developing new product lines.

4. Business planning requires the collection of long-term financial results from past statements.

A long-range business plan (LRBP) outlines a company’s long-term plan and prediction on future performance for a period of between five to ten years. To come up with a reliable long-range plan, an FP&A analyst must gather historical data from the financial statements for at least the past five years to comprehend long-term trends in the company’s operations.

Factors such as the revenue growth rate and return on invested capital should be taken into consideration when an FP&A analyst budgets project expenses and maps out long-term resource allocation.

5. The three financial statements act as a source for validation in financial models.

After constructing a financial model and placing all the data in the right places, an FP&A analyst should always validate the data to ensure the accuracy of the calculations. The three financial statements then become the optimal sources for data reconciliations because they are the formal records of the financial performance of the business.

When inconsistencies are found between a number in a model and in the financial statement, an FP&A analyst should revise the model to match the financial statement before proceeding. It is common practice in financial modeling to insert a column of numbers, such as the total revenue and total allocation costs, directly linked to the financial statement at the end of a financial model for prompt comparisons.

Related Resources

Thank you for reading our guide to the three financial statements in FP&A. CFI is the global provider of the global Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below may be useful:

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- How the 3 Financial Statements are LinkedHow the 3 Financial Statements are LinkedHow are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and

- Types of Financial ModelsTypes of Financial ModelsThe most common types of financial models include: 3 statement model, DCF model, M&A model, LBO model, budget model. Discover the top 10 types

- Guide to Financial ModelingFree Financial Modeling GuideThis financial modeling guide covers Excel tips and best practices on assumptions, drivers, forecasting, linking the three statements, DCF analysis, more

-

Calculate MIRR Using WACC: A Step-by-Step Guide

The modified internal rate of return (MIRR) calculates the return earned on an investment while taking into consideration that you may not be able to re-invest the money you earn at the same rate the

-

Achieving Wealth in the USA: Strategies & Opportunities

Becoming rich in America takes hard work. The United States is called the "Land of Opportunity" for a reason. Many millionaires in America are self-made, coming from humble beginnin

Accounting

- Using Gas Cards at the Pump: A Simple Guide

- Laundry Hacks: Using Salt for Stain Removal & Fabric Care

- Understanding Principal Payments in Financial Statements

- Understanding Inventory Purchases: Calculation & Reporting

- Understanding the Interrelationship of Financial Statements

- CPA vs. CFA: Understanding the Differences & Choosing the Right Finance Designation

- Understanding the Three Core Financial Statements

- Understanding Financial Statements: A Beginner's Guide

- FreshBooks Mobile App: Streamline Invoicing & Expense Tracking (2024 Update)

-

Lighter Fluid Uses Beyond Cigarettes: Cleaning & Household Hacks

Lighter Fluid Uses Beyond Cigarettes: Cleaning & Household HacksUse Lighter Fluid Around the House How to Use Lighter Fluid Around the House. With disposal lighters so common today, lighter fluid has been pushed to the rear of the shelf. That's a sham...

-

Understanding Common Equity: Definition & Significance

A company's stockholders' equity on its balance sheet is the accounting value of all stockholders' interest in the company if the company were to pay off all of its debts. Common stock is ...