Understanding Loan Delinquency Rates: A Key Indicator of Credit Portfolio Health

The delinquency rate refers to the percentage of loans that are past due. It indicates the quality of a lending company’s or a bank’s loan portfolio.

Understanding the Delinquency Rate

The delinquency rate is commonly used by analysts to determine the quality of the loan portfolio of lending companies or banksTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks in the USA as of February 2014. . It compares the percentage of loans that are overdue to the total number of loans. A lower rate is always desirable, as it indicates that there are fewer loans in the lender’s loan portfolio that are paying outstanding debt late.

In the industry, lenders typically do not label a loan as being delinquent until the loan is 60 days past due. However, the figure is not absolute and varies from lender to lender. For example, one lender may consider a 30-day overdue loan as delinquent while another lender may only consider a 45-day overdue loan as delinquent.

When a loan is labeled as delinquent, lending companies generally work with third-party collection agencies to recover the loan. If the delinquent loan is unable to be recovered after an extended period of time, it is written off by the lender.

Formula for the Delinquency Rate

Where:

- Number of Delinquent Loans refers to the number of loans that have missed their payments; and

- Total Number of Loans refers to the total number of loans in the loan portfolio.

Practical Example

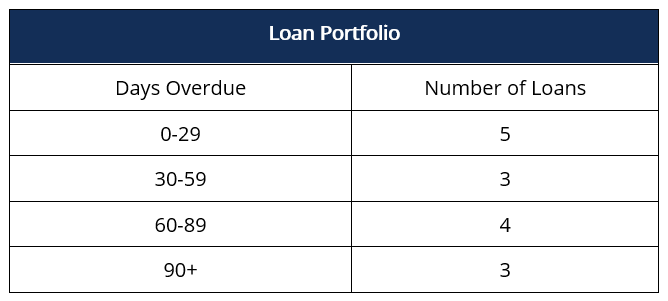

A loan portfolio currently consists of 45 loans. Of the 45 loans in the portfolio, 15 have payments that are overdue. The following is a schedule outlining the overdue loans:

If the loan portfolio defines delinquent loans as loans that are overdue by 60 days or more, what is the rate of delinquency of the loan portfolio?

Delinquency Rate = (7 / 45) x 100 = 15.55% = 16%

Interpreting the Delinquency Rate

The lower the delinquency rate, the higher the quality of the loan portfolio. The rate should be compared to an industry average or among the loan portfolio of competitors to determine whether the loan portfolio shows an “acceptable” rate.

A major drawback is that the calculation of the rate of delinquency uses the number of loans instead of the value of loans. To analysts, it is important to understand the value of loans that are delinquent before making an assessment regarding the quality of the loan portfolio.

For example, if a portfolio of 100 loans valued at $1,000,000 has ten loans that are delinquent with a value of $1,000, one can argue that the delinquent loans do not have a material impact on the overall loan portfolio. As such, a modification to the rate of delinquency is to use the value of the delinquent loans to the value of the loan portfolio. The modified delinquency rate is shown as follows:

In the example above, the modified delinquency rate of the $1 million loan portfolio would be ($1,000 / $1,000,000) x 100 = 0.1%. Had an analyst used the number of delinquent loans instead of the value of delinquent loans, the analyst would generate a rate of delinquency of (10 / 100) x 100 = 10%.

Therefore, the delinquency rate should only be used for a loan portfolio whose underlying loans are of similar value. If the value of the underlying loans varies greatly, the modified version should be used.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below:

- Debt CapacityDebt CapacityDebt capacity refers to the total amount of debt a business can incur and repay according to the terms of the debt agreement.

- Loan ServicingLoan ServicingLoan servicing is the way a finance company (a lender) goes about collecting principal, interest, and escrow payments that are due or overdue.

- Probability of DefaultProbability of DefaultProbability of Default (PD) is the probability of a borrower defaulting on loan repayments and is used to calculate the expected loss from an investment.

- Recovery RateRecovery RateRecovery rate, commonly used in credit risk management, refers to the amount recovered when a loan defaults. In other words, the recovery rate is the amount, expressed as a percentage, recovered from a loan when the borrower is unable to settle the full outstanding amount. A higher rate is always desirable.

-

Understanding Swap Rate Curves: A Comprehensive Guide

The swap rate curve is a chart that depicts the relationship between swap rates and all available corresponding maturities. Essentially, it indicates the expected returnsExpected ReturnThe expected re

-

Understanding Implied Rates: A Comprehensive Guide

The implied rate is an interest rate that expresses the difference between the forward/future rate and the spot rate. It serves as a useful tool for comparing returns across different assets and can b

finance

- Understanding APR: What It Is and How It Works

- Asset-Based Loans: A Comprehensive Guide for Businesses

- Compound Growth Rate: Definition & Calculation | [Your Brand]

- Understanding Coupon Rate: A Key Bond Investment Metric

- Understanding Forward Rates: A Comprehensive Guide

- Understanding Loans: Definition, Types & How They Work

- Understanding the Overnight Interest Rate: A Comprehensive Guide

- Prime Rate Explained: Understanding Interest Rates for Businesses & Consumers

- Conventional Loans: Your Guide to Private Mortgage Options

-

Recourse Loans Explained: Understanding Borrower Liability

Recourse Loans Explained: Understanding Borrower LiabilityA recourse loan – alternatively known as recourse debt – is a type of loan that makes the borrower 100% liable for any outstanding balance. The loans require collateralCollateralCollateral...

-

Swap Rate Explained: Understanding Fixed Exchange Rates in Derivatives

Swap Rate Explained: Understanding Fixed Exchange Rates in DerivativesThe swap rate is the fixed rate of a swapSwapA swap is a derivative contract between two parties that involves the exchange of pre-agreed cash flows of two financial instruments. The cash flows a...