Peer-to-Peer (P2P) Lending: A Comprehensive Guide

Peer-to-peer lending is a form of direct lending of money to individuals or businesses without an official financial institution participating as an intermediaryFinancial IntermediaryA financial intermediary refers to an institution that acts as a middleman between two parties in order to facilitate a financial transaction. The institutions that are commonly referred to as financial intermediaries include commercial banks, investment banks, mutual funds, and pension funds. in the deal. P2P lending is generally done through online platforms that match lenders with the potential borrowers.

P2P lending offers both secured and unsecured loansBridge LoanA bridge loan is a short-term form of financing that is used to meet current obligations before securing permanent financing. It provides immediate cash flow when funding is needed but is not yet available. A bridge loan comes with relatively high interest rates and must be backed by some form of collateral. However, most of the loans in P2P lending are unsecured personal loans. Secured loans are rare for the industry and are usually backed by luxury goods. Due to some unique characteristics, peer-to-peer lending is considered as an alternative source of financing.

How does peer-to-peer lending work?

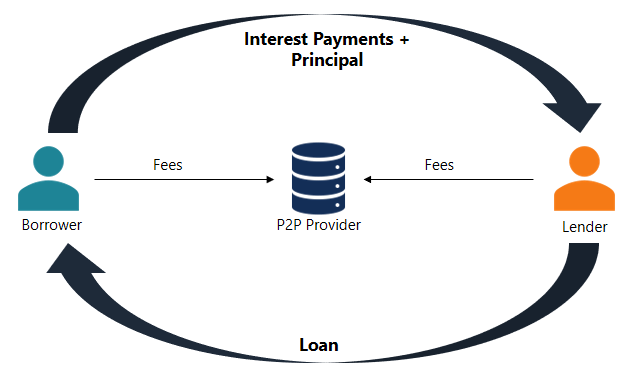

Peer-to-peer lending is a fairly straightforward process. All the transactions are carried out through a specialized online platform. The steps below describe the general P2P lending process:

- A potential borrower interested in obtaining a loan completes an online application on the peer-to-peer lending platform.

- The platform assesses the application and determines the risk and credit ratingFICO ScoreA FICO score, more commonly known as a credit score, is a three-digit number that is used to assess how likely a person is to repay the credit if the individual is given a credit card or if a lender loans them money. FICO scores are also used to help determine the interest rate on any credit extended of the applicant. Then, the applicant is assigned with the appropriate interest rate.

- When the application is approved, the applicant receives the available options from the investors based on his credit rating and assigned interest ratesInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal..

- The applicant can evaluate the suggested options and choose one of them.

- The applicant is responsible for paying periodic (usually monthly) interest payments and repaying the principal amount at maturity.

The company that maintains the online platform charges a fee for both borrowers and investors for the provided services.

Advantages and disadvantages of peer-to-peer lending

Peer-to-peer lending provides some significant advantages to both borrowers and lenders:

- Higher returns to the investors: P2P lending generally provides higher returns to the investors relative to other types of investments.

- More accessible source of funding: For some borrowers, peer-to-peer lending is a more accessible source of funding than conventional loans from financial institutions. This may be caused by the low credit rating of the borrower or atypical purpose of the loan.

- Lower interest rates: P2P loans usually come with lower interest rates because of the greater competition between lenders and lower origination fees.

Nevertheless, peer-to-peer lending comes with a few disadvantages:

- Credit risk: Peer-to-peer loans are exposed to high credit risks. Many borrowers who apply for P2P loans possess low credit ratings that do not allow them to obtain a conventional loan from a bank. Therefore, a lender should be aware of the default probability of his/her counterparty.

- No insurance/government protection: The government does not provide insurance or any form of protection to the lenders in case of the borrower’s default.

- Legislation: Some jurisdictions do not allow peer-to-peer lending or require the companies that provide such services to comply with investment regulations. Therefore, peer-to-peer lending may not be available to some borrowers or lenders.

More resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following free CFI resources:

- Cash CreditCash CreditA Cash Credit (CC) is a short-term source of financing for a company. In other words, a cash credit is a short-term loan extended to a company by a bank. It enables a company to withdraw money from a bank account without keeping a credit balance.

- Debt CapacityDebt CapacityDebt capacity refers to the total amount of debt a business can incur and repay according to the terms of the debt agreement.

- Loan CovenantLoan CovenantA loan covenant is an agreement stipulating the terms and conditions of loan policies between a borrower and a lender. The agreement gives lenders leeway in providing loan repayments while still protecting their lending position. Similarly, due to the transparency of the regulations, borrowers get clear expectations of

- PrepaymentPrepaymentA Prepayment is any payment that is made before its official due date. Prepayments may be made for goods and services or towards the settlement of debt. They can be categorized into two groups: Complete Prepayments and Partial Prepayments.

-

Peer-to-Peer Lending: A Comprehensive Guide for Investors & Borrowers

Looking for a new investment avenue to boost your wealth? Or maybe you need to borrow money to open up your own business or afford a down payment on your first home? Whether you need a lo

-

Annuities Explained: A Simple Guide to Retirement Income

So you're wondering what is an annuity? There are dozens of different flavours of annuities that perform different functions and pay their holders out in different ways, but for our purposes let’

finance

- Consumer Lending: Types, Benefits & How It Works

- Securities Lending: Definition, Process & Benefits

- Peer-to-Peer Lending: Benefits & Advantages - A Comprehensive Guide

- Peer-to-Peer Lending: A Comprehensive Guide for Borrowers & Lenders

- P2P Lending vs. Family Loans: Which is Right for You?

- Safeguarding Your Investments: 5 Risk Reduction Strategies for P2P Lending

- Peer-to-Peer Lending: A Comprehensive Guide for Borrowers & Investors

- Understanding Crypto Lending: Risks & Opportunities

- Peer-to-Peer Lending (P2P): A Comprehensive Guide for Borrowers & Investors

-

Jumbo CDs: Higher Rates & Deposits Explained

Jumbo CDs: Higher Rates & Deposits ExplainedA jumbo CD is similar to a conventional CD although the former generally requires a higher deposit and accrues interest at a higher rate. A CD is a certificate of deposit that is offered by banks for ...

-

Understanding Regulation Z: Your Rights as a Borrower

Understanding Regulation Z: Your Rights as a BorrowerRegulation Z is a consumer-protection regulation that compels lenders to disclose the cost of credit in a clear way for consumers. Whether you’re applying for a mortgage or dealing...