Commitment Fees Explained: What They Are & How They Work

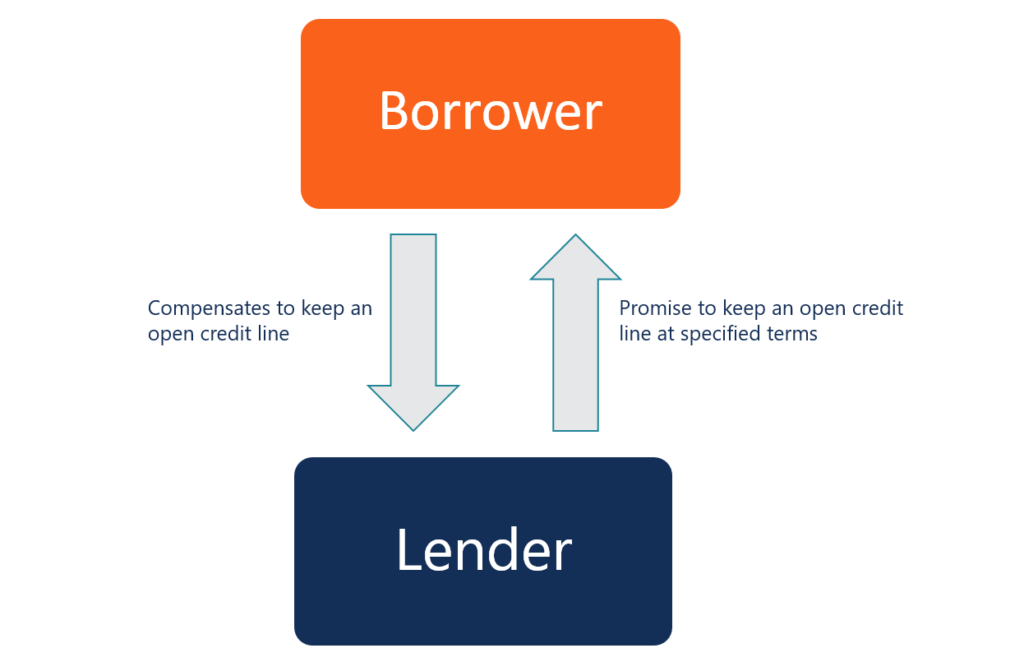

A commitment fee is a fee that is charged by a lender to a borrower to compensate the lenderTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks in the USA as of February 2014. for keeping a credit line open. The fee also secures a lender’s promise to provide the credit lineBank LineA bank line or a line of credit (LOC) is a kind of financing that is extended to an individual, corporation, or government entity, by a bank or other on the agreed terms at specific dates, regardless of the conditions of the financial markets. The fee compensates the lender for the risks associated with an open credit line despite uncertain future market conditions and the lender’s current inability to charge interestInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also on the principal.

Lenders send borrowers commitment letters stating the commitment fee and explaining how the fee was determined. Typically, a lender charges a flat fee or a percentage of the undisbursed or future loan amount. The percentage fee generally varies between 0.25% and 1%. The fee is usually paid after the credit agreement’s been finalized. However, the amount can be charged periodically if it is charged on the undistributed loan. In such cases, the fee is based on the average balance of the undisbursed loan amount.

Commitment Fee vs. Interest

Frequently, commitment fee and interest are often confused with another. Although there are similarities between the two, there is a significant difference between them. A commitment fee is charged on the undistributed or future loan, while interest is calculated on the amount that has already been distributed.

Sample Calculation

Company ABC obtained a $40 million credit line from Bank X at a 3% interest rate and with a 0.75% commitment fee to keep a credit line open. The fee is charged yearly on the unused portion of the credit line. ABC Corp. used $25 million in the first year. Thus, the fee paid to Bank X in the second year will be calculated in the following way:

Commitment Fee = Unused Amount of Credit Line × Commitment Rate

= ($40m – $25m) x 0.75% = $112,500

The situation above is an oversimplified example of commitment fee calculation. Generally, the fee is calculated periodically based on the average unused credit line balance, multiplied by the fee rate and by the number of days in the period.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Bridge LoanBridge LoanA bridge loan is a short-term form of financing that is used to meet current obligations before securing permanent financing. It provides immediate cash flow when funding is needed but is not yet available. A bridge loan comes with relatively high interest rates and must be backed by some form of collateral

- Debt CapacityDebt CapacityDebt capacity refers to the total amount of debt a business can incur and repay according to the terms of the debt agreement.

- Revolving Credit FacilityRevolving Credit FacilityA revolving credit facility is a line of credit that is arranged between a bank and a business. It comes with an established maximum amount, and the

- Trade CreditTrade CreditA trade credit is an agreement or understanding between agents engaged in business with each other that allows the exchange of goods and services

-

Hope Credit: Understanding Your Post-Secondary Education Tax Credit

The Hope Credit is one of the lifetime education tax credits in the U.S. that provides financial assistance to taxpayers or their children who are pursuing post-secondary education. The creation of th

-

Revolver Debt: Understanding Revolving Credit for Businesses & Individuals

Revolver debt, also known as revolving debt, is a form of credit that can be accessed by corporations and individuals. What separates revolving debt from regular installment loans, then? In a regular

finance

- Intraday Credit: Understanding Short-Term Account Overdrafts

- Credit Amnesty: Understanding the Truth & Avoiding Scams

- Understanding B Credit Ratings: What They Mean for Businesses

- Understanding Tender Fees: Costs in Corporate Takeovers

- Cashback Credit Cards: A Comprehensive Guide

- Credit Analysis: A Comprehensive Guide to Assessing Credit Risk

- Understanding Credit Scores: What They Are & Why They Matter

- HELOCs Explained: Flexible Home Equity Financing

- VantageScore 3.0: Understanding the Latest Credit Scoring Model

-

Credit Unions Explained: What They Are & How They Benefit You

Credit Unions Explained: What They Are & How They Benefit YouA credit union is a type of financial organization that is owned and governed by its members. Credit unions provide members with a variety of financial services, including checking and savings account...

-

Understanding FICO Scores: Your Key to Creditworthiness

Understanding FICO Scores: Your Key to CreditworthinessA FICO score, more commonly known as a credit score, is a three-digit number that is used to assess how likely a person is to repay the credit if the individual is given a credit card or if a lenderTo...