Pecking Order Theory: Understanding Corporate Financing Strategies

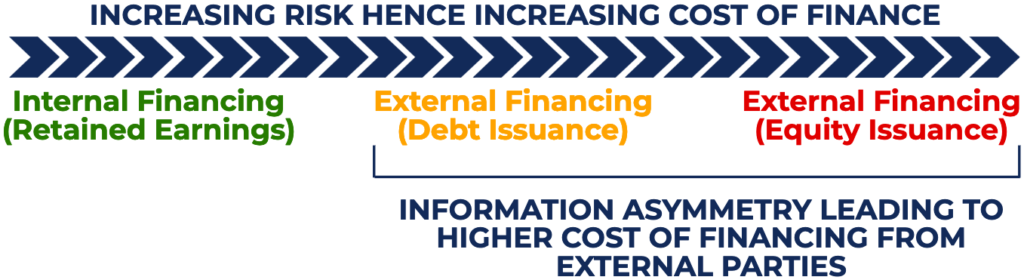

The Pecking Order Theory, also known as the Pecking Order Model, relates to a company’s capital structureCapital StructureCapital structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. A firm's capital structure. Made popular by Stewart Myers and Nicolas Majluf in 1984, the theory states that managers follow a hierarchy when considering sources of financing.

The pecking order theory states that managers display the following preference of sources to fund investment opportunities: first, through the company’s retained earnings, followed by debt, and choosing equity financing as a last resort.

Illustration of the Pecking Order Theory

The following diagram illustrates the pecking order theory:

Understanding the Pecking Order Theory

The pecking order theory arises from the concept of asymmetric informationAsymmetric InformationAsymmetric information is, just as the term suggests, unequal, disproportionate, or lopsided information. It is typically used in reference to some type of business deal or financial arrangement where one party possesses more, or more detailed, information than the other.. Asymmetric information, also known as information failure, occurs when one party possesses more (better) information than another party, which causes an imbalance in transaction power.

Company managers typically possess more information regarding the company’s performance, prospects, risks, and future outlook than external users such as creditors (debt holders) and investors (shareholdersShareholderA shareholder can be a person, company, or organization that holds stock(s) in a given company. A shareholder must own a minimum of one share in a company’s stock or mutual fund to make them a partial owner.). Therefore, to compensate for information asymmetry, external users demand a higher return to counter the risk that they are taking. In essence, due to information asymmetry, external sources of finances demand a higher rate of return to compensate for higher risk.

In the context of the pecking order theory, retained earningsRetained EarningsThe Retained Earnings formula represents all accumulated net income netted by all dividends paid to shareholders. Retained Earnings are part financing (internal financing) comes directly from the company and minimizes information asymmetry. As opposed to external financing, such as debt or equity financing where the company must incur fees to obtain external financing, internal financing is the cheapest and most convenient source of financing.

When a company finances an investment opportunity through external financing (debt or equity), a higher return is demanded because creditors and investors possess less information regarding the company, as opposed to managers. In terms of external financing, managers prefer to use debt over equity – the cost of debtCost of DebtThe cost of debt is the return that a company provides to its debtholders and creditors. Cost of debt is used in WACC calculations for valuation analysis. is lower compared to the cost of equity.

The issuance of debt often signals an undervalued stock and confidence that the board believes the investment is profitable. On the other hand, the issuance of equity sends a negative signal that the stock is overvalued and that the management is looking to generate financing by diluting shares in the company.

When thinking of the pecking order theory, it is useful to consider the seniority of claims to assets. Debtholders require a lower return as opposed to stockholders because they are entitled to a higher claim to assets (in the event of a bankruptcy). Therefore, when considering sources of financing, the cheapest is through retained earnings, second through debt, and third through equity.

Example of the Pecking Order Theory

Suppose ABC Company is looking to raise $10 million for an investment project. The company’s stock price is currently trading at $53.77. Three options are available for ABC Company:

- Finance the project directly through retained earnings;

- One-year debt financing with an interest rate of 9%, although management believes that 7% is the fair rate

- Issuance of equity that will underprice the current stock price by 7%.

What would be the cost to shareholders for each of the three options?

Option 1: If management finances the project directly through retained earnings, the cost is $10 million.

Option 2: If management finances the project through debt issuance, the one-year debt would cost $10.8 million ($10 x 1.08 = $10.8). Discounting it back one year with the management’s fair rate would yield a cost of $10.09 million ($10.8 / 1.07 = $10.09 million).

Option 3: If management finances the project through equity issuance, to raise $10 million, the company would need to sell 200,000 shares ($53.77 x 0.93 = $50, $10,000,000 / $50 = 200,000 shares). The true value of the shares would be $10.75 million ($53.77 x 200,000 shares = $10.75 million). Therefore, the cost would be $10.75 million.

As illustrated, management should first finance the project through retained earnings, second through debt, and lastly through equity.

Key Takeaways of the Pecking Order Theory

The pecking order theory relates to a company’s capital structure in that it helps explain why companies prefer to finance investment projects with internal financing first, debt second, and equity last. The pecking order theory arises from information asymmetry and explains that equity financing is the costliest and should be used as a last resort to obtain financing.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Cost of CapitalCost of CapitalCost of capital is the minimum rate of return that a business must earn before generating value. Before a business can turn a profit, it must at least generate sufficient income to cover the cost of funding its operation.

- Debt vs Equity FinancingDebt vs Equity FinancingDebt vs Equity Financing - which is best for your business and why? The simple answer is that it depends. The equity versus debt decision relies on a large number of factors such as the current economic climate, the business' existing capital structure, and the business' life cycle stage, to name a few.

- Project FinanceProject Finance - A PrimerProject finance primer. Project finance is the financial analysis of the complete life-cycle of a project. Typically, a cost-benefit analysis is used to

- Revenue-based FinancingRevenue-Based FinancingRevenue-based financing, also known as royalty-based financing, is a type of capital-raising method in which investors agree to provide capital to a company in exchange for a certain percentage of the company’s ongoing total gross revenues.

-

Understanding Investor Influence & Key Investment Methods

The level of investor influence a company holds in an investment transactionInvestment MethodsThis guide and overview of investment methods outlines they main ways investors try to make money and mana

-

Net Debt to EBITDA Ratio: Understanding Company Solvency

The net debt-to-EBITDA ratio measures a company’s ability to pay off its liabilities. It shows how much time the company needs to operate at the current debt and EBITDA levels to pay all of its

finance

- Acid-Test Ratio: Understanding Your Company's Short-Term Liquidity

- Dividend Irrelevance Theory: Understanding Its Implications

- Understanding the Earnings Multiplier (P/E Ratio): A Comprehensive Guide

- Equity Financing: A Comprehensive Guide for Business Growth

- Understanding the IPO Process: A Comprehensive Guide

- Modigliani-Miller Theorem: Understanding Capital Structure & Firm Value

- Skin in the Game: Understanding Risk & Accountability

- SWORD Financing: Funding Biotech R&D - A Comprehensive Guide

- Revenue-Based Financing: A Comprehensive Guide

-

Understanding the Envy Ratio in Private Equity

Understanding the Envy Ratio in Private EquityIn private equity, the envy ratio is a ratio that shows the price paid by investors in relation to the price paid by the management team for their respective shares of the company’s common equit...

-

Equity Capital Market: Definition & How It Works

Equity Capital Market: Definition & How It WorksThe equity capital market is a subset of the broader capital market, where financial institutions and companies interact to trade financial instruments and raise capital for companies. Equity capital ...