CPA vs. CFA: Understanding the Differences & Choosing the Right Finance Designation

The notice to reader report is a compilation of financial statements using financial data provided by the management. The report is prepared by an external chartered accountantCPA vs CFA®When considering a career in corporate finance or the capital markets you will often hear people asking, “Should I get a CPA or CFA?” and “Which is better?”. In this article, we will outline the similarities and differences of the CPA vs CFA designations and try to steer you in the right direction about, and it does not provide assurance on the correctness of the financial statements.

The notice means that the prepared financial statements have not been audited or reviewed, and therefore, the accountant offers no assurance on the accuracy of the financial statement. However, the report gives confidence to certain users, such as directors and shareholders of the company.

The goal of the notice to reader is to use the information provided by the management or owners and prepare and present financial statements that are correct and not misleading in the opinion of the management.

The main financial statements prepared in the report include the income statement, balance sheet, cash flow statement, and statement of retained earningsStatement of Retained EarningsThe statement of retained earnings provides an overview of the changes in a company's retained earnings during a specific accounting cycle. It is structured as an equation, such that it opens with the retained earnings at the beginning of the reporting period, makes adjustments for items such as net income and dividends. Each page of the notice to reader report should include a “notice to reader” note at the top of the page to denote the level of usefulness of the report. It cautions users that the report may not be appropriate for their use since it is prepared for a specific purpose.

Key Components of the Notice to Reader Report

The following are some of the elements included in the notice to reader report:

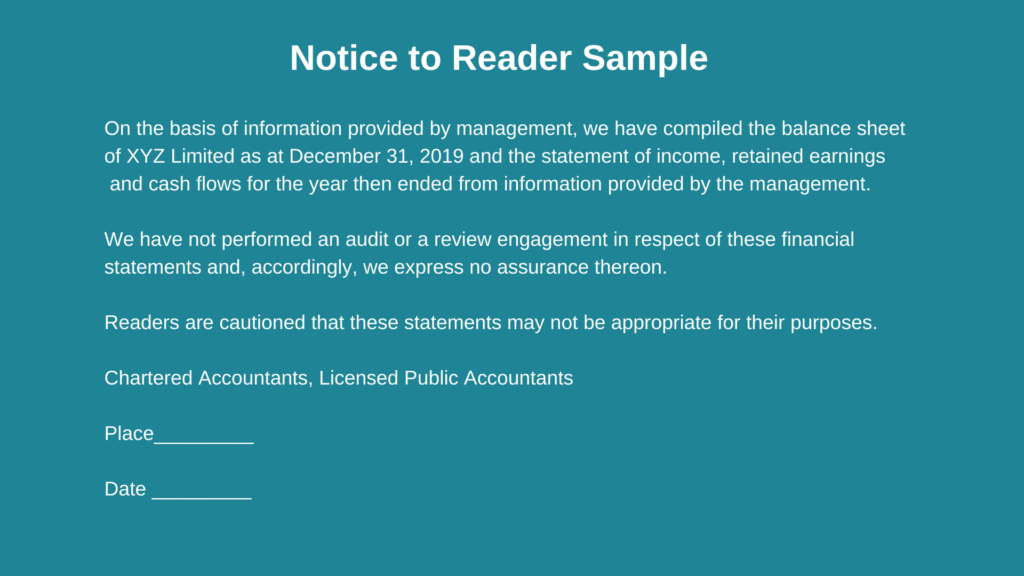

1. Nature of assignment

The report explicitly states the nature of work that the accountant is required to perform. The accountant should state that compiled financial statements were prepared based on the information provided by the management or owners of the company, and that that he/she did not conduct an audit or review of the statements. It cautions users of the financial statement from interpreting the report as a vote of confidence on the correctness of the financial statements.

2. Scope limitation

The report also discloses the scope of limitation of the accountant’s work. The limitation informs users of the report that there is no form of assurance that is expressed on the financial statements.

3. Caution to reader

The compiled financial statements should include a “notice to reader” heading to denote that it is not appropriate for the user’s purposes. The management furnishes the accountant with information to be used in compiling financial statements, and it is necessary to caution readers on the level of reliability they should place on the report.

Qualities of the Notice to Reader Report

1. Prepared by an external chartered accountant

Notice to reader financial statements are prepared by a licensed external chartered accountant or a CPA. The financial statements cannot be prepared by the in-house accountant or bookkeeper using the company’s accounting systems. However, if the company uses an external accountant to prepare year-end tax returns, it can use the same accountant to prepare the notice to reader financial statements.

2. Financial statements are not audited

Although notice to reader reports are prepared by an external professional accountant, the accountant only prepares the financial statements based on the information provided by management and does not audit the numbers to verify their accuracy.

The compiled financial statements should be clearly marked “unaudited” to inform readers that the prepared reports have not been audited and should not be interpreted as an assurance on the correctness of the compiled statements.

3. Purpose of financial statements

The notice to reader financial statements should include a note that cautions readers that the compiled statements may not be appropriate for their purpose. Usually, the statement is prepared for specific purposes, such as obtaining bank financing Bank LineA bank line or a line of credit (LOC) is a kind of financing that is extended to an individual, corporation, or government entity, by a bank or otherfrom a financial institution or when selling the business. Such financial statements may not be appropriate for other types of users.

4. Nature of work

The purpose of the notice to reader is to compile financial statements based on the raw financial data provided by the management. The external accountant is provided with data, and they are not required to verify the authenticity of the information provided.

While licensed accountants are required to maintain their independence from their client, the standards that guide notice to reader financial statements are usually less strict on the expected performance of the practitioner.

Uses of the Notice to Reader Report

Here are some of the reasons why notice to reader report may be prepared:

1. Investors

When investing in small companies or startups, investors may require key financial statements to analyze the companies’ assets vs. liabilities, profitability, and future growth potential. The accountant will be required to prepare financial statements that provide specific information that the investors require.

2. Selling a business

During a merger or acquisition transaction, prospective buyers may require financial statements for the past three to five years to help in their due diligenceDue DiligenceDue diligence is a process of verification, investigation, or audit of a potential deal or investment opportunity to confirm all relevant facts and financial information, and to verify anything else that was brought up during an M&A deal or investment process. Due diligence is completed before a deal closes.. The management may engage an external accountant to prepare the notice to reader financial statements that provide the information required by prospective buyers.

A review or audit engagement may only be required in complex M&A transactions or in the case of large companies with substantial annual revenues.

3. Creditors

Banks may require clients to furnish them with the latest financial statement during the assessment of credit applications or routine evaluation of the creditworthiness of existing borrowers. The company may require the external accountant to prepare specific financial statements that provide the information required by the creditor.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- M&A Considerations and ImplicationsM&A Considerations and ImplicationsWhen conducting M&A a company must acknowledge & review all factors and complexities that go into mergers and acquisitions. This guide outlines important

- Notes to Financial StatementsFinancial Statement NotesFinancial statement notes are the supplemental notes that are included with the published financial statements of a company. The notes are

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

The Critical Role of Audits in Legal Compliance

The legal importance of an audit is to uphold the reliability of financial statements for all external users. AuditorsAuditorAn auditor is a person or a firm assigned to perform an audit on

-

Bookkeeping vs. Accounting: Key Differences Explained

Bookkeeping and accounting share some commonaliti

Accounting

- Understanding R1 & I1 Credit Report Codes: What They Mean

- Harmonized Financial Statements: Pros, Cons, and Global Impact

- Understanding Call Reports: A Guide to Bank Financial Health

- Understanding Auditor's Reports: A Comprehensive Guide

- Understanding Financial Statement Notes: A Comprehensive Guide

- Understanding Financial Statements: A Comprehensive Guide

- Understanding Materiality Thresholds in Audits: A Comprehensive Guide

- Understanding the Philosophy of Accounting: Principles & Concepts

- Understanding the Three Core Financial Statements

-

FASB: Understanding Financial Accounting Standards & GAAP

FASB: Understanding Financial Accounting Standards & GAAPThe Financial Accounting Standards Board (FASB) is an independent organization that exists in the private sector. It is responsible for establishing accounting standards for financial reporting within...

-

Full Disclosure Principle: Understanding Public Company Financial Reporting

Full Disclosure Principle: Understanding Public Company Financial ReportingThe Full Disclosure Principle states that all relevant and necessary information for the understanding of a company’s financial statements must be included in public company filingsPublic Compan...