Equity Swap Contracts: Definition, Mechanics & Applications

An equity swap contract is a derivative contract between two parties that involves the exchange of one stream (leg) of equity-based cash flows linked to the performance of a stock or an equity indexDow Jones Industrial Average (DJIA)The Dow Jones Industrial Average (DJIA), also referred to as "Dow Jones” or "the Dow", is one of the most widely-recognized stock market indices. with another stream (leg) of fixed-income cash flows.

In equity swap contracts, the cash flows are based on a predetermined notional amount. However, unlike currency swaps, equity swaps do not imply the exchange of principal amountsPrincipal PaymentA principal payment is a payment toward the original amount of a loan that is owed. In other words, a principal payment is a payment made on a loan that reduces the remaining loan amount due, rather than applying to the payment of interest charged on the loan.. The exchange of cash flows occurs on fixed dates.

Equity swap contracts offer a great degree of flexibility; they can be customized to suit the needs of the parties participating in the swap contract. Essentially, equity swaps provide synthetic exposure to equities.

Advantages of Equity Swap Contracts

Equity swap contracts provide numerous benefits to the counterparties involved, including:

1. Avoid transaction costs

One of the most common applications of equity swap contracts is for the avoidance of transaction costsTransaction CostsTransaction costs are costs incurred that don’t accrue to any participant of the transaction. They are sunk costs resulting from economic trade in a market. In economics, the theory of transaction costs is based on the assumption that people are influenced by competitive self-interest. associated with equity trades. Also, in many jurisdictions, equity swaps provide tax benefits to the participating parties.

2. Hedge against negative returns

Equity swap contracts can be used in hedging risk exposures. The derivatives are frequently used to hedge against negative returns on a stock without forgoing the possession rights on it. For example, an investor holds some shares, but he believes that recent macroeconomic trends will push the stock price down in the short term, although he expects the stock to substantially appreciate in the long term. Thus, he might enter a swap agreement to mitigate possible negative short-term impact on the stock without selling the shares.

3. Access more securities

Finally, equity swap contracts may allow investing in securities that otherwise would be unavailable to an investor. By replicating the returns from a stock through an equity swap, the investor can overcome certain legal restrictions without breaking the law.

Similar to other types of swap contracts, equity swaps are primarily used by financial institutions, including investment banksList of Top Investment BanksList of the top 100 investment banks in the world sorted alphabetically. Top investment banks on the list are Goldman Sachs, Morgan Stanley, BAML, JP Morgan, Blackstone, Rothschild, Scotiabank, RBC, UBS, Wells Fargo, Deutsche Bank, Citi, Macquarie, HSBC, ICBC, Credit Suisse, Bank of America Merril Lynch, hedge funds, and lending institutions or large corporations.

Example

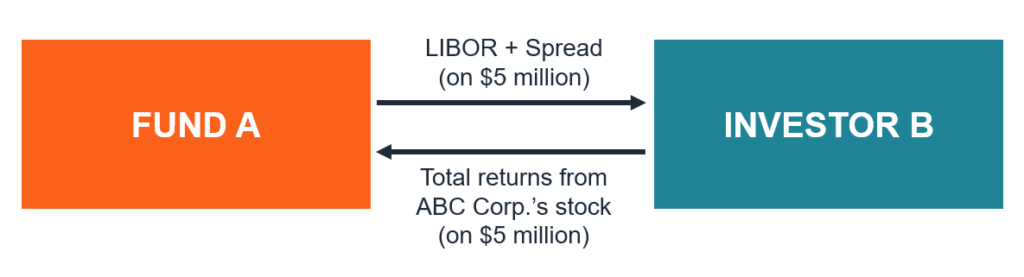

In order to understand the functioning of equity swap contracts, let’s consider the following example. The manager of Fund A is wanting to replicate the returns of ABC Corp.’s stock without purchasing the company’s actual shares.

On the other hand, Investor B holds a long position in the stocks of ABC Corp. Investor B believes that the company’s stock price will be volatile in the short term, thus he wants to hedge the potential risk of the stock price dropping. Fund A and Investor B can create an equity swap contract with each other to achieve their respective goals. The swap will include the exchange of future streams of cash flows.

One leg of the swap will be paid by Fund A to Investor B and will be the stream of floating payments linked to the LIBORLIBORLIBOR, which is an acronym of London Interbank Offer Rate, refers to the interest rate that UK banks charge other financial institutions for index. The other swap leg will be paid by Investor B to Fund A and will be based on the future total returns of ABC Corp.’s stock for the specified period.

Both legs will be calculated using a notional principal amount. In this case, both parties agree on a notional principal amount of $5,000,000. Note that Fund A and Investor B will not exchange principal amounts at the beginning of the contract nor on the maturity date.

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Credit Default SwapCredit Default SwapA credit default swap (CDS) is a type of credit derivative that provides the buyer with protection against default and other risks. The buyer of a CDS makes periodic payments to the seller until the credit maturity date. In the agreement, the seller commits that, if the debt issuer defaults, the seller will pay the buyer all premiums and interest

- Interest Rate SwapInterest Rate SwapAn interest rate swap is a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another

- Risk and ReturnRisk and ReturnIn investing, risk and return are highly correlated. Increased potential returns on investment usually go hand-in-hand with increased risk. Different types of risks include project-specific risk, industry-specific risk, competitive risk, international risk, and market risk.

- Swap SpreadSwap SpreadSwap spread is the difference between the swap rate (the rate of the fixed leg of a swap) and the yield on the government bond with a similar maturity. Since government bonds (e.g., US Treasury securities) are considered risk-free securities, swap spreads typically reflect the risk levels perceived by the parties involved in a swap agreement.

-

Understanding Horizontal Equity in Taxation

Horizontal equity is an economic theory that is used to assess the fairness of tax burden across a population. The theoretical underpinning of horizontal equity is that the amount of taxes paid should

-

Interest Rate Swaps: A Comprehensive Guide

An interest rate swap is a type of a derivative contract through which two counterparties agree to exchange one stream of future interest payments for another, based on a specified principal amount. I

finance

- Backstop: Understanding Financial Safety Nets and Contingency Funding

- Commodity Swaps: Definition, Uses & Hedging Strategies

- Currency Swap Contracts: Definition & How They Work

- Debt/Equity Swap: Understanding Financial Restructuring

- Understanding Equity: A Comprehensive Guide for Investors

- Equity Crowdfunding: A Comprehensive Guide for Startups & Investors

- Understanding Negative Equity: Causes, Risks & Solutions

- Equity Futures Contracts: Definition, Types & Uses

- Volatility Swaps: A Comprehensive Guide for Investors

-

Equity Swap Contracts: Definition, Mechanics & Applications

Equity Swap Contracts: Definition, Mechanics & ApplicationsAn equity swap contract is a derivative contract between two parties that involves the exchange of one stream (leg) of equity-based cash flows linked to the performance of a stock or an equity indexDo...

-

Forward Contracts: Definition, How They Work & Examples

Forward Contracts: Definition, How They Work & ExamplesA forward contract, often shortened to just forward, is a contract agreement to buy or sell an assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in th...