Understanding Bank Business Segments: Retail, Wholesale & Wealth Management

A bank’s major business segments are retail banking, wholesale banking, and wealth managementPrivate Wealth ManagementPrivate wealth management is an investment practice that involves financial planning, tax management, asset protection and other financial services for high net worth individuals (HNWI) or accredited investors. Private wealth managers create a close working relationship with wealthy clients to help build a portfolio that achieves the client’s financial goals.. While banks might have different names for their various business operations, they still have the same business functions as these three categories. Some larger banks also have business segments outside of the traditional three, such as treasury services or insurance. However, the revenueRevenueRevenue is the value of all sales of goods and services recognized by a company in a period. Revenue (also referred to as Sales or Income) generated by those segments is small compared to the primary segments.

Summary

- The three main business segments for a bank are retail banking, wholesale banking, and wealth management.

- Retail banking or personal banking involves deposits, mortgages, loans, and credit cards.

- Wholesale banking is related to sales and trading and mergers and acquisitions.

- Wealth management generates revenue through retail brokerage services and asset management.

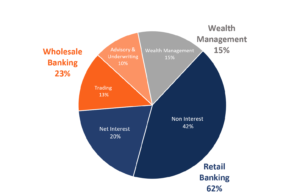

Revenue Breakdown by Segment

While the revenue distribution per business segment is different for all banks, the approximate breakdown by business segment is as follows:

What is the Retail Banking Segment?

Retail banking is the largest earnings contributor. It is the segment most people are familiar with, as it includes operations that occur in a bank’s branch. Products involved in retail banking include deposits, credit cards, and mortgages. This segment is also known as personal banking, as it serves individuals. However, it is also targeted towards small commercial clients.

Revenue from retail banking is split into interest and non-interest origins. Net interest income accounts for approximately 70% of retail revenues. It is calculated by taking the interest collected from mortgage and credit cards and subtracting interest paid on deposits. Non-interest income contributes around 30% of the retail banking segment’s revenue. It is calculated from taking the difference between all non-interest revenue and operating expenses.

The revenues are generated through account fees, transaction fees, credit card fees, and foreign exchange revenues. The fees are often small amounts and relatively unnoticed by the clients. Expenses included in this section are compensation costs and infrastructure costs. They can add up to 50% of a bank’s retail revenue.

What is the Wholesale Banking Segment?

Wholesale banking is the second largest segment for banks. Another name for wholesale banking is capital marketsCapital MarketsCapital markets are the exchange system platform that transfers capital from investors who want to employ their excess capital to businesses. This segment deals with corporate and institutional clients and is associated with investment bankingInvestment BankingInvestment banking is the division of a bank or financial institution that serves governments, corporations, and institutions by providing underwriting (capital raising) and mergers and acquisitions (M&A) advisory services. Investment banks act as intermediaries. Activities include corporate lending, sales and tradingSales and TradingSales and Trading (S&T) is a group at an investment bank that consists of salespeople, who call institutional investors with ideas and opportunities, and traders, who execute orders and advise clients on entering and exiting financial positions. Sales and trading is the lifeblood that makes or breaks a securities firm, and mergers and acquisitionsPurchase Accounting – Mergers & Acquisitions (M&A)This guide will cover purchase accounting for mergers and acquisitions. In an acquisition, a company purchases another company’s assets, identifiable business segments, or subsidiaries. In a merger, a company purchases another company in its entirety.. Business in the wholesale banking segment typically accounts for 15% to 40% of overall revenue. This largely depends on the bank and market conditions. This segment is the most difficult to forecast and is usually valued at a lower multiple. The difficulty in forecasting revenue stems from the volatility of markets and the lack of disclosure in transactions.

Trading is a volatile operation that represents 30 – 40% of wholesale revenue. Revenue emerges through realized and unrealized gains and losses on the trading of fixed income investments, currencies, commodities, and equities. Another operation in this segment is mergers & acquisitions. It is very profitable, as there are no capital requirements. Revenue depends on the fees, which are usually around 0.15 to 1.5% of the transaction value.

What is the Wealth Management Segment?

Wealth management is a quickly growing segment for banks. Revenue is generated through retail brokerage services and asset management. Wealth management is usually valued at a higher multipleComps - Comparable Trading MultiplesAnalyzing comparable trading multiples (Comps) involves analyzing companies with similar operating, financial and ownership profiles to provide a useful understanding of: operations, financials, growth rates, margin trends, capital spending, valuation multiples, DCF assumptions, and benchmarks for an IPO than other segments because of several reasons. It is more profitable due to lower credit requirements, there is lower volatility, and greater growth. Growth is attributed to the changing population demographics. As baby boomers start to save for retirement instead of taking out loans or mortgages, protecting and growing savings become more important. Therefore, wealth management is growing at a faster rate than other business segments.

In terms of revenue, since a majority of the assets managed are invested in equitiesEquityIn finance, equity is the market value of the assets owned by shareholders after all debts have been paid off. In accounting, equity refers to the book value of stockholders’ equity on the balance sheet, which is equal to assets minus liabilities. The term, "equity", in finance and accounting comes with the concept of fair and equal treatment, trading commissions contribute to revenue. There’s been more trading activity in recent years, which increases commissions. However, the short-term increase in trading revenue is a major source of volatility due to its dependence on the equity markets. On the other hand, since management-related fees do not depend on the performance of the market, volatility does not increase.

Advisors that can create and manage strong relationships with affluent clients is especially important in the wealth management segment. As both the trading commissions and management fees depend on the number of clients, it’s important to employ advisors who can fulfill the client’s goals. Stronger relationships also mean that clients are less likely to leave during market downturns. It is up to the advisors to convince clients to continue to trust the bank even when the markets are not doing well.

Additional Resources

Thank you for reading CFI’s article on the major business segment for banks. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep improving your knowledge, we recommend the following CFI resources:

- Sales and TradingSales and TradingSales and Trading (S&T) is a group at an investment bank that consists of salespeople, who call institutional investors with ideas and opportunities, and traders, who execute orders and advise clients on entering and exiting financial positions. Sales and trading is the lifeblood that makes or breaks a securities firm

- Investment BankingInvestment BankingCFI's Investment Banking Manual. This 400+ page guide is used as a real training tool and bulge bracket global investment banks. Learn everything a new investment banking analyst or associate needs to know to get started on the job. This guide and handbook teaches accounting, Excel, financial modeling, valuation,

- Financial AdvisorsFinancial AdvisorA Financial Advisor is a finance professional who provides consulting and advice about an individual’s or entity’s finances. Financial advisors can help individuals and companies reach their financial goals sooner by providing their clients with strategies and ways to create more wealth

- Buy Side vs. Sale SideBuy Side vs Sell SideBuy Side vs Sell Side. The Buy Side refers to firms that purchase securities and include investment managers, pension funds, and hedge funds. The Sell Side

-

Understanding Offshore Banking: Benefits and Regulations

Off shore banking provides benefits for international business. According to Offshorecompany.com, offshore banking is often considered as a form of tax evasion and money laundering in poorly

-

Alternatives to Online Banking: Secure Banking Options

finance

- Virtual Banking Explained: Everything You Need to Know

- Understanding Operating Expenses (OpEx): A Comprehensive Guide

- Understanding Bank Reserves: A Comprehensive Guide

- Understanding Key Bank Ratios: A Comprehensive Guide

- Banking Fundamentals: A Comprehensive Overview for Beginners

- Business Banking: Services, Accounts & Loans Explained

- Understanding Business Metrics: Key Performance Indicators & KPIs

- Fractional Banking Explained: How It Works & Its Role in Finance

- Non-Operating Assets: Definition, Examples & Financial Impact

-

Business Operations: Definition, Activities & Optimization

Business Operations: Definition, Activities & OptimizationBusiness operations refer to activities that businesses engage in on a daily basis to increase the value of the enterprise and earn a profit. The activities can be optimized to generate sufficient rev...

-

Exit Strategies: Planning Your Business's Future

Exit Strategies: Planning Your Business's FutureExit strategies are plans executed by business owners, investors, traders, or venture capitalistsVenture CapitalVenture capital is a form of financing that provides funds to early stage, emerging comp...