Understanding Corporate Liquidity: Sources and Types

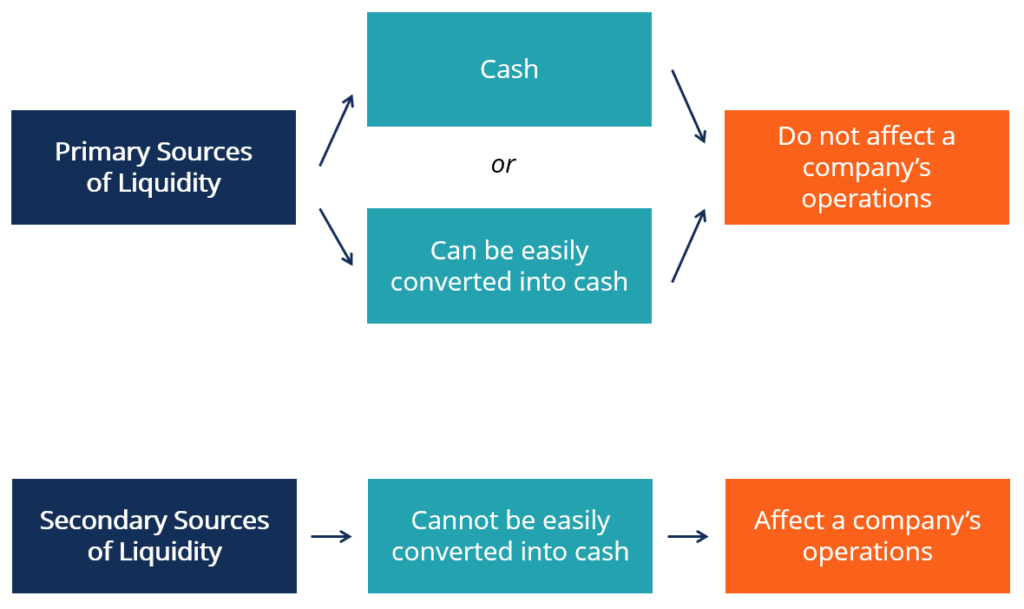

For a company, its sources of liquidity are all the resources that can be used to generate cash. There are generally two major classes of sources of liquidity for a company:

- The primary sources of liquidity, which are either cash or other resources that can be converted into cash very easily; and

- The secondary sources of liquidity, which usually can’t be converted into cash as easily and fast as the primary sources and may imply asset sales or other actions that would affect a company’s operations.

Primary Sources of Liquidity

Primary sources of liquidity can be easily used to generate liquidity for the company. They are generally cash and other near-cash assets. More specifically, they include:

1. Cash balances (generally in a bank account)

They can be either actual cash already stored in bank accounts or cash that can be generated by the liquidation of short-term securities (which comes with a maturity of less than 90 days). On the balance sheet, such sources of liquidity are generally indicated by the item “cash and cash equivalentsCash EquivalentsCash and cash equivalents are the most liquid of all assets on the balance sheet. Cash equivalents include money market securities, banker's acceptances.”

2. Short-term funds

They include commercial credit (i.e., trade payables), bank credit, and short-term securities not maturing within 90 days.

3. Cash flow management

They are related to the company’s ability to manage cash effectively and the level of decentralization of cash inflows and outflows. For example, a company with a highly decentralized collection system may find it more difficult to access cash resources promptly.

Secondary Sources of Liquidity

Unlike the primary sources of liquidity, the secondary sources usually cannot be converted into cash without an effect on the company’s operations. For example, it can be the case of a company that has run out of cash and near-cash assets and needs to liquidate assets, such as inventory, plants, and equipment, to pay its bills.

More specifically, a company’s secondary sources of liquidity include:

1. Negotiating its debt obligations

A company can generate liquidity by getting more favorable terms on its debt, i.e., by renegotiating maturities, the size and timing of principal repayments, and interest rates.

2. Liquidating assets

It can involve relatively liquid assets, such as inventory, or other less liquid assets, such as plant, equipment, and real estate properties. The urgency with which the cash is needed in the situations where liquidation is necessary generally implies that the assets are sold at a discount to their usual price.

3. Bankruptcy protection and reorganization

Sources of Liquidity and Business Health

Liquidity is a key factor in assessing a company’s creditworthinessCreditworthinessCreditworthiness, simply put, is how "worthy" or deserving one is of credit. If a lender is confident that the borrower will honor her debt obligation in a timely fashion, the borrower is deemed creditworthy.. To fully pay what it owes on time, a company must have access to proper sources of liquidity. Generally speaking, a financially healthy company should be able to meet its obligations relying on its primary sources of liquidity.

If access to secondary resources is needed, it means that the company has experienced, or is experiencing, liquidity issues. While it can be due to temporary conditions, it’s often a sign of deeper fundamental problems in the business.

Ratios, Business Fundamentals, and Sources of Liquidity

For an analyst or a manager, it’s usually possible to assess whether a company is likely going to need to use secondary resources of liquidity by assessing its financial health. The process generally relies on, but is not limited to, the analysis of the following aspects of a business:

1. Free cash flow generation, margins, and overall business trends

For example, other conditions being equal, a company that produces large and rising cash flows will be better equipped to face its current obligations without access to secondary sources of liquidity than a company with small and declining cash flows.

2. Liquidity ratios (Current ratio, quick ratio, and accounts receivable turnover)

For example, a deterioration in the ratio between cash and current liabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the can put a company in dangerous territory. Indications that a company is finding it difficult to collect payments can also contribute to increasing the risk of reliance on secondary sources of liquidity.

3. Competition, business risks, and other factors

Additional factors that are not visible in financial statements can indicate that a company’s primary sources of liquidity will not be enough to face obligations. For example, it can be the case of a company that is going to face a large fine or a business that is going to face a sudden increase in competition or whose cash has been seized by authorities.

Related Readings

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Credit EventCredit EventA credit event refers to a negative change in the credit standing of a borrower that triggers a contingent payment in a credit default swap (CDS). It occurs when an individual or organization defaults on its debt and is unable to comply with the terms of the contract entered, triggering a credit derivative such as a credit default swap.

- Financial RatiosFinancial RatiosFinancial ratios are created with the use of numerical values taken from financial statements to gain meaningful information about a company

- Quick RatioQuick RatioThe Quick Ratio, also known as the Acid-test, measures the ability of a business to pay its short-term liabilities with assets readily convertible into cash

- Statement of Cash FlowsStatement of Cash FlowsThe Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements that report the cash

-

![Cash Budget: Benefits & How to Limit Expenses - [Year]](https://www.etffin.com/article/uploadfiles/202109/2021092517342195_S.jpg)

Cash Budget: Benefits & How to Limit Expenses - [Year]

A cash budget is based on the money your business actually earns A cash budget is a finance tool geared toward limiting a company's expenditures to the amount of cash it actually has avai

-

Diversify Your Income: Exploring Multiple Income Streams

There are many different sources of income, but only a few people grab multiple opportunities. If you are really interested in building your personal wealth, you need to have a deeper understand

finance

- Understanding the Benefits of Account Liquidity

- Cash Reserves: Definition, Benefits & Short-Term Needs

- Understanding Corporate Finance Ratios: A Comprehensive Guide

- Understanding Financial Ratios: A Comprehensive Guide

- Understanding Liquidity in Financial Markets: A Comprehensive Guide

- Understanding Non-Cash Expenses: A Comprehensive Guide

- Funding Sources for Businesses: A Comprehensive Guide

- Understanding Accounting Transactions: A Comprehensive Guide

- Understanding Cash Equivalents: Definition & Examples

-

Disbursement Explained: Definition, Impact & Accounting Implications

Disbursement Explained: Definition, Impact & Accounting ImplicationsA disbursement is an act of paying out money – especially from a public or dedicated fund. It often refers to the payment made for a client to a third party, as reimbursement will be sought from...

-

Profit vs. Cash Flow: Understanding the Key Difference

Profit vs. Cash Flow: Understanding the Key DifferenceUnderstanding the difference between profit vs cash is very important in the finance industry. Profit is defined as revenue less all the expenses of a company in a certain period, while cash flow is c...