Annuity Due Explained: Payments at the Beginning of Each Period

Annuity due refers to a series of equal payments made at the same interval at the beginning of each period. Periods can be monthly, quarterly, semi-annually, annually, or any other defined period. Examples of annuity due payments include rentals, leasesLeaseA lease is an implied or written agreement specifying the conditions under which a lessor accepts to let out a property to be used by a lessee. The, and insurance payments, which are made to cover services provided in the period following the payment.

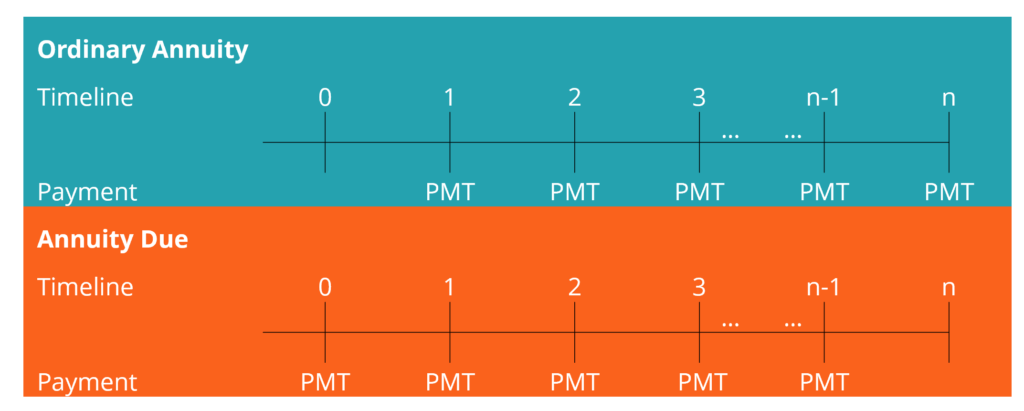

The annuity due can be illustrated as follows:

The first payment is received at the start of the first period, and thereafter, at the beginning of each subsequent period. The payment for the last period, i.e., period n, is received at the beginning of period n to complete the total payments due.

Summary

- Annuity due refers to a series of equal payments made at the same interval at the beginning of each period.

- The first payment is received at the start of the first period and, thereafter, at the start of each subsequent period.

- The present value of an annuity due uses the basic present value concept for annuities, except that cash flows are discounted to time zero.

Present Value of an Annuity Due

The present value of an annuity due uses the basic present value concept for annuities, except we should discount cash flow to time zero.

The formula for the present value of an annuity due is as follows:

Alternatively,

Where:

- PMT – Periodic cashflows

- r – Periodic interest rate, which is equal to the annual rate divided by the total number of payments per year

- n – The total number of payments for the annuity due

The second formula is intuitive, as the first payment (PMT on the right side of the equation) is made at the start of the first period, i.e., at time zero; hence it comes without a discounting effect.

Example

An individual makes rental payments of $1,200 per month and wants to know the present value of their annual rentals over a 12-month period. The payments are made at the start of each month. The current interest rate is 8% per annum.

Using the formula above:

FV of the Investment = $1,200 x 11.57

FV of the Investment = $13,886.90

Future Value of an Annuity Due

The future value of an annuity due uses the same basic future value concept for annuities with a slight tweak, as in the present value formula above.

To calculate the future value of an ordinary annuity:

Where:

- PMT – Periodic cashflows

- r – Periodic interest rate, which is equal to the annual rate divided by the total number of payments per year

- n – The total number of payments for the annuity due

Example

A company wants to invest $3,500 every six months for four years to purchase a delivery truck. The investment will be compounded at an annual interest rate of 12% per annum. The initial investment will be made now, and thereafter, at the beginning of every six months. What is the future value of the cash flow payments?

Using the formula above:

FV of the Investment = $3,500 x 10.49

FV of the Investment = $36,719.61

The calculations for PV and FV can also be done via Excel functions or by using a scientific calculator.

Annuity Due vs. Ordinary Annuity

1. Payments

The major difference between annuity due and the more popular ordinary annuity is that payments for an ordinary annuity are made at the end of the period, as opposed to annuity due payments made at the start of each period/interval. Ordinary annuity payments include loan repayments, mortgage paymentsMortgageA mortgage is a loan – provided by a mortgage lender or a bank – that enables an individual to purchase a home. While it’s possible to take out loans to cover the entire cost of a home, it’s more common to secure a loan for about 80% of the home’s value., bond interest payments, and dividend paymentsDividendA dividend is a share of profits and retained earnings that a company pays out to its shareholders. When a company generates a profit and accumulates retained earnings, those earnings can be either reinvested in the business or paid out to shareholders as a dividend..

2. Present value

Another difference is that the present value of an annuity due is higher than one for an ordinary annuity. It is a result of the time value of money principle, as annuity due payments are received earlier.

Hence, if you are set to make ordinary annuity payments, you will benefit from getting an ordinary annuity by holding onto your money longer (for the interval). Conversely, if you are set to receive annuity due payments, you will benefit, as you will be able to receive your money (value) sooner. In any annuity due, each payment is discounted one less period in contrast to a similar ordinary annuity.

The relationship in equation terms can be illustrated as below:

PV of an Annuity Due = PV of Ordinary Annuity * (1+i)

Multiplying the PV of an ordinary annuity with (1+i) shifts the cash flows one period back towards time zero.

The last difference is on future value. An annuity due’s future value is also higher than that of an ordinary annuity by a factor of one plus the periodic interest rate. Each cash flow is compounded for one additional period compared to an ordinary annuity.

The formula can be expressed as follows:

FV of an Annuity Due = FV of Ordinary Annuity * (1+i)

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- AmortizationAmortizationAmortization refers to the process of paying off a debt through scheduled, pre-determined installments that include principal and interest

- Installment LoanInstallment LoanAn installment loan refers to both commercial and personal loans that are extended to borrowers and that require regular payments.

- OverheadsOverheadsOverheads are business costs that are related to the day-to-day running of the business. Unlike operating expenses, overheads cannot be

- Net Present Value (NPV)Net Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present.

-

Equivalent Annual Annuity (EAA): Project Evaluation Explained

Equivalent Annual Annuity (or EAA) is a method of evaluating projects with different life durations. Traditional project profitability metrics such as NPVNPV FormulaA guide to the NPV formula in Excel

-

Jumbo CDs: Higher Rates & Deposits Explained

A jumbo CD is similar to a conventional CD although the former generally requires a higher deposit and accrues interest at a higher rate. A CD is a certificate of deposit that is offered by banks for

finance

- Commercial Annuities: Understanding Contracts & Payments

- Federal Annuities: A Comprehensive Overview for Qualified Individuals

- Fixed Annuities: A Comprehensive Guide to Guaranteed Retirement Income

- Understanding Due to Account: A Comprehensive Guide

- Fixed Annuities: A Comprehensive Guide to Guaranteed Retirement Income

- Deferred Annuities: A Comprehensive Guide for Retirement Planning

- Annuity Loans: Access Retirement Funds Without Cashing Out

- Understanding Annuity Due: Payments at the Start of a Period

- Annuities Explained: A Simple Guide to Retirement Income

-

Union Pension Annuities: A Comprehensive Guide

Union Pension Annuities: A Comprehensive GuideOne of the advantages of union membership is that workers are more likely to have retirement plans than are non-union employees. A union pension annuity is a defined-benefit pension plan regulated und...

-

Indexed Annuities: A Comprehensive Guide for Retirees

Indexed Annuities: A Comprehensive Guide for RetireesAn indexed annuity is a financial product that pays out a return based on the performance of a linked index. The contract is backed by an insurance company and is popular among retirees because it pro...